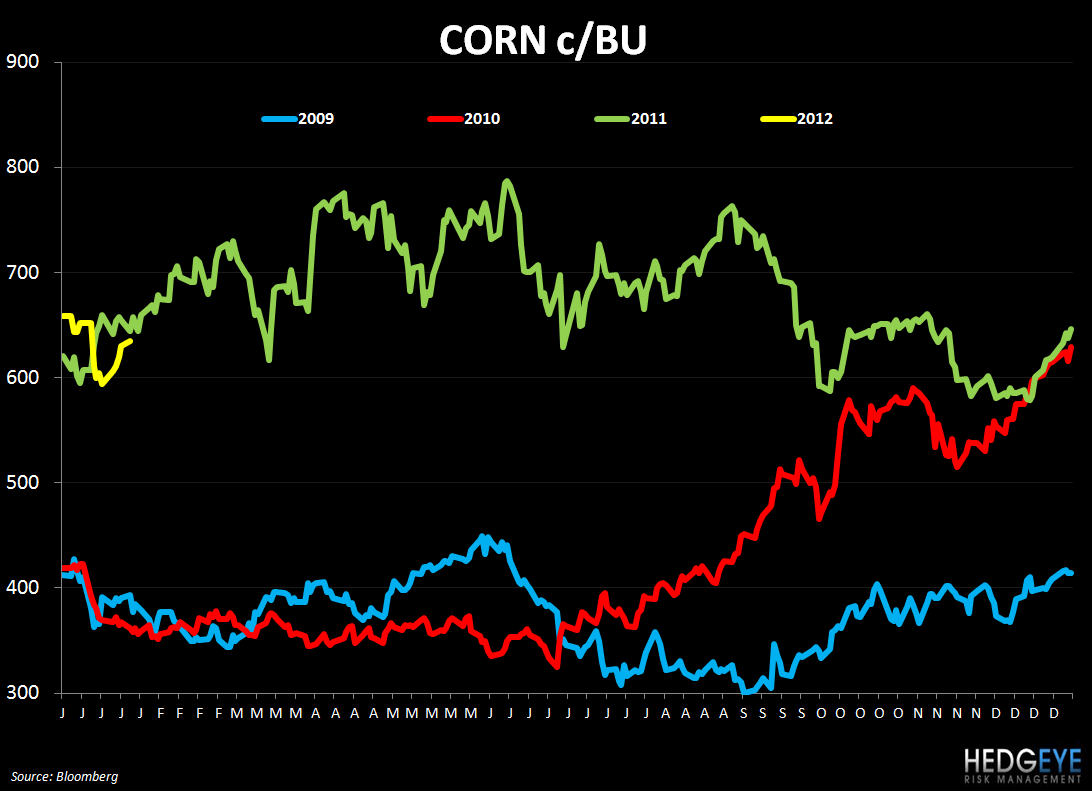

Corn and wheat gained 7% and 8%, respectively over the last week. Most commodities moved higher as the Dollar Index weakened.

Almost all of the commodities that we monitor saw week-over-week price increases. Food inflation is likely to be less of a factor, on the margin, for restaurant stocks than it was in 2012 but we still expect some companies to see continued pressure on margins. This will be especially true in the first half of the year for companies with exposure to beef and chicken (particularly wings).

In terms of CPI, consumers are still seeing steeper food inflation in their grocery bills than in the restaurant check. Proposed legislation in Washington, HB 3798, is expected to lead to higher food prices for American consumers. The legislation focused on egg production. For an albeit one-sided write up, click here.

SUPPLY/DEMAND DYNAMICS

Grains – WEN, TXRH, CMG, PNRA, DPZ

DPZ: Company expects overall basket to be up 4.5-6% in 2011. No specific guidance for 2012 but hoping for a moderation from 2011 levels.

CMG: Management plans to take no additional pricing in 2011. Currently there is roughly 4.6% of price on the menu.

SUPPLY

- Corn output in Argentina is expected to fall by 7% in the year starting March 1ston a year-over-year basis.

- Russian grain shipments will slow because of shrinking inventories, according to the USDA.

DEMAND

- Export demand for American corn is improving. Export deports near New Orleans boosted premiums this week to the highest level in two months.

- The UN’s Food and Agriculture Organization has spoken out against the use of corn for ethanol production as it “affects the prices of maize all over the world”.

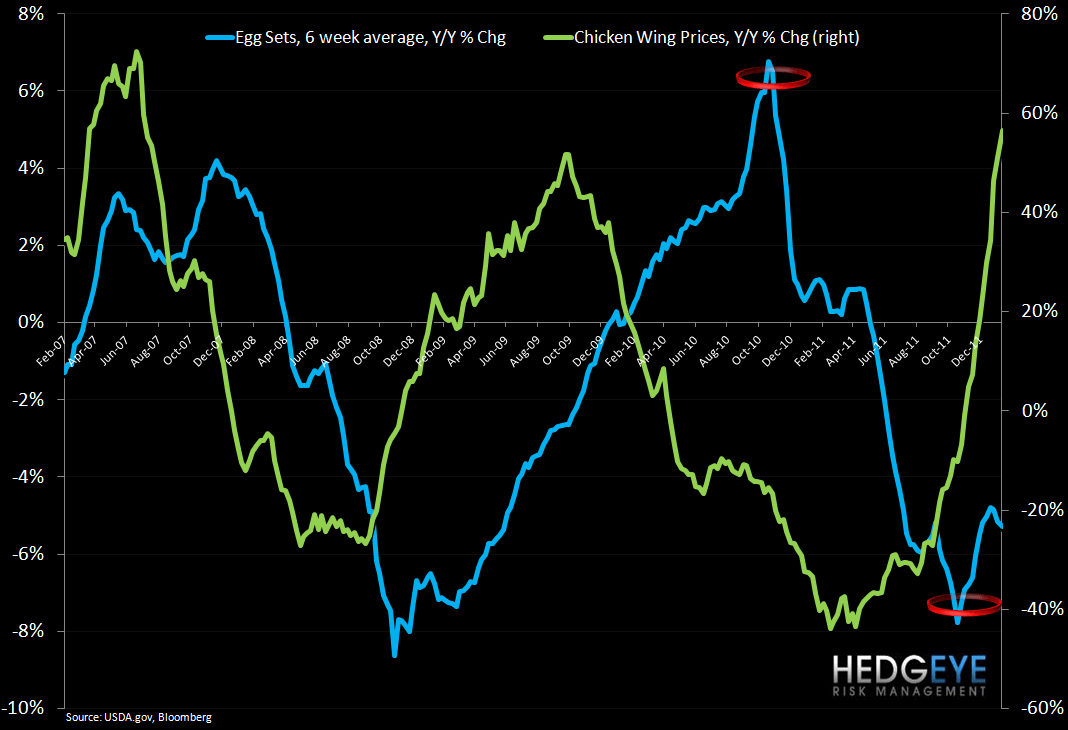

Chicken Wings – BWLD

BWLD: The company has guided to ~2% pricing for 2012. We believe that this will be revised higher. We also expect guidance for “moderate” inflation to be revised when the company reports 4Q11 earnings.

SUPPLY

- The six-week moving average for egg sets has declined for the past couple of weeks (chart below). We will be watching this as a leading indicator of supply in the U.S. chicken industry.

DEMAND

- We expected demand for chicken to be strong in 2012 as restaurants look to offset the elevated beef prices. This is bullish for wing prices.

Beef – WEN, TXRH, JACK, CMG

WEN: The company expects ROP margins to be down roughly 100 basis points year-over-year in 2011. Beef remains a concern at 20% of spend. The company purchases fresh beef and does not contract its beef needs.

SUPPLY

- The USDA is releasing its biannual cattle inventory report on Friday. The report is expected to show shrinkage in the U.S. herd, which is already the smallest since the 1950s.

- Elevated corn prices are not helping the cattle industry, with many ranchers in Texas seeing their businesses hurt in the past year by elevated feed costs and severe drought.

DEMAND

- The largest tailwind for U.S. beef demand is Japan reviewing curbs on U.S. beef imports. Japan was once U.S. beef’s biggest customer. South Korea is also expected to increase its consumption of U.S. beef.

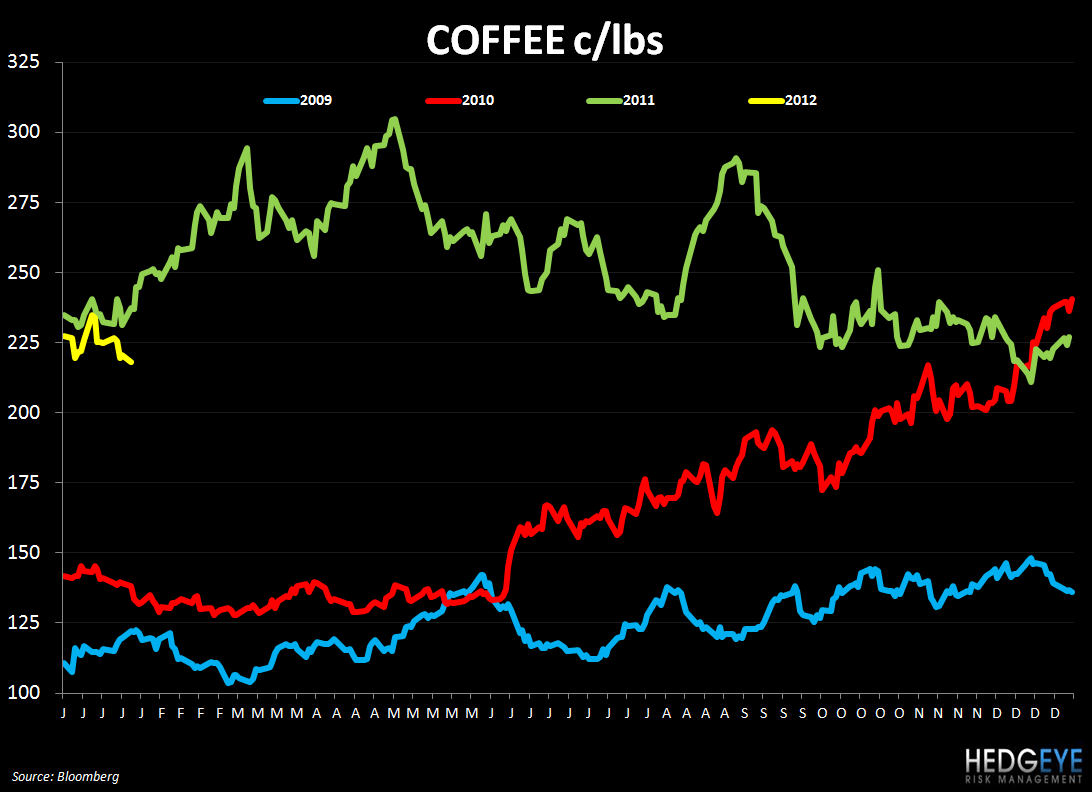

Coffee – SBUX, DNKN, GMCR, PEET, THI, CBOU

SBUX: Company reports tomorrow, it will be interesting to hear thoughts on pricing strategy going forward. We expect some commodity-related pressure to ease as we lap higher coffee costs of 2011.

SUPPLY

- Peru’s coffee crop is expected to fall by 8.8% this year from last year’s record.

- Brazil is consuming more of its own coffee, which will lead to higher prices in the U.S.

DEMAND

- Coffee consumption in Brazil, the world’s largest producer, will rise by 3.5% this year, according to a Brazilian roaster’s association known as Abic said today.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst