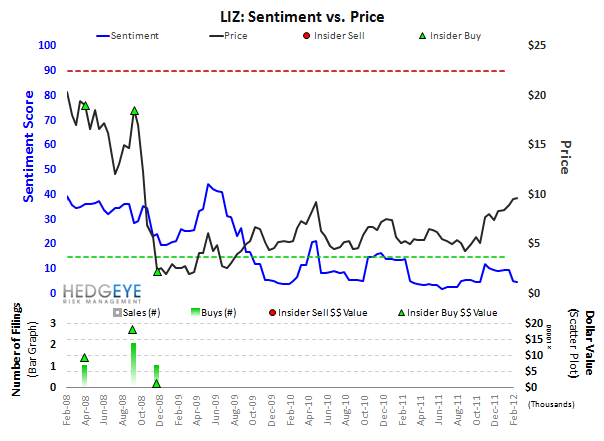

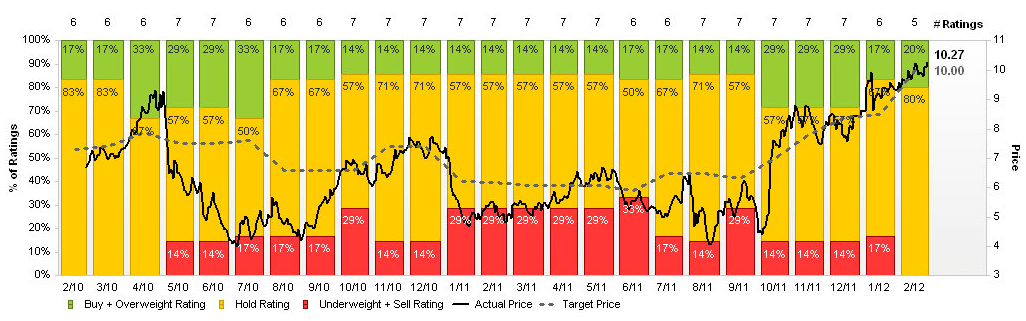

Conclusion: We like LIZ heading into and out of the upcoming quarter. There's no change to our view that LIZ could double again this year. Increasing clarity on company fundamentals and balance sheet will be an incremental positive this quarter. It’s also worth noting that short interest remains at ~25% of the float heading into the quarter and sentiment remains one of the weakest in retail despite a stock move from $5 to $10. That’s going to change as the stock moves from $10 to $20.

TRADE (3-Weeks or Less):

LIZ closes the book on 2011 after the close Wednesday when it reports Q4 results. With all of the moving parts during the quarter, earnings results are going to be secondary to balance sheet clarity and the latest on brand sales with nearly 2/3 of Q1 now in the books.

- To be clear, screens still suggest the company has ~$735mm in net debt instead of its current position of $270mm significantly overstating Enterprise Value at $1.7Bn instead of $1.3Bn and multiples.

- This point may seem small, but when the biggest overhang on the stock has been its leverage coupled with the reality that screens still play a key role in generating ideas, it should not be overlooked in terms of what we expect to be increasing interest in LIZ coming out of the quarter.

- At the brand level, initial sales at Juicy since the brands re-launch in February and the turn in profitability at Lucky will be key issues of focus on the call. The turn at Juicy is certainly going to take more than a few weeks of sales or even a quarter for that matter, but most that have seen the new line would agree that it’s an incremental upgrade.

- As for Lucky, we think the turn in profitability may not have materialized quite as expected in Q4, but the brand remains squarely positioned to turn profitable here in 2012.

- There’s been no shortage of positive commentary on the luxury handbag market from both department stores and brands alike and we expect no different here from Kate Spade. The key item to keep in mind here is the cadence of last year’s compares which were most difficult in January (+96%) before getting progressively easier in Feb (+87%) and March (+44%). With 2-year trends running in the 40%s-50%s, we fully expect a meaningful sequential comp deceleration, but this might catch newer investors by surprise.

- All in, we’re ahead of the Street at $0.14 vs. $0.07E and expect interest in the name to continue to build following the quarter.

TREND (3-Months or More):

Kate Spade continues to fire on all cylinders. In addition to 20%+ store growth and increased store productivity, Kate is the company’s key growth engine. Moreover, Lucky and Juicy are both at inflection points. While our positive take on LIZ is not predicated on a significant change here, it would provide an additional tailwind.

TAIL (3-Years or Less):

If the success of Kate Spade is any indication, Lucky and Juicy have a lot to look forward to under new leadership. The company will have its lumps along the way, but at current valuation you get Lucky and Juicy for free. Using both COH and KORS as a proxy, Kate alone could grow over 4x in the next 3-5 years.

After years of underperformance, the company has shed the weight and is now re-emerging as a growth stock with mid-teens revenue growth and expanding margins. Most investors have yet to realize the magnitude of this transformation. We think this stock is a double from here with an opportunity for significantly more upside.

Casey Flavin

Director