This note was originally published at 8am on March 01, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“You have to choose not to spiral into hate.”

-Izzeldin Abuelaish

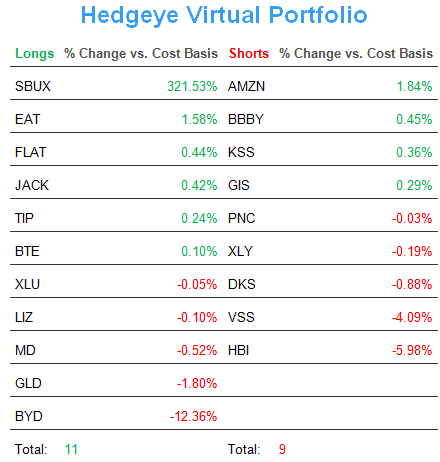

On red yesterday I took up my positions in US Equities and Commodities to 12%, respectively, buying Utilities and Gold in the Hedgeye Asset Allocation Model. I also sold my entire US Dollar position (9%) on green. Don’t hate me for moving fast. Sometimes that’s just what I do.

‘Trading, Fast and Slow’ might be a good title for a new book (or maybe just a high-frequency tweet). It uses 3 words that some people in our business love to hate. Trading? Oh no, “I’m not a trader, I am an investor.” Ok. Do you invest fast or slow? Do you manage risk? Yes, we know – you actually have to trade to answer both of those questions.

While plenty of people from The Old Wall are just punching the over-compensation clock at this point, I think we have entered the thralls of creative destruction. These are the most exciting times of my 13-year career. There is so much to Re-think, Re-work, and Re-build.

We have an entire industry that needs to be debated. Every process. Every premise. Every minute of every day offers you an opportunity to not only get in the game, but be the change we all want to see in this profession.

If that sounds a little speechy, it’s because it is. As Ray Dalio at Bridgewater likes to say, this business is all about figuring out the truth. In the final pages of Izzeldin Abuelaish’s ‘I Shall Not Hate’, he comments on the same principles of risk management in the Middle East:

“I’m not talking about the light of religious faith here, but light as a symbol of truth. The light that allows you to see, clear away from the fog – to find wisdom. To find the light of the truth you have to talk to, listen to, and respect each other.” (page 196)

The partisan politics, economics, and investing styles that have failed us over the last 5yrs are broken. Don’t Hate The Debate. Embrace change and progress. We can always do better. We always have.

Back to the Global Macro Grind…

One of the most heated debates I have with clients remains centered on the interconnectedness of the world’s reserve currency to market prices that are primarily denominated in that currency (US Dollars).

Since most of Western academia has not taught us to re-think markets this way, their dogma is now our dilemma. That’s why we need to slap on the accountability pants and hash this one out, fast. It’s time for the professors to be held accountable to the debate.

If you don’t think Fed Policy drives the US Dollar and Inflation/Deflation Expectations of assets priced in Dollars, try that theory at home with your own money. If the Fed were to even whisper about a rate hike, Oil and Gold would get hammered.

That’s why managing risk around big up/down moves in the USD is critical to getting Big Beta right. With the US Dollar Index up +0.8% on the day yesterday (one of its biggest up days of 2012), here’s what happened underneath the Globally Interconnected Market hood:

- Silver = down -6.9%

- Gold = down -5.5%

- Basic Materials (XLB) = down -1.9%

It’s a good thing the Dollar isn’t correlated to Apple.

Notwithstanding that the Chairman of the Federal Reserve didn’t mention the words (and hasn’t since 2006) CORRELATION RISK in his entire semi-annual testimony yesterday, we’re still not in the business of taking his word for it on what is or is not happening out there.

I know this is a touchy subject – particularly to the legions of Nobel Prize winners who get paid to be willfully blind to it. But this is America, not Russia. We, The People, have a fiduciary responsibility to hold central planners accountable.

Transparency, Accountability, and Trust?

- Transparency: Bernanke to Ron Paul yesterday on defining inflation - “I’ll talk to you about that offline”

- Accountability: Bernanke’s prepared remarks on his mandate for PRICE STABILITY -“as we expected, inflation was transitory”

- Trust: Bernanke on his forecasts – “my projections are considerably lower than last year”

Alrighty then.

- So there is no inflation because Bernanke chooses to define it with what’s just universally considered not true

- And as long as commodity markets oscillate between bubble and crash mode, price inflation/deflation is “transitory” and stable?

- And if you’re willing to take his word for it on forecasts that he’s had dead wrong, we can soft land this puppy perfectly

I really don’t hate the man. I Don’t Hate The Debate either. As an immigrant to what I genuinely felt was the last bastion of free-market of capitalism in the world, I just find being held hostage to an un-elected central planner who is obfuscating the truth un-American.

My immediate-term support and resistance ranges for Gold, Oil (Brent), Utilities (XLU), US Dollar Index, and the SP500 are now $1697-1735, $122.21-126.02, $34.74-35.68, $78.09-79.06, and 1363-1372, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer