Positions in Europe: Short EUR/USD (FXE); Short France (EWQ)

Asset Class Performance:

- Equities: European equity performance fell largely in a band of -100 to +50bps week-over-week with some notable divergences. Top performers:Russia (RTSI) 4.4%; Romania 4.2%; Norway 1.7%. Bottom performers:Cyprus -19.3%; Greece -9.0%; Slovakia -1.8%; Poland -1.6%; Spain -1.5%; Portugal -1.0%.

- FX: The EUR/USD is up 2.38% week-over-week. Divergences:TRY/EUR -3.08%, ISK/EUR -3.05%, GBP/EUR -2.02%; PLN/EUR +0.46%. The RUB/EUR is up 6.10% YTD, one of the best performing major emerging market currencies against the EUR.

- Fixed Income: 10YR sovereign yields were down week-over-week, with Portugal bucking the trend to the upside. Portuguese yields climbed 50bps to 12.77% w/w, while Spain’s 10YR saw the biggest decline at -21bps to 5.05%. Greece fell -14bps to 34.24% and Italy fell -9bps to 5.48%

In Review:

How hard can you scrape the hull of a ship before it tears? The Eurozone churned for another week and with the less-than-exuberant reaction to Tuesday’s news that Eurozone finance ministers forged a €130 billion rescue deal for Greece and terms on PSI to reduce the country's outstanding debt by €107 billion, it’s clear that few think this “deal” provides the nail to shore up Greece’s sovereign and banking imbalance and therein right the Greek economic ship.

The main issue is that there are still so many question marks ahead, not unlike past weeks and months. One central issue concerns PSI. If not enough bondholders agree to the terms—and the agreement assumes 95% participation on a haircut of 53.5% of the principal value of the bonds with an average coupon of 2.63% for the first 8 years and then 3.65% for the balance of the 30 year maturity—a significant legal battle could be waged between parties. And already in the weeds is discussion that the ECB, on its own and without judicial or parliamentary review, swapped its Greek debt for new Greek debt that is not subject to any collective action clauses (CACs). Obviously this “changing of the goalposts”, if substantiated, has severe negative implications on the success of participation and future issuance from other sovereigns.

Second, select Eurozone member parliaments still need to vote on the terms of the rescue fund and PSI package, with Germany’s vote coming on Monday, February 27. While it is expected to pass in Germany, it is not a guarantee, and more broadly the process to bring these measures to vote across countries simply runs final ratification closer to Greece’s €14.5 billion bond repayment coming due on March 20.

Announcements from the IMF this week also dampened sentiment, including a statement that the balance of risks in this "accident-prone" economic program is "mostly tilted to the downside, and “even a small shock could see the country's debt growing on an ever-increasing trajectory.” Further, the downgrade from the European Commission of Eurozone GDP to -0.3% in 2012 versus a previous estimate of +0.5% muted the agreement talks.

The bull camp however turns to the 2nd installment of the LTRO allotment of 36M paper that will be rolled out. We continue to caution that though this may help solve the liquidity crisis, it does little for underlying solvency issues at banks. Additionally, we’ve seen few indications that lending is picking up material. The chart below under “Charts of the Week” shows that these LTRO funds could simply be contributing to the elevated levels of the ECB’s overnight deposit facility.

Finally, another disturbing trend (however not new) is money deposits leaving southern Europe for Germany and points north. Bloomberg recently compiled this data and found that deposits in Greece, Spain and Italy shrank 28% from a peak in June 2009, as deposits climbed 10% since May 2010 (when Greece received its first bailout).

Below is a calendar of critical catalysts to be aware of:

This Weekend (2/25- 2/26): G20 Finance Ministers Meeting in Mexico City. Decision on IMF loan of €500B is expected.

Wednesday (2/29): 2nd 36-Month LTRO Allotment.

Wednesday (2/29): Eurogroup Meeting to sign the previously endorsed agreement between the 17 members on the Treaty for the European Stability Mechanism.

Thursday and Friday (3/1-3/2): Signing of the Fiscal Compact by 17 Eurozone leaders together with the non-euro area leaders of countries willing to join. Further, the group will reassess the adequacy of resources under the EFSF and ESM rescue funds.

Call Outs:

- The European Commission said it now expects the Eurozone economy to shrink by -0.3% in 2012, versus a previous forecast of +0.5% in November, with the region undergoing a "mild recession".

- EU may give countries such as Spain softer deficit targets but there will be no let-up in the overall austerity drive as the continent struggles to draw a line under its two-year debt crisis.

- Russia - Prime Minister Vladimir Putin will probably win Russia’s presidential election in the first round on March 4, according to the latest projection from the independent Levada Center. Putin has the support of 66% of decided voters versus 15% for Communist Party leader Gennady Zyuganov, said Lev Gudkov, Levada Center’s director.

Portfolio Positions:

Short France (EWQ) – Keith opportunistically shorted France on 2/22 and again today (2/24) in the Hedgeye Virtual Portfolio as we got our price on a backdrop of weak fundamentals and data and an uncertain political climate that is trending towards a socialist candidate victory in the upcoming Presidential elections (in April) that could spell higher taxes and more spending.

French consumer confidence did climb for a second straight month in February one point to 82, according to a poll from the national statistics office Insee, however there are material signs that in 2012 France will be butting up against higher unemployment, a debt load of over 90% of GDP, stretched deficit targets, and uncertainty around cost saving measures (austerity) and associated revenues given the uncertainty of who will be leading the state in the weeks ahead: Sarkozy or his challenger, the socialist Francois Hollande.

