--Interbank risk continues to recede ahead of Wednesday's 2nd LTRO allotment.

Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor".

If you'd like to receive the work of the Financials team or request a trial please email .

Positions in Europe: Covered EUR/USD (FXE) and France (EWQ) today

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 3 bps to 65 bps.

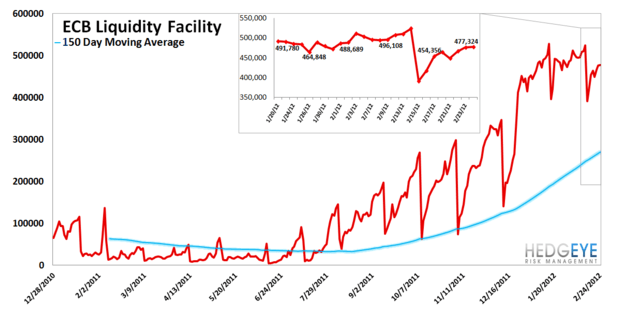

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

European Financials CDS Monitor – Bank swaps were tighter in Europe last week for 33 of the 40 reference entities. The average tightening was 4.8% and the median tightening was 1.0%.

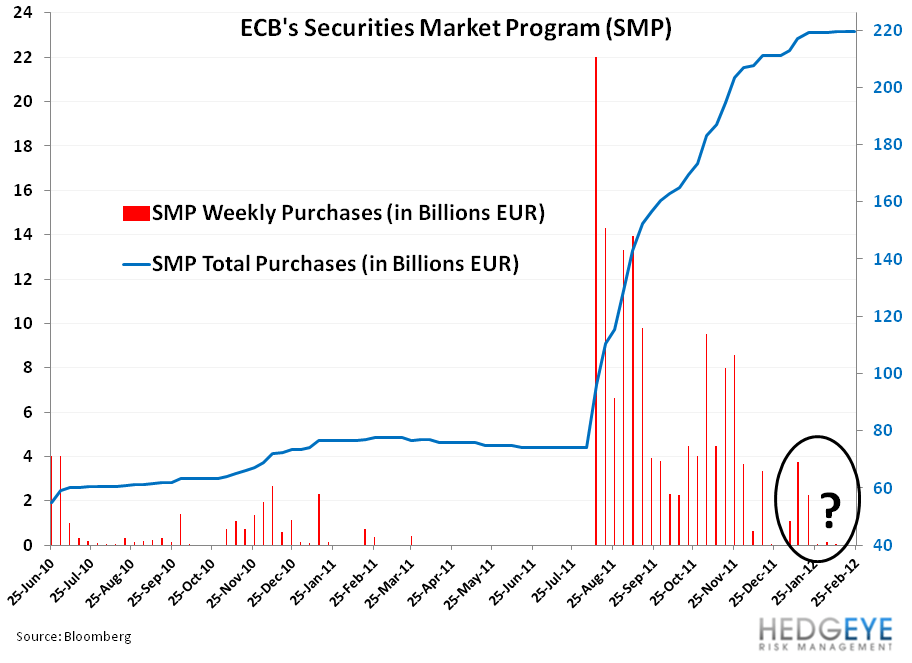

Security Market Program – For a second straight week the ECB's purchased no securities on the secondary bond market. In the last 5 weeks the Bank has only purchased €246 MILLION, versus €2.243 BILLION in the week ended 1/20 and 3.766 BILLION in the week ended 1/12, with the total facility at €219.5B. We continue to wonder if the ECB is making up the numbers and not reporting their purchasing. Here we welcome your thoughts.

Matthew Hedrick

Senior Analyst