Yesterday's press release confirms that PVH is indeed taking back the license for the ck Calvin Klein European apparel and accessories retail business from Warnaco in 2013 as originally announced last week. This may appear insignificant relative to the overall size of these businesses, but that’s not the case when you run through the numbers. In fact, this deal could provide a nice kicker to PVH earnings growth 3-4 years out to the tune of $8 in value added to PVH and $1 lost for WRC, which we don’t think the Street is focused on. As a result, this move is bullish for PVH and bearish for WRC over the near-term, though over the long-term we think this move is bullish for both.

This scenario is hardly new in retail, only the names and faces are different. WRC misses its minimum growth targets on the CK bridge line and underperforms. Then it loses the business because the licensee feels they can do better. Think JNY losing Lauren, Ralph, Polo Jeans and LIZ losing DKNY. Management teams always talk about the 'safety' of certain licensing agreements, but when a licensee is under pressure it will always invest in brands it owns, not licenses. We’ve seen this movie before. But here are some things to consider in this case:

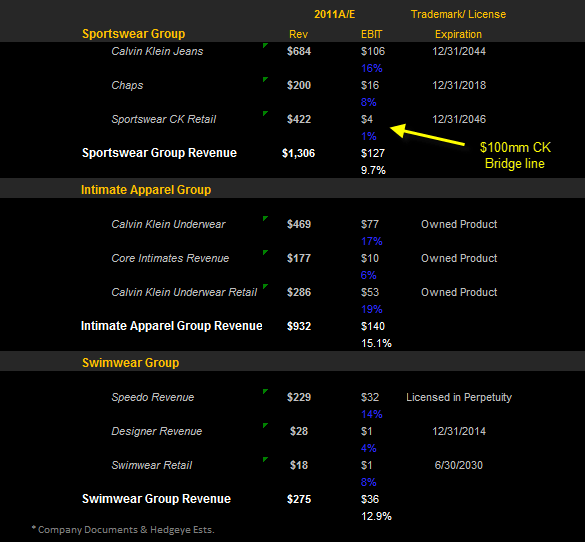

- For starters, the CK ‘bridge’ brand accounts for ~$100mm in revenues at breakeven for WRC including what is approximately a 7% royalty. That equates to ~4% of WRC’s total sales for 2011, which the company expects to largely replace with its CK Jeans business at higher margin. Take a look at the table below to see how this line stacks up to other CK licenses WRC operates for reference.

- Assuming a normalized profitability in the LSD range, the loss of this license could be sized at roughly $1 in value (which presumably is already in the stock).

- The bottom-line is that this deal won’t have much of an impact on WRC losing a breakeven business and if anything will be net positive as the company removes the distraction and focuses on investing in its own content.

- In addition to filling these stores with CK Jeans, WRC is likely to get more aggressive in growing its CK underwear line at retail, product it owns and doesn’t license and which accounts for ~50% of EBIT.

- At the aforementioned royalty rate of 7%, this business currently generates roughly $7mm in EBIT for PVH equating to ~$0.07 in EPS or 1% of PVH’s earnings. Bringing the line in-house should nearly double that out of the gate.

- PVH highlights the opportunity to grow this CK line to a $500mm business over the next 5-7 years, but it’s important to note that we shouldn’t think of this growth in a straight line. Typically, when licenses are bought back in, the business are grown far more aggressively in the early years. Recall when RL brought the Lauren and Ralph licenses back in from JNY back in 2003.

- So, let’s assume that when PVH brings this business back in-house in 2013 that it can get it close to $300mm by 2015 at 20% margin. That would equate to $0.60 in EPS. If we assume 25% margins, more in-line to the rest of PVH’s CK brand profitability, we’re looking at $0.75 in incremental EPS. With EPS over $9 in earnings power in 2015, that would take the CK ‘bridge’ line from 1% to accounting for nearly 8-10% of PVH’s earnings 3-4 years out, or about $10 in stock value at a 13x multiple. That equates to ~$8 in present value. A meaningful contribution to an $85 stock.we'd argue that this is probably not on the stock.

Like its doing with its Hilfiger licenses, if PVH decides to get more aggressive in taking control over its own content and driving growth at its CK business, it will have investors thinking about $10 in earnings power 4-5 years out providing further upside. Investors that missed the strategic importance and magnitude of this when RL first started buying in its licenses are likely to consider this as PVH embarks down this same path.

Casey Flavin

Director