TODAY’S S&P 500 SET-UP – March 15, 2012

As we look at today’s set up for the S&P 500, the range is 32 points or -1.81% downside to 1369 and 0.48% upside to 1401.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1436 (-3249)

- VOLUME: NYSE 853.21 (-5.94%)

- VIX: 15.31 3.45% YTD PERFORMANCE: -34.57%

- SPX PUT/CALL RATIO: 1.01 from 1.42 (-28.87%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – here’s your hat-trick of ‘not goods’; if you are long anything in Fixed Income, that is (who would be?) – Treasury Bonds are getting blasted – 2yr yield have moved +44% to the upside in 2 weeks. It’s a good thing there is zero asymmetric risk with the Bernank’s zero bound policy.

- TED SPREAD: 39.24

- 3-MONTH T-BILL YIELD: 0.08%

- 10-Year: 2.29 from 2.27

- YIELD CURVE: 1.82 from 1.74

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Empire Manufacturing, Mar., est. 17.5 (prior 19.53)

- 8:30am: PPI (M/m), Feb., est. 0.5% (prior 0.1%)

- 8:30am: Jobless Claims, week Mar. 10, est. 357k (prior 362k)

- 9am: TIC Flows, Jan., est. $40.0b (prior $87.1b)

- 9:45am: Bloomberg Consumer Comfort, week of Mar. 11, est. -36.0 (prior -36.7)

- 10am: Philadelphia Fed., Mar., est. 12 from 10.2

- 10am: Freddie Mac mortgage rates

- Treasury Secretary Tim Geithner speaks to Economic Club of New York, Noon

GOVERNMENT:

- President Obama travels to an Prince George’s County Community College to talk about energy

- FERC meets to discuss Exelon-Constellation merger, PJM plan for capacity pricing, 10am

- House in recess, Senate in session:

- Senate Appropriations subcommittee hears from Transportation Secretary on agency’s budget, 9am

- Senate Appropriations subcommittee hears from FBI director on agency’s budget, 10am

- Senate Environment subcommittee hears from Nuclear Regulatory Commission chairman on lessons from Fukushima, 10am

- Senate Finance Committee hears from Deere & Co. Chairman on establishing normal trade relations with Russia, 10am

- Supreme Court not in session

WHAT TO WATCH:

- Cisco Systems said to be in advanced talks to acquire NDS Group for $5b: Calcalist

- Yahoo! investor Third Point plans to file preliminary proxy statement “within the week” to seek shareholder votes on proposed slate of four new directors

- LSI Corp. filed complaint with ITC against Funai Electric, MediaTek and Realtek Semiconductor over technology used in audiovisual devices

- Credit-card cos. report monthly net charge-offs, delinquencies

- Schlumberger said to seek buyers for unit that distributes oilfield supplies, business that may fetch as much as $800m

- Google will present changes to search engine over next few months that could affect millions of websites: WSJ

- Morgan Stanley preparing to invest millions in Mexican energy cos. as country opens up industry to private capital

- Foreclosure filings in the U.S. fell 8% in Feb., smallest y/y decrease since Oct. 2010: RealtyTrac

- House Republicans pushing for new round of budget cuts this year, congressional aides say, raising possibility of govt. shutdown shortly before Nov. election

- Tropical cyclone Lua forecast to strengthen on Australia’s northwest coast as Chevron evacuates workers from gas projects, iron ore ships steam out to sea

EARNINGS:

- Quebecor (QBR/B CN) 6 a.m., C$0.91

- Hanwa Solar (HSOL) 6 a.m., $(0.30)

- Aurizon Mines (ARZ CN) 6 a.m., C$0.13

- Gabriel Resources (GBU CN) 7 a.m., $(0.01)

- Scholastic (SCHL) 7 a.m., $(0.70)

- Winnebago (WGO) 7 a.m., $0.04

- Cato (CATO) 7 a.m., $0.34

- AMC Networks (AMCX) 8 a.m., $0.60

- Ross Stores (ROST) 8:30 a.m., $0.85

- Athabasca Oil Sands (ATH CN) Pre-mkt, C$(0.03)

- Crescent Point Energy (CPG CN) 9 a.m., C$0.12

- Dole (DOLE) 4:05 p.m., $(0.12)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

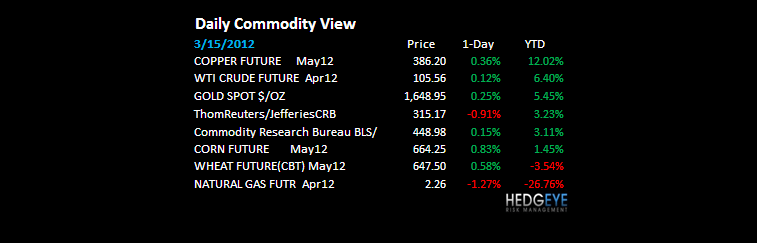

- Cocoa Rally Fading as African Rains Erase Shortage: Commodities

- Soybeans Near Six-Month High as Brazil Crop May Miss Estimates

- Oil Trades Near One-Week Low on Supply; Goldman Sees $130 Brent

- Copper Swings Between Gains, Losses on Chinese, U.S. Economies

- Gold Rebounds in New York as Low Interest Rates May Spur Demand

- Cocoa Falls to One-Week Low as Rains Boost Crops; Sugar Advances

- Global Food Prices Seen Declining as Demand Growth Slows

- Rubber Shortage Widening to Bolster Prices, Producers Say

- Oil Exports Ease Crude Sting for U.S. Economy: Chart of the Day

- Obama’s Keystone Denial Imperils Refiners’ $25 Billion Oil Bet

- Oil at $126 Boosts BP Ability to Pay More for Gulf Spill: Energy

- Checking German Power May Trim Poland Price Gap: Energy Markets

- Orange-Juice Price Seen Unaffected by End to U.S. Brazil Duties

- Iron Ore Seen Rallying as China Lending Policy May Boost Demand

- Fortescue Raises $2 Billion From Junk Bonds After Doubling Sale

- Impala’s Hand Forced as Zimbabwe Starts Nationalization

CURRENCIES

EUROPEAN MARKETS

SPAIN – acts like le chien de Sarkozy; the IBEX continues to flash a major negative divergence vs Global Equities as of late (Spain -1.4% YTD w/ Germany +20%!); when your stock, currency (Euro), and bond markets are all falling at the same time – not good.

ASIAN MARKETS

ASIA – post the USA meltup in everything Apple and celebrations in Financials to a made-up test, Asia has basically been down for the last 2 days (Equities), with China and India leading the decline. Bulls were begging for India to cut rates last night and they didn’t (inflation), so the Sensex dropped -1.6% on that and snapped TRADE line support of 18,023, again. China’s FDI print was down -0.9% y/y – not good.

MIDDLE EAST

The Hedgeye Macro Team