Distortions in the Seasonal Adjustment Factor

After our claims post last week, "The Ghost of Lehman," we had a number of clients ask us if we could quantify the effect we discussed. Lehman's Ghost is a distortion in the seasonal adjustment factors that the Department of Labor is using to treat jobless claims arising from the shock in the series in late 2008 - early 2009. The Labor Department uses a five-year lookback in constructing its seasonal adjustment factor, which means that the '08-'09 shock continues to skew the data. Essentially, the seasonal adjustment sees the increase in claims in September 2008 - February 2009 and reads it as a seasonal factor rather than as a bona fide shock.

To estimate the extent of the distortion from the seasonal factor on this week's data, we examined the YoY increase in NSA claims in February 2009 (+88%) and then backed out the average YoY growth from September 2008 to February 2009 (+60%). So the February 2009 growth is 28% above trend, YoY. This should be a rough approximation of the contribution of the seasonal factor from that year. Since the overall seasonal adjustment takes a five-year average, we divide this number by five to get a 5.6% increase. The conclusion is that this week's claims data is 5.6% understated. Instead of being 351k, it should really be 372k.

What's Next?

This week of the year captures the maximum benefit from the distortion - i.e. claims are understated in the last weeks of February by the largest amount. From now through May, the understatement disappears. Absent an underlying trend in the series, this effect would drive claims higher by about 20k over the course of the next three months. By July, the distortion reappears, this time as an overstatement, pushing claims slightly higher still. From July through year-end, the distortion disappears, and the underlying trend will be reflected in the weekly data.

Over the last year, claims have generally moved lower YoY (NSA) by around 10%. Off of a base of 350-400k, this implies 35-40k improvement this year, or around 3-4k per month. This underlying trend is thus overwhelmed by the distortion for the next few months (as true improvement is masked by the understatement/tailwind reversing).

This Week

The headline initial claims number rose 3k WoW to 351k (staying flat after a 3k upward revision to last week’s data). Rolling claims fell 7k to 359k. On a non-seasonally-adjusted basis, reported claims fell 20k WoW to 345k.

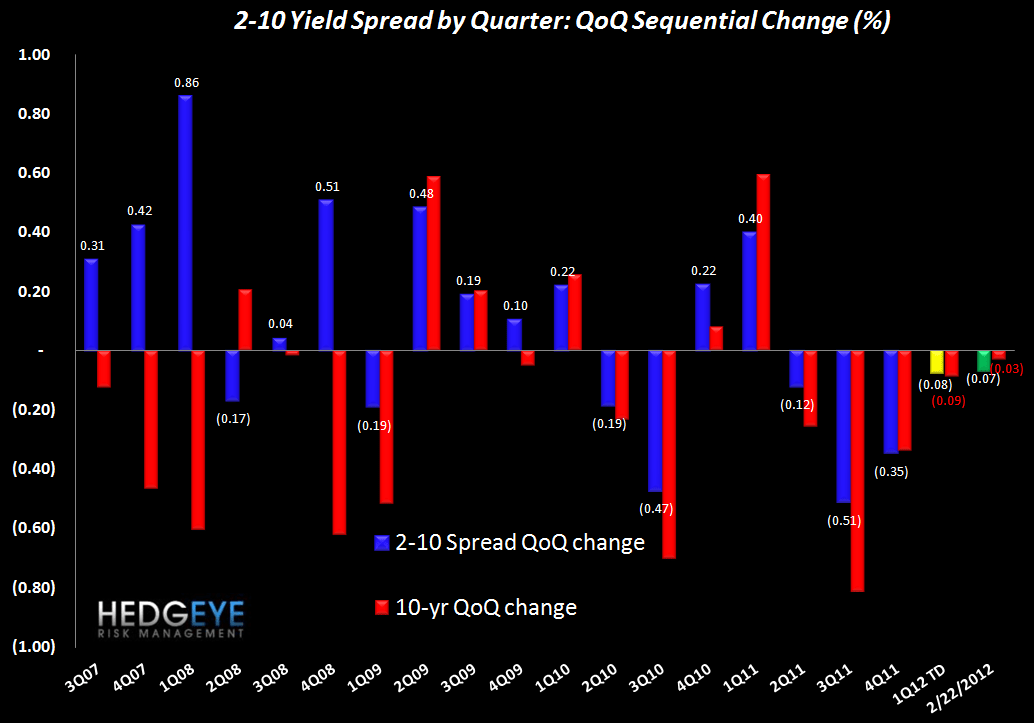

2-10 Spread

The 2-10 spread widened 5 bps versus last week to 170 bps as of yesterday. The ten-year bond yield increased 7 bps to 201 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link below to view in your browser.