This note was originally published at 8am on February 28, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“If we do not change our direction, we are likely to end up where we are headed.”

-Chinese Proverb

In my intraday risk management note yesterday titled “Higher-Highs”, I explained why I was buying/covering on red. Fifteen SP500 points higher (+1%), I was tweeting about why I was selling/shorting green up at 1371.

If we do not change our direction, we are likely to get run over.

Back to the Global Macro Grind…

Taking a step back, from a positioning perspective here’s what I’ve done since being bullish on everything US Growth and Consumption (pre Ben Bernanke’s Policy To Inflate, pushing US Dollar Debauchery out to 2014, on January 25th, 2011):

- Long Inflation

- Short Growth

Notwithstanding all of the single security mistakes I’ve made in the last month (11 losing positions out of my last 45), the obvious risk management lesson since January 25thhas been that perma-bulls and perma-bears rarely change direction – at least not quickly.

That’s the immediate-term. That’s also the rear-view mirror. Looking forward, what lessons have growth investors learned over the intermediate to long-term about the relationship between Inflation and Growth?

Until we get through month-end, I do not know the answer to that question. My sense is that there has not been much evolution in the risk management process over the course of the last 2 major growth slowdowns (2008 and 2011), so this time won’t be different.

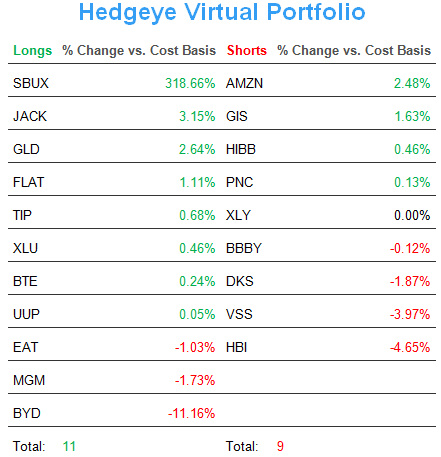

How am I positioning the Hedgeye Asset Allocation Model into month-end markups (February ends tomorrow):

- CASH = 52% (down from 91% on January 25th, before the US Equity market dropped for 4 consecutive days)

- FIXED INCOME = 24% (Inflation Protection and Growth Slowing – TIP and FLAT)

- COMMODITIES = 9% (Gold – GLD)

- INTERNATIONAL FX = 9% (US Dollar – UUP)

- US EQUITIES = 6% (Utilities – XLU)

- INTERNATIONAL EQUITIES = 0%

Taking these positions in order, here’s the what I am thinking as of this morning:

- CASH: when it’s my own money, it’s going to be a big position at 3yr highs in US Equities – that’s just how I roll

- TIP and FLAT: both positions are shining examples of Growth Slowing As Inflation Accelerates (same call I made last year)

- GLD: pushing into its 12 consecutive year of going up, this repudiation of Keynesian Economics still looks like my weight

- UUP: I just started buying US Dollars back in the last few days as a hedge against Japan’s massive debt maturities in March

- XLU: I swapped out of our long Financials (XLF) position yesterday at +13.7% YTD and into Utilities which are down -2.5% YTD

As for International Equities, having a 0% asset allocation at the top of a move is also plainly described as my mistake. We were long China coming out of the December 29th2-year low – and I sold too early. The good news is that we waited until February 16thto sell Chinese Equities (CAF) for a +15.11% gain. The bad news is that China has moved higher since (+11.4% YTD).

Changing direction when markets are Headed Higher is not easy. Neither is buying on red or selling on green. But this is what I do. The process is both malleable and repeatable. I wake up every morning looking forward to fresh opportunities, not dwelling on mistakes.

Some people in our profession don’t like to talk about their mistakes. Many of those people like to call me names my Mom wouldn’t like when I call out our successes. Sadly, this won’t change direction anytime soon either. It’s just the way some people are.

On pages 218-219 of “Thinking, Fast and Slow” in his chapter titled The Illusions of Pundits, Daniel Kahneman nails this difficult topic of success/failure to the boards: “…experts resisted admitting that they had been wrong, and when they were compelled to admit error, they had a large collection of excuses: they had been wrong only in their timing, an unforeseeable event…” etc.

Sound familiar?

Of course it does. Whether you have worked at 4 different hedge funds like I have, or whether this is your first wonderful experience chasing alpha at an asset management firm, you know exactly who the excuse makers are – their operating principles are very different than mine.

The best news I can give you is that it still isn’t too late. We can still Re-think, Re-build, and Re-work all that we do in this profession. Our collective policy, strategy, and capital mistakes provide tremendous opportunity for change. If I didn’t believe that deep down in my gut, I wouldn’t feel like our firm is Headed Higher this morning either.

My immediate-term support and resistance ranges for Gold, Oil (Brent), Utilities (XLU), Inflation Protection (TIP), Growth Slowing (FLAT), US Dollar (UUP), and the SP500 are now $1752-1798, $121.93-126.34, $34.72-35.41, $118.11-119.66, $58.01-59.65, $21.71-22.12, and 1358-1373, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer