Positions in Europe: Short EUR/USD (FXE)

Asset Class Performance:

- Equities: European indices were up across the board for a third straight week, with a strong outperformance from Eastern Europe week-over-week. Top performers: Denmark 7.7%; Russia (RTSI) 5.4%; Ukraine 5.1%; Romania 5.0%; and the Czech Republic 4.3%. Bottom performers: Cyprus -2.1%; Slovakia -2.0%.

- FX: The EUR/USD -0.6% week-over-week. Divergences: PLN/EUR +1.3%, HUF/EUR +0.9%, CZK/EUR +0.7%

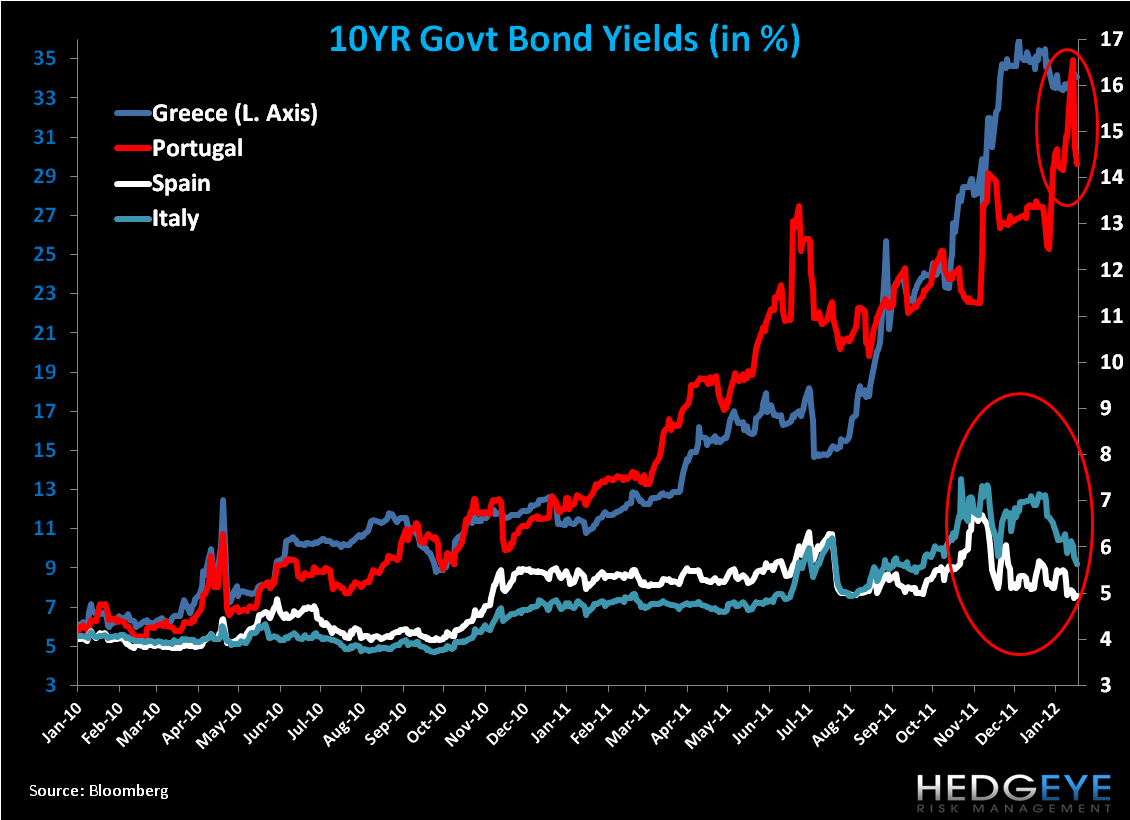

- Fixed Income: 10YR sovereign yields broadly decreased w/w, with Portugal leading the charge, down -57bps to 14.3%.

In Review:

***Ach Ja… So where have we really gone in the last week? We saw another strong week-over-week performance across the region’s equity markets, had another week of indecision on Greek PSI, and saw headline risk rule capital market daily performance—not unlike many days in the last two years. Portuguese risk appeared front and center early in the week (see why in last week’s Monitor), pushing yields on the 10YR up to as high as 17.4% on Monday after which the yield moderated -300bps. There’s increased “hope” in the LTRO, include the second 36M allotment to be issued on February 29th, and bullish sentiment around the fiscal compact that is to be signed on March 1-2 (more below). We think the market may be overly bullish on both events.

