This note was originally published January 20, 2012 at 12:45 in Energy

We look to Schlumberger (SLB) as a bellwether for the oil services industry. From the Company’s 4Q11 results, and more importantly the management team’s commentary and outlook, we have more confidence in our bearish thesis on North American land-focused energy services companies. Further, we feel that the service companies with the most leverage to the rebound in deepwater drilling, as well as the nascent international shale drilling market, will be the outperformers in 2012.

Weatherford International (WFT) is heavily exposed to the North American land services market. According to the 4Q10 segment breakdown, 48% of WFT’s revenue and 66% of its operating income comes from its North America business, which makes a soft North American services market a major headwind. Further, WFT is not a major player in deepwater or an early mover in international shale exploration, which will be the pockets of strength in 2012. Given, we like WFT on the short side. If you are looking to pair it off, go with long SLB. We shorted WFT this morning in our Virtual Portfolio at $16.68.

Other reasons we like WFT on the short side are as follows:

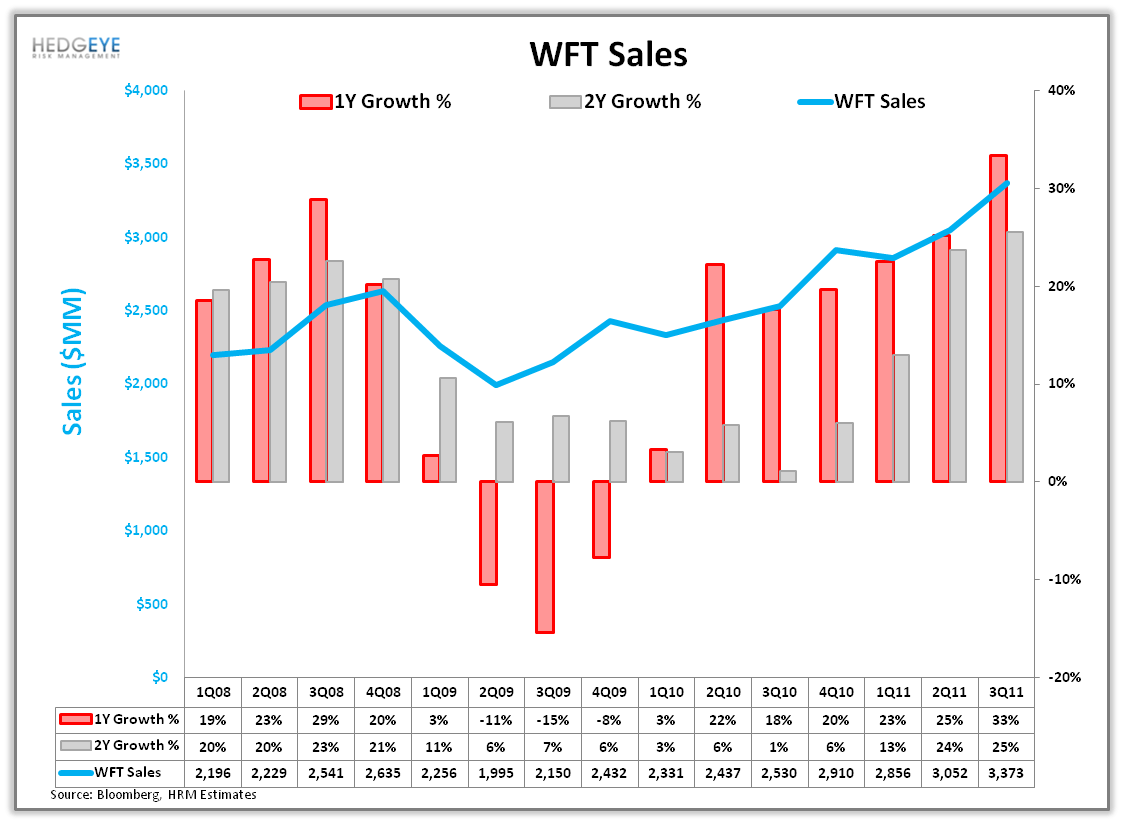

- Slower top line growth in 2012 as company compares against increasingly difficult 2011 numbers (chart 1);

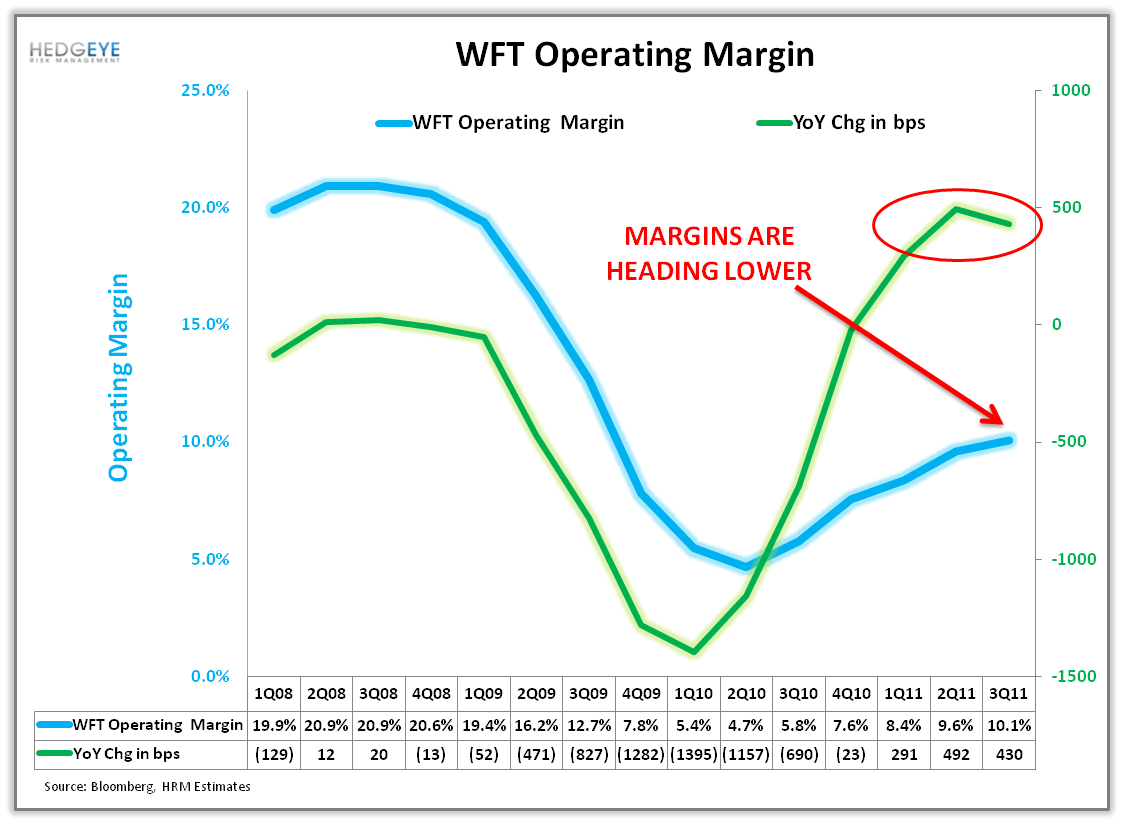

- Margins peaking and contracting (chart 2);

- North American land drilling activity slowing (chart 3);

- North American land pricing slowing (chart 4);

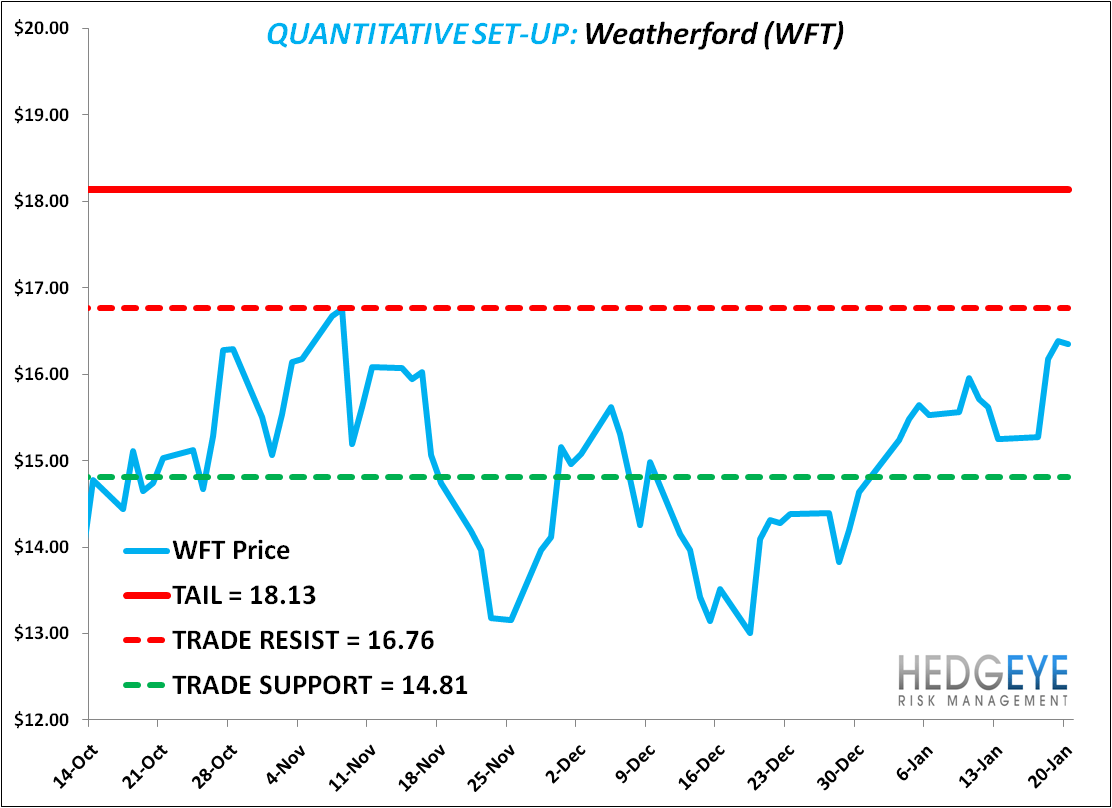

- The stock is 26% off its December 2011 low and is bumping up against our TRADE line resistance of $16.76. The long-term TAIL line is broken, $18.13 (chart 5).

SLB confirmed our fundamental view on the services industry in North America – that gives us incremental confidence in our short WFT thesis. BHI and HAL report earnings early next week – we see no reason for those companies to say much different.

Here are some callouts from the SLB call along with quotes from the management team:

Land activity in North America is flat and likely falling due to crashing natural gas prices. Pricing – pressure pumping, drilling, and completions – is slowing. As a result, sell side estimates are too high for 1Q12 in their assumption of 26% y-o-y revenue growth and too high for the full-year barring a recovery in the natural gas market:

“The current consensus is probably somewhat on the optimistic side or on the high side [for 1Q12]. Just a comment on how we see the quarter from this point. I think the underlying activity continues to be strong and it's driven by steady growth in the international markets and also strong activity in North America shale liquids. Like you say, we are going to see the normal seasonal slowdown in the North Sea and Russia. And I think also the sequential drop in product sales and multi-client sales. I think also there is some added uncertainty going into Q1 now in terms of the impact of the accelerating drop in North America shale gas activity. So generally I would say that the current consensus is somewhat on the optimistic.”

“In North America, land revenue grew in line with rig count while margins increased moderately driven in part by internal efficiencies and active cost management. Pricing in our wireline and drilling product lines continue to show an upward trend although slowing somewhat compared to previous quarters. In pressure pumping downward pricing pressure in the gas basins continued in the fourth quarter. Pricing in liquids-rich basins remained more or less flat excluding the impact of continued conversion to 24-hour operations.”

“In North America, we expect land rig count to remain flat with Q4 2011, combined provided the ongoing drop in gas activity will be countered by increasing activity in the liquids and liquids rich basins.”

“Well, if you look at pressure pumping pricing, as I said, we continue to see downward pressure on pricing in gas [basins] in Q4. The liquids basins we saw pricing basically being flat, some contracts being up in some context been down.”

The deepwater recovery – particularly in the GoM and off both coasts of Africa – is fully underway and will be a tailwind for the deepwater servicers in 2012:

“ This quarter I think was the first quarter where our Gulf of Mexico margins were accretive to North America.”

“We're quite optimistic in terms of the outlook for the Gulf of Mexico. Firstly in terms of our market share position and in terms of how well we can leverage our high-end technology and operational performance in this type of market. So we see steady growth in deepwater drilling rig counts during 2012, roughly about a rig a month so we would be at pre-Macondo levels for drilling rigs in the Deepwater by the latter part of 2012.”

We are in the early stages of E&P in international shale plays. That activity will continue to trend higher over 2012 and 2013; SLB and HAL are the early movers:

“We won a lot of contracts in the international market requiring fracturing capacity. So in the event that we have the opportunity or basically decide to shift capacity internationally, I think that will be welcomed by our international operations.”

“I think that international capacity is obviously one driver that's going to support pricing going forward because we don't see significant overcapacity in the international market.”

“We won a number of these contracts in all parts of the world and I would say that the increase in activity for us in international unconventionals over this year and going into next year is probably somewhat higher than where I thought it would be going back two or three quarters. So we expect to see strong growth in all the international shale plays for us in 2012. The work is still going to be around evaluation and pilot projects in general but I mean it's still going to represent very good growth for us and I think the two markets that are going to take of the fastest, I would say would be Argentina and China.”

Kevin Kaiser

Analyst