THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

It’s February, welcome to round 2 of the inflation/deflation/reflation game of expectations:

- CHINA – immediate-term growth expectations are coming down in a hurry now that commodity inflation expectations are rising – last night’s PMI print of 50.5 was not only a miss vs uninformed whispers (sad), but was a sequential deceleration in the slope of improvement (hard to beat the DEC v-bottom vs NOV). Chinese stocks closed down -1.1% on the news, and they should have.

- GERMANY – just absolutely ripping this morning on a big breakout above my long-term TAIL line for the DAX of 6503. Germany’s stock market is now up +11.7% YTD! (vs SPX +4.3%) as the old Bundesbankers prove out that there is an economic model that resides right of left-center (Keynes).

- TREASURIES – kaboom! US Growth expectations are getting hammered into the hole now w/ 10yr yields hitting YTD lows this morn at 1.81%. A lot of people will convince themselves that US stock futures up is whatever they want it to be, but I see that simply as inflation expectations rising which, in turn, slow growth even further. The Yield Spread hitting its lowest YTD at 161bps wide – should put a lid on the Financials at $XLF 14.24.

After 4 consecutive down days in the SP500, we’re due for another low-volume bounce to another lower long-term high. Immediate-term resistance = 1323.

SUBSECTOR PERFORMANCE

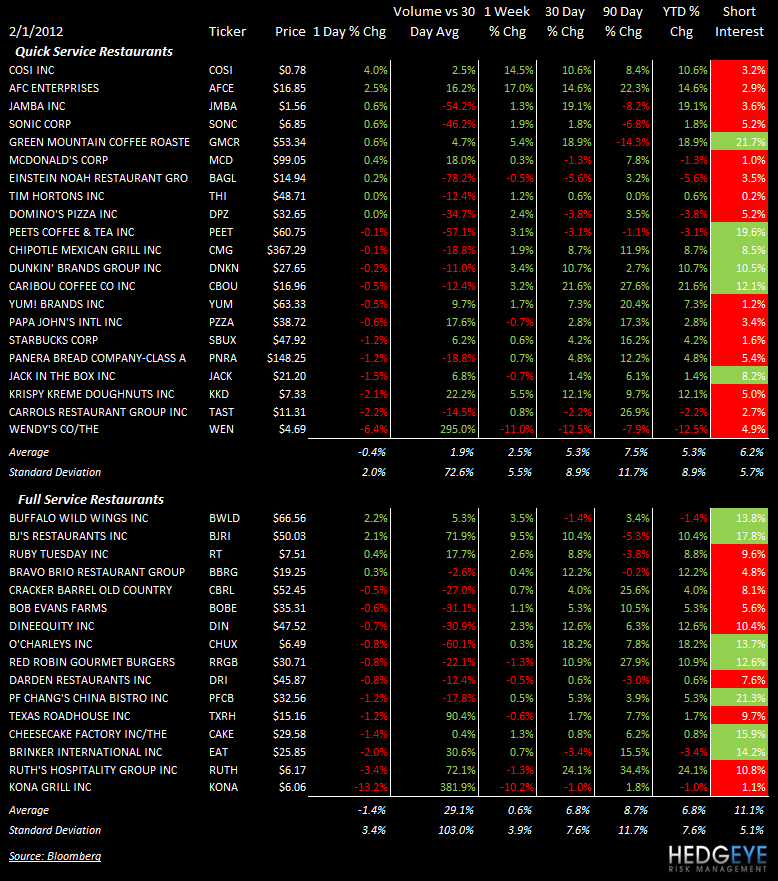

QUICK SERVICE

WEN: Wendy’s was cut to “Neutral” at Roth Capital.

JACK: Jack in the Box was initiated “Buy” at Lazard.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

WEN: Wendy’s traded down -6.4% on accelerating volume. See our note from Monday; this concept needs $3.7 billion to right itself and become competitive again.

CASUAL DINING

MRT: Tilman Fertitta announced today that this wholly-owned company, Fertitta Morton’s Restaurant’s, Inc., has successfully completed a tender offer for all of the outstanding shares of common stock of MRT at $6.90 per share.

NOTABLE PERFORMANCE ON ACCELERATING VOLUME:

BWLD: Traded up 2.2% a week ahead of earnings. We think the forward commentary will be bearish for the stock.

KONA: Traded down -13% on accelerating volume after appointing Berke Bakay as president and CEO

Howard Penney

Managing Director

Rory Green

Analyst