While the LTRO will provide needed liquidity, we’ve yet to see data indicating lending upticks (much is still being parked overnight with the ECB), and banks still have a long way to go to write down assets and raise capital into the July 1st deadline. To the fiscal compact we maintain that countries will not give up their sovereignty to Brussels (or Berlin), which will leave the underfunded EFSF + ESM facilities vulnerable. We saw evidence of the sovereignty issue early in the week with Germany floating the idea of establishing a budget overseer to have strict control and veto power over Greece’s fiscal policy decisions going forward (tantamount to the fiscal compact) in return for bailout funds. Greece’s Finance Minister Venizelos adamantly rejected this plan and warned that “anyone who puts a nation before the dilemma of economic assistance or national dignity ignores some key historical lessons.”

We’d expect fits of optimism follow by selling pressures across equity markets, not unlike our outlook for the EUR/USD that may be range bound until we see any material policy moves to initiate an inflection. The ECB’s SMP bond purchasing program remains an important indicator. Surprisingly there was very little buying last week (€63MM) despite very positive bond auctions across key peripheral countries. We saw a similar trend of successful auctions this week, which will make Monday’s data critical. Could the SMP in fact be stepping back? Are banks picking up the slack? We’re not convinced on either front.

Data this week showed an uptick in Services and Manufacturing PMIs across most countries, with Ireland showing a negative divergence. While Eurozone inflation has come in, unemployment remains sticky at 10.4% [of course considerably higher across the periphery and for the youth (between to 20-50%)], and fiscal consolidation is taking its toll on confidence, spending, and more broadly economic output. We expect the BOE to increase asset purchases (between 50-75B GBP) to mitigate some of the blow the economy has taken when it meets on Thursday. Conversely, data out of Germany continue to be positive, which has helped propel the DAX to 14.7% year-to-date and yields on its 10YR around 1.83%.

Call Outs:

- A Greece government official said that talks with the troika are basically completed but a few sticking points remain centered around wages, supplementary pensions and the recapitalization of banks. There was talk that a PSI deal was close and the latest terms being floated call for a 72% haircut, 3.6% coupon + GDP warrant, and no ECB participation. Nothing is official yet, but a statement is expected for Monday.

- Spain gives banks an extra year to recognize losses if they agree to merge with other lenders. (lenders have ~ €175 billion of troubled real-estate assets.)

- 1 year to make €50 billion of provisions against real-estate assets.

- If they agree by the end of May to merge, they get a further 12 months to take the charges and can tap the state’s bank-bailout facility for funds.

- The government will make banks increase the ratio of provisions set aside for land to 80 percent from 31 percent, de Guindos said. For unfinished developments, the provisioning level will rise to 65% from 27% and to 35% for assets including finished developments and houses.

Key European Data:

Eurozone CPI Estimate 2.7% JAN Y/Y vs 2.7% DEC

Eurozone Unemployment Rate 10.4% DEC vs 10.4% NOV

Eurozone PPI 4.3% DEC Y/Y (exp. 4.3%) vs 5.4% NOV [-0.2% DEC M/M vs 0.2%]

Eurozone Retail Sales -1.6% DEC Y/Y (exp. -1.3%) vs -1.5% NOV [-0.4% DEC M/M (exp. 0.3%) vs -0.4%]

Manufacturing PMI (JAN vs DEC):

France 48.5 vs 48.9

Germany 51 vs 48.4

Eurozone 48.8 vs 46.9

UK 52.1 vs 49.7 (exp. 50)

Italy 46.8 vs 44.3 (exp. 45.3)

Denmark 54.3 vs 59.4

Russia 50.8 vs 51.6

Ireland 48.3 vs 48.6

Sweden 51.4 vs 48.9 (exp. 49.5)

Hungary 49.8 vs 48.6

Poland 52.2 vs 48.8

Turkey 51.7 vs 52.0

Norway 54.9 vs 46.6 (exp. 48)

Spain 45.1 vs 43.7

Czech Republic 48.8 vs 49.2

Switzerland 47.3 vs 49.1 (exp. 51.2)

PMI Services (JAN vs DEC):

Eurozone 50.4 JAN F (exp. 50.5) vs 48.8 DEC

Germany 53.7 JAN F (exp. 54.5) vs 52.4 DEC

France 52.3 JAN F (exp. 51.7) vs 50.3 DEC

UK 56 (exp. 53.3) vs 54

Italy 44.8 JAN (exp. 45.4) vs 44.5 DEC

Russia 56.5 vs 53.8

Ireland 48.3 vs 48.4

Spain 46.1 vs 42.1

Eurozone Composite 50.4 JAN F (exp. 50.4) vs 48.3 DEC

Positives (+)

Eurozone Business Climate Indicator -0.21 JAN (exp. -0.25) vs -0.32 DEC

Eurozone Consumer Confidence -20.7 JAN FINAL (exp. -20.6) vs -21.3 DEC

Eurozone Economic Confidence 93.4 JAN (exp. 93.8) vs 92.8 DEC

Eurozone Industrial Confidence -7.2 JAN (exp. -6.8) vs -7.2 DEC

Eurozone Services Confidence -0.6 JAN (exp. -1.6) vs -2.6 DEC

Germany Unemployment Rate 6.7% JAN (exp. 6.8%) vs 6.8% DEC

Germany Unemployment Chg -34K JAN (steepest decline since Mar 2011 to 2.85 million) vs -25K DEC

Negatives (-)

Spain Q4 GDP 0.3% Y/Y vs 0.8% in Q3 [ -0.3% Q/Q (exp. -0.3%) vs 0.0% in Q3]

Italy Business Confidence 92.1 JAN vs 92.5 DEC

RATES:

(2/2) Romania Interest Rate CUT 25bps to 5.50%

(2/2) Czech Repo Rate UNCH at 0.75%

(2/3) Russia Overnight Deposit Rate UNCH at 4.00%

Russia Overnight Auction-Based Repo UNCH at 5.25%

Russia Refinancing Rate UNCH at 8.00%

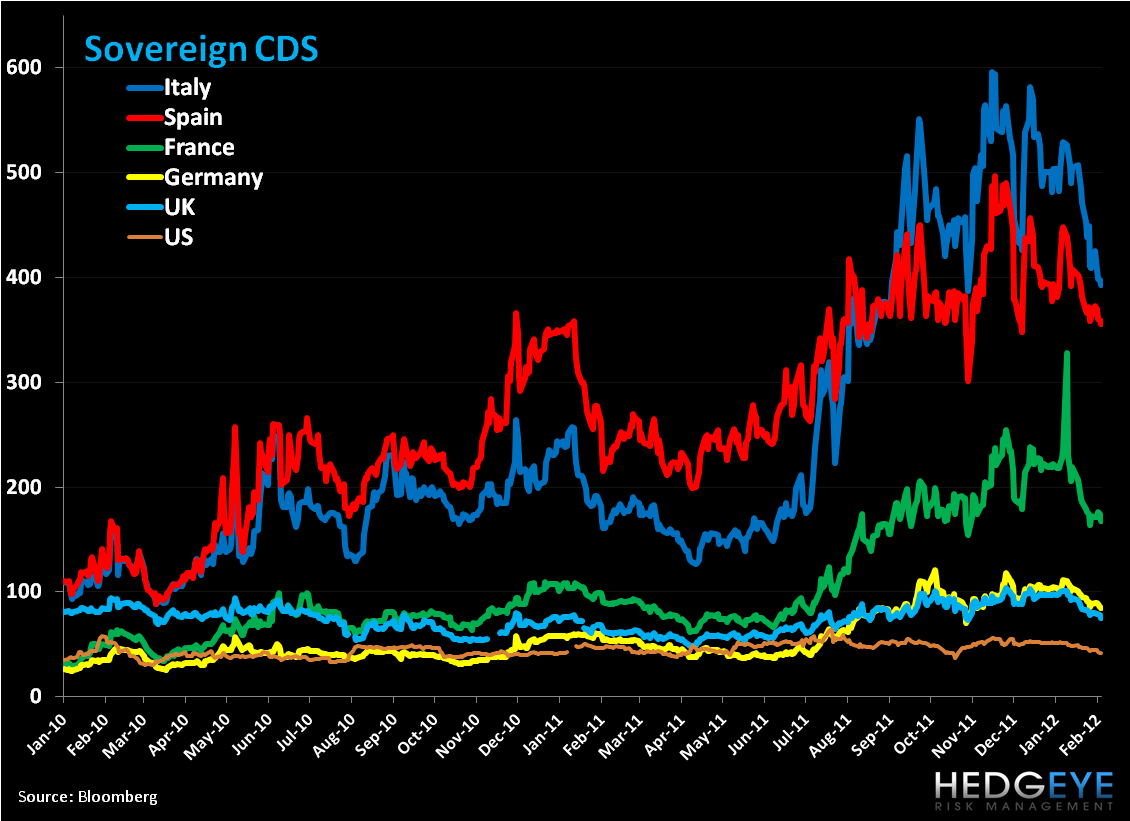

CDS Risk Monitor:

On a w/w basis, CDS was largely down across European sovereigns, with Portugal leading the charge, down -87bps to 1,333bps. Ireland saw the next largest drop at -40bps to 583bps (see charts below).

