This note was originally published at 8am on February 13, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The dominance of conclusions over arguments is most pronounced where emotions are involved.”

-Daniel Kahneman

Intraday on Friday we finally had a -1% down move in US Equities and a +1.5% up move in long-term US Bonds. So, I covered our short position in the SP500 (SPY) and sold our long position in US Treasuries (TLT) on that. Buy red, Sell green.

Buying on red and Selling on green? That’s meant to be an over-simplification of what it is that I do. I love saying it, tweeting it, and doing it – because actually finding it within me to do it when I have so many other risk management signals banging around in my head is quite difficult.

On page 103 of “Thinking, Fast and Slow” Kahneman compartmentalizes what’s happening in my little brain and reminds me that I am hostage to what his psychologist buddy, Paul Slovic, coined as “The Affect Heuristic.” It helps explain why “people let their likes and dislikes determine their beliefs about the world.”

Back to the Global Macro Grind …

At least in my own head, I’m crystal clear that I dislike Big Government Interventions, Socializations, and Regulations of free-market pricing. If all I did was trade on the Emotional Conclusions that are embedded in those thoughts, I’d be wrong a lot more than I am. Separating what should happen versus what is going to happen is critical in markets that whip around like this.

What whipped around last week?

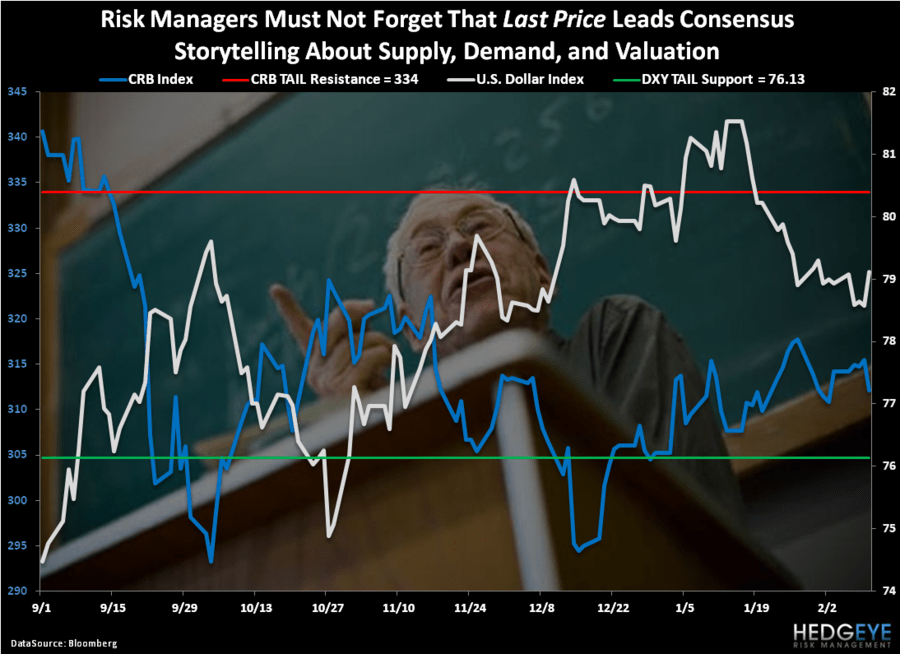

- The US Dollar Index finally stopped going down (1stup week in the last 4) = up +0.3%

- Commodity Inflation (18 component CRB Index) stopped inflating = down -0.6%

- US Equity Volatility (VIX) ripped to 20.79 = straight up +21.6%

What’s fascinating and sad about this all at the same time is that it reminds us how sensitive market prices are to a devaluation of the US Dollar. Emotional Conclusions drive expectations too. The US Dollar currently has an immediate-term +0.7 correlation to Volatility (VIX).

Emotional? Right before they stopped inflating, CFTC (Commodities Futures Trading Commission) data showed that in the week ended February 7th, 2012, money managers ramped up their net-long positions to commodity inflation by +13% week-over-week. At 929,199 contracts (Bloomberg.com), that’s the biggest net-long position since September of 2011. Atta boy Bernank!

For those of you who still remember who and what got crushed in September 2011, the CRB Index dropped from 343 to 293 by the first week of October 2011. That was a -14.6% vertical drop as the US Dollar Index ramped +7%. Got Emotional Conclusions about causality?

Or was that Correlation Risk? Or was it expectations? Or Europe?

Whatever it was, it was the real-time score.

That’s the thing about market prices. They could not care less about what you or I think. They do what they do when they do them, rendering our immediate-term opinions about valuation, supply, and demand useless.

We’re all book smart. Or at least, technically, that’s what the diplomas say. Being market-smart will be determined many years after we leave this game – when every week, month, and year of our risk management performance has been TimeStamped.

In the meantime, we need to know what we are going to do now. As in right now. Markets wait for no one. And now that the Greek “news” is out of the way, I think this week’s focus will turn to:

- Japan: nasty Keynesian Growth Slowdown (down -2.3% GDP Growth y/y for Q411) and pending sovereign debt maturity in March

- China: growth slowing (again) as global inflation expectations rise (again)

- USA: economic data to be reported this week which should already start to show inflating import, consumer, and producer prices

I’ve dropped the Cash position in the Hedgeye Asset Allocation Model from 91% on the day of Bernanke’s Policy to Inflate (January 25th, 2012) to 64% this morning. Effectively, I’m long Inflation Expectations Rising (Energy, Gold, etc.) and I’m right worried about it. If we see the US Dollar hold last week’s gains, I’ll have no problem selling inflated prices on green.

My immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, and the SP500 are now $1714-1761, $114.89-120.01, $1.31-1.33, and 1338-1360, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer