In the near term, strong same-store sales trends are maintaining sentiment around the stock and for that reason we do not hold a view on the short term TRADE (3 weeks or less) duration. The TREND and TAIL are less convincing for us and, we believe, investors are going to be more adamant in their demands for disclosure as time goes on. We see this already happening; when the press release hit this morning, the stock reacted strongly in the premarket before reversing during the earnings call at 8 a.m.

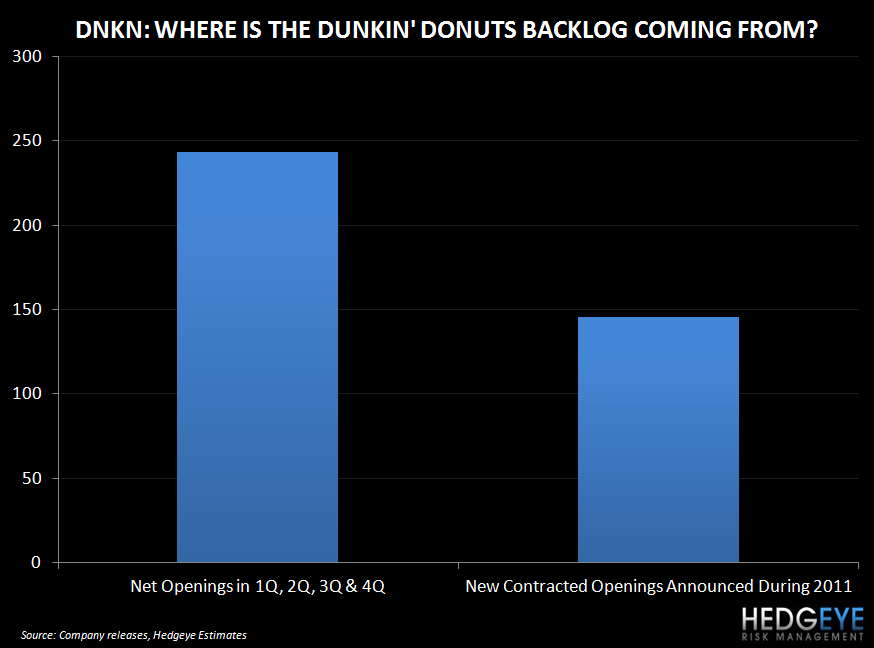

Dunkin' Brands makes more money by opening a new store than it does from an incremental 1% in same-store sales. Dunkin’ Donuts, its primary source of revenue, is heavily franchised and for that reason we are far more interested in its backlog of prospective new unit openings and franchisee commitments than we are in comps when assessing the viability of the company’s growth plans. In 4Q11, the company opened 120 new Dunkin’ Donuts stores and announced 25 new franchise commitments. In the absence of disclosure from management on this, we can only deduce that the backlog is declining.

A friend in the analyst community did ask specifically about this and the response he got was that the backlog is “growing”. If there is not issue around the topic – and it would certainly be a positive for the stock – why not disclose the details? We will remain skeptical until we see the numbers.

EARNINGS CALL NOTES

Dunkin' Donuts' U.S. (70%+ of consolidated revenues):

- 7.4% same store sales in 4Q11

- Increased marketing – in 2011 the number of weeks on national TV doubled versus 2010

- Breakfast sandwiches drive higher average ticket - in Q4 the Smoked Sausage Breakfast Sandwich was offered nationally as a limited time offer

- Driving lunch with the bakery sandwich platform - chicken and tuna salad sandwiches along with the new Texas toast grilled cheese sandwich in December

- Began selling Dunkin' Donuts K-Cups halfway through 3Q11 – in 4Q11 K-Cups represented a little less than 30% of our total comp increase

- Dunkin' Donuts and Baskin-Robins as well benefited from the warmer weather in 4Q11

- Signed a long-term agreement with our Dunkin' Donuts franchisee owned procurement and distributions co-operative - impact will be the greatest of franchisees in new markets where we estimate we will see between 200 and 300 basis-point reductions in food costs

- Franchisees opened 120 net new restaurants for a total of 243 net new restaurants in 2011. More than 80% of these restaurants are outside our core markets, and more than 90% of new developments were with existing franchisees

- Additionally, our franchisees completed 248 remodels during the quarter for a total of 636 in 2011

International

- Announced that Giorgio Minardi has joined us as President of International for Dunkin' brands

- The new Baskin-Robbins international store design is in more than 200 stores in the Middle East, Singapore, Russia, Canada, Korea and China. Management is focused on China

- Operating income was impacted by an $18.8 million impairment charge related to the company's investment in the South Korea joint venture. Management said that "the Dunkin' Donuts Brand had a challenging year in Korea and we are working with our joint venture partners to help them to improve the performance of the business."

GUIDANCE

- Dunkin' Donuts U.S. business comp store sales growth to be in the 3.5% to 4.5% range during 2012

- Baskin-Robbins U.S. business comp store sales growth to be flat to 2%

- Management is not providing guidance on the international comps in 2012

- Expect to open between 550 and 650 net new units globally

- Expect to open 260 to 280 net new Dunkin' Donuts restaurants in the U.S.

- Close between 60 and 80 Baskin-Robbins locations in the U.S.

- Franchisees will remodel between 600 and 650 Dunkin Donuts U.S. restaurants

- Plan to open between 350 and 450 net new units between Baskin-Robbins and Dunkin' Donuts internationally - weighted toward Baskin-Robbins.

- Revenue growth for 2012 is expect to be in the 6% to 7%

- “Adjusted” operating income growth in the 10% to 12% range

- Grow revenue at roughly twice the rate of expenses

- Guidance of adjusted operating income margin of 45% to 46% and this is all off a 52-week base in 2011.

- Guidance of adjusted earnings per share between $1.19 and $1.23 for fiscal year 2012.

- 2012 share count is expected to be $122 million.

- Generate between $100 million and $110 million in free cash flow

DNKN provides very detailed guidance on a number of business metrics just not the one that drives the long term growth of the company – the backlog of franchise store openings. Again, the company opened 120 net new Dunkin’ Donuts stores in 4Q11 and announced only 25 new franchisee commitments.

In the short run we would expect to see the potential for a future dividend and/or a share repurchase announcement to serve as a catalyst for some activity on the long side. On the call, management indicated that it is does not plan to deploy excess FCF to pay down debt. Having said that, until further notice we are contending that the back log is declining and the long-term growth story – as yet – does not warrant a premium multiple.

Howard Penney

Managing Director

Rory Green

Analyst