EUR-USD:

Keith shorted the EUR/USD via the eft FXE on 1/19 in the Hedgeye Virtual Portfolio with the price bumping up against our immediate term TRADE resistance level of $1.29. This is a position we’re monitoring closely given the extreme headline risk moving the pair.

Fiscal Compact:

Below we’ve copied the main points issued from Monday’s EU Summit concerning the fiscal compact. The full issue can be found here: http://www.scribd.com/doc/79957011/Fiscal-Compact-Treaty

First: we agreed and endorsed the fiscal compact, a treaty on stability and convergence in

the Economic and Monetary Union. The 17 euro leaders will sign it at our next meeting in

March (1-2), together with the non-euro area leaders of countries willing to join. The Treaty is

all about more responsibility and better surveillance. Every country that signs it commits to

bringing in a "debt brake" or "golden rule" into its own legislation, and will do so at

constitutional or equivalent level. New voting rules and an automatic correction

mechanism will enforce compliance more effectively. 25 Member States will sign it, that is

all except the UK and the Czech Republic. The treaty will enter into force once 12 euro

countries have ratified it.

Secondly: we endorsed the agreement between the 17 on the Treaty for the European

Stability Mechanism. We call on Finance Ministers to sign it at the next Eurogroup

Meeting (Feb 29th?), so that it can take effect from July 2012. The early entry into force of this

permanent firewall will prevent contagion in the euro area and further restore confidence.

Thirdly: as agreed in December, we will reassess the adequacy of resources under the

EFSF and ESM rescue funds in March. -- And since our next summit is on the 1st of

March, this is actually less than 5 weeks from now!

Fourth and last element: concerning Greece, we welcome the progress made in the

negotiations with the private sector. We call on the Greek authorities and the troika to

agree on the steps to put the current programme back on track. We urge Finance Ministers

to take all necessary actions to implement the private sector involvement agreement and to

adopt the new programme by the end of the week, well in time for the launching of the

'PSI' by mid-February.

Final point: Although it was not formally on the agenda today, we also briefly touched

upon foreign relations. I have issued a separate press statement on this, so let me just

mention the three topics we discussed. We endorsed the restrictive measures against Iran,

including an oil embargo, as decided by the Foreign Ministers last week. We expressed our

outrage at the atrocities and repression committed by the Syrian regime, and urged the

members of the UN Security Council to take long overdue steps to bring an end to the

repression.

The European Week Ahead:

Sunday: Jan. UK Lloyds Employment Confidence

Monday: Feb. Eurozone Sentix Investor Confidence; Dec. Germany Factory Orders; Jan. UK BRS Sales Like-For-Like and New Car Registrations; Jan. Russia Consumer Prices and Core Inflation

Tuesday: Jan. Germany Wholesale Price Index (Feb 7-12); Dec. Germany Industrial Production; Jan. UK BRC Shop Price Index; Dec. France and Russia Trade Balance

Wednesday: Dec. Germany Current Account, Trade Balance, Exports, and Imports; Jan. France Business Sentiment and Budget Balance; Iceland Interest Rate Announcement

Thursday: Eurozone Policy Meeting and Interest Rates Announcement; UK Interest Rates Announcement and Asset Purchase Target; Jan. UK GDP Estimate; Dec. UK Industrial and Manufacturing Production, Trade Balance; France Survey of Industrial Investments; Jan. Russia Budget Balance (Feb 9-13); Nov. Greece Unemployment Rate

Friday: Jan. Germany Consumer Price Index – Final; Jan. UK PPI Input and Output; Dec. France Current Account, Manufacturing and Industrial Production; Dec. Italy Industrial Production

Extended Calendar Call-Outs:

16 February: Allegedly the “new” PSI deadline

29 February: 2nd 36-Month LTRO Allotment

25-26 February: G20 Finance Ministers Meeting in Mexico City. Decision on IMF loan of €500B expected

20 March: Greece’s €14.5 Billion Bond Redemption Due

30 June: Deadline for EU Banks to meet €106 Billion capital target/the 9% Tier 1 capital ratio

1 July: ESM to come into force

Matthew Hedrick

Senior Analyst