While Hollande talks about fiscal consolidation, he’s indicated that he may undo Sarkozy’s rise in the pension age, has questioned the EU’s fiscal compact, is unclear on his position on Eurobonds, and may well be a bigger spender than saver of government money. Clearly there are many unanswered questions here, but we think the risk lies to the downside.

Returning to the data, this week showed that the number of people in France actively looking for work made its highest high since the Euro went into circulation, to 2,861,700 in January versus 2,848,300 in December. This should put upward pressure on last year’s 5.6% unemployment rate. This week’s initial February PMI data also showed that Services underperformed expectations coming in at 50.3 (vs 52.0), which Manufacturing beat expectations at 50.2 (vs 49.0), as both run along the contraction/expansion line of 50.

Short EUR/USD (FXE) - Keith shorted the EUR/USD via the eft FXE on 2/23 and again today (2/24) in the Hedgeye Virtual Portfolio, after watching the pair rise from $1.30 earlier this week through $1.33 and then up to $1.34, the line in our quantitative model signaling overbought on the intermediate term TREND, prompting the decision to short. We think that despite optimism around the Greek deal we see a long tail ahead to shore up Greek and Eurozone sovereign and banking imbalances.

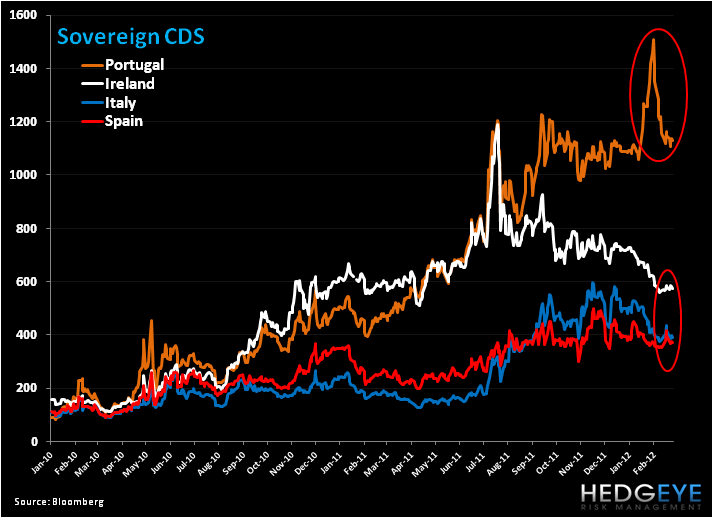

CDS Risk Monitor:

On a week to date basis, CDS was largely down across European sovereigns (vs up last week), with Spain leading the charge on the downside -28bps to 370bps, followed by Italy (-25bps) to 391bps and Portugal (-19bps) to 1130 (see charts below).

Charts of the Week:

Really? In the chart below we show the secondary bond purchasing program of the ECB, known as the Securities Market Program (SMP). Last week the ECB did NO buying, and combining the last 4 weeks the Bank has only purchased €246 MILLION, versus €2.243 BILLION in the week ended 1/20 and 3.766 BILLION in the week ended 1/12, with the total facility at €219.5B. We continue to wonder if the ECB is making up the numbers and not reporting their purchasing. Here we welcome your thoughts.

The ECB’s Overnight Deposit Facility remains elevated. Thank you LTRO?

The European Week Ahead:

Monday: Jan. Eurozone Money Supply; Germany Bundestag will vote on new Greek Aid Package; Feb. UK Nationwide House Prices (Feb 27-29); Feb. Italy Business Confidence

Tuesday: Feb. Eurozone Consumer Confidence – Final, Business Climate Indicator, Economic, Industrial, and Services Confidence; Mar. Germany GfK Consumer Confidence Survey; Feb. Germany Consumer Price Index – Preliminary; Feb. Italy Reported Sales, GfK Consumer Confidence Survey

Wednesday: Eurozone Second LTRO Allotment; Jan. Eurozone CPI; Feb. Germany Unemployment Change, Unemployment Rate; Jan. Germany Import Prices; Jan. UK Net Consumer Credit, Money Supply, Mortgage Approvals, Net Lending Sec. on Dwellings; Jan. France Consumer Spending

Thursday: EU Leaders Meet in Brussels (Mar 1-2); Feb. Eurozone PMI Manufacturing – Final, CPI Estimate; Jan. Eurozone Unemployment Rate; Feb. Germany and France PMI Manufacturing – Final; Feb. UK, Russia, and Italy PMI Manufacturing; 4Q France Unemployment Rate; Feb. Italy CPI – Preliminary, Budget Balance; Jan. Italy Unemployment Rate - Preliminary

Friday: Jan. Eurozone PPI; Jan. Germany Retail Sales; Feb. UK PMI Construction; 2011 Italy Deficit to GDP, Annual GDP

Extended Calendar Call-Outs:

27 February: The German Bundestag plans to vote on the issue of Greece’s second bailout, including the embedded terms of the PSI.

25-26 February: G20 Finance Ministers Meeting in Mexico City. Decision on IMF loan of €500B is expected.

29 February: 2nd 36-Month LTRO Allotment.

29 February: Eurogroup Meeting to sign the previously endorsed agreement between the 17 members on the Treaty for the European Stability Mechanism.

1-2 March: Signing of the Fiscal Compact by 17 Eurozone leaders together with the non-euro area leaders of countries willing to join. Further, the group will reassess the adequacy of resources under the EFSF and ESM rescue funds.

20 March: Greece’s €14.5 billion Bond Redemption due.

April: French Elections (Round 1) begins to conclude in May.

April: Greek Presidential Elections

30 June: Deadline for EU Banks to meet €106 billion capital target/the 9% Tier 1 capital ratio.

1 July: ESM to come into force.

Matthew Hedrick

Senior Analyst