This note was originally published at 8am on February 08, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“I would think we do a Quantitative Easing 3 if the Dollar gets too strong.”

-Larry Fink

Wow. Larry Fink is the CEO of Blackrock – they run $3.5 Trillion in client assets – and after a +101% move in US stocks from the 2009 low, he told Bloomberg yesterday that “investors should be 100% in Equities.”

Game on.

Fink is probably a good guy. We probably have a few things in common too. For one, we both started our careers at First Boston. He eventually ran their bond department. I eventually left.

Evidently, one thing that we do not have in common is the concept of Wall St 2.0 Global Macro Risk Management. There’s tremendous responsibility in being trusted with real-time recommendation. Time and price really do matter. With my own money, I’d never be 100% in anything – never mind stocks, after their best start to a year in decades.

The other thing Fink and I don’t have in common are political aspirations. He’d like to replace Geithner as head of the Treasury. I’d rather be a one-legged duck swimming in a circle.

When you consider the aforementioned currency quote within the context of where some of this country’s thought leaders are relative to my Strong Dollar = Strong America vote, Fink and I are not even in the same area code of having a debate.

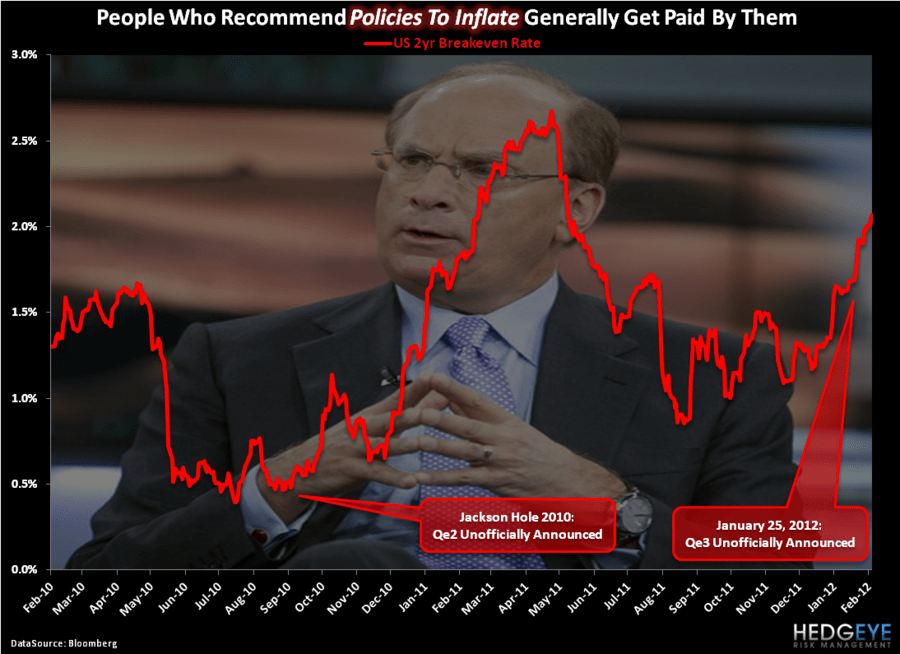

Is my opinion Too Strong? After testing 40-year lows during Qe2 of last year, was the US Dollar Too Weak? Is Larry Fink’s view of arresting gravity and not letting America’s currency trade at its non-Fed intervention free-market price Too Strong?

So many critical questions. So little time left.

Back to the Global Macro Grind…

With Santorum sweeping 3 states last night, President Obama’s probability of re-election (Intrade contracts) are going up and the US Dollar Index is going down. It sounds like Fink’s goal in advising Obama will be to keep the Dollar down. I guess if you’re in the business of seeing asset prices inflate, that makes some sense.

But does it make sense for American Savers and Consumers?

You tell me. I’m already telling you what I think. It’s no different than what I thought when Larry Fink was bullish on US Equities in February of last year. US Dollar Debauchery drives inflation. Inflation slows real GDP growth.

Now if you take Bernanke or the US government’s word for it, we don’t have inflation. Notwithstanding the fact that Bernanke cites a US inflation calculation that has been changed 9x since 1996, the “deflator” in this past quarter’s US GDP report was only 0.4%.

What does that mean?

- Q4 US GDP Growth for 2011 was reported at 2.75%

- Q4’s “Deflator” (you subtract inflation from the reported number for a real GDP #) was 0.39%

- With Consumer and Producer Price inflation running 10x that 0.39% “deflator”, US GDP was grossly overstated

I don’t use the word “grossly” very loosely. Neither does Clarium Capital’s Peter Thiel use the word “fraud” casually. Last night, like two non-Keynesian ships in the night, Thiel (founder of Pay Pal) and I were on separate sides of Yale University’s campus hosting spirited discussions with students and faculty about the alternative debate to currency debasement (he called Keynes a fraud).

Back to these feisty little critters called Inflation Expectations that slowed US GDP Growth in its tracks at 0.36% in Q1 of 2011 (yes, before the Europe that every guy who was wrong on his 2011 US GDP forecast by 60-80% blamed), here are some facts:

- US stocks haven’t had 1 down day of more than 0.57% in 2012 YTD (yes, stock prices are inflating)

- Brent Oil is trading at $116.35/barrel this morning = up +6.5% since Bernanke debauched the US Dollar on January 25th

- Gold has gone from $1622 on the morning of January 25th(pre FOMC statement) to $1749 this morning = +7.8%

If someone wants to explain to me that markets aren’t expecting the Chairman of the Federal Reserve to inflate, I’m ready to debate them in any public forum – any time, any place.

Russian stocks (driven by expectations of Petro-Dollar prices = Dollar Down, Oil Up) are up another +1.3% and up +19.5% YTD! Both the central banks of Australia and South Korea have come out in the last 48 hours and said no more rate cuts with inflation running higher. India, who is highly dependent on foreign oil, just saw its yield curve go back to flat as inflation expectations ramped.

I could (and do) go on, and on, and on about this … because the data that supports it does…

The bottom line is that people who get paid (including me because I am long Energy (XLE) and Gold) by inflation expectations rising are the same people who generally say there is no inflation.

Calling that out for what it is isn’t Too Strong. It’s called the truth. Respect and leadership in America isn’t allocated by your title. Its earned each and every day. There may be bailouts for people losing client capital. But there is no bailout for losing credibility.

My immediate-term support and resistance ranges for Gold, Oil (Brent), EUR/USD, US Dollar Index, and the SP500 are now $1736-1766, $112.71-116.85, $1.30-1.32, $78.59-79.09, and 1327-1354, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer