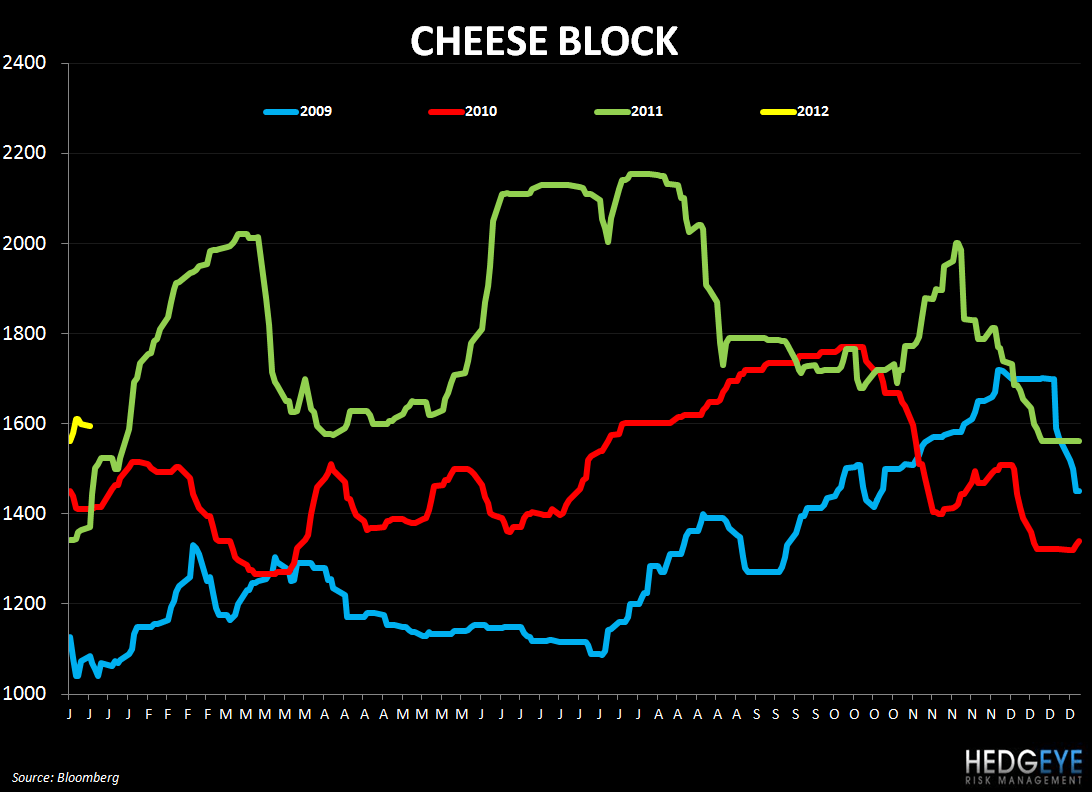

Commodity price changes were mixed over the past week as chicken wings, cheese, and coffee gained while beef and grains declined. The strengthening dollar is putting a dampener on food inflation, particularly with respect to grain prices, and this, if it continues, will help to ease price inflation – eventually – in derivative food groups like proteins and dairy. One beneficiary could be PNRA while companies with exposure to dairy and protein like CAKE, CMG, TXRH and JACK will likely have to work through other supply and demand factors that are sustaining higher commodity prices in those groups. The bad news for BWLD was wing prices increasing by over 7% week-over-week.

STOCK THOUGHTS

Wheat – PNRA, DPZ, PZZA

Supply & Demand

Tomorrow’s World Agricultural Supply and Demand Estimates update from the World Agricultural Outlook Board will shed new light on supply and demand pressures on wheat and other foodstuffs. Analysts are expecting a large increase in the size of the winter crop planted – the largest for three years – just as global supplies are growing to their highest levels in 10 years. Russia, Ukraine, Canada, and India also harvested larger crops in 2011 than in 2010 due, in some cases, to adverse weather conditions in 2010.

Demand is still expected to be strong in 2012. The USDA expects growth in demand to exceed 4% with feed use in wheat rising 16% year-over-year as corn prices push farmers to substitute more for corn in livestock feed.

PNRA

Panera follows a laddering purchasing strategy for wheat and, as a result, the cost of the grain for PNRA is expected to be flat in 2011 versus the year prior.

As of the last earnings call, on October 26th, management declined invitations to provide thoughts on the quarterly cadence of commodity inflation for 2012 instead providing 4% as an annual inflation estimate. The company locks into some of its wheat needs up to a year in advance so we do not expect any revision in near-term expectations due to the spot price declining. The top-line has been strong, however, so the company could continue to deliver in the face of commodity pressure.

DPZ

Dominos is locked into wheat “partway” into 2012.

Chicken Wings – BWLD

Supply & Demand

As the impact of processors cutting production is felt in the supply of chicken and the demand for chicken from the food service industry increases in 2012, we expect prices to increase for chicken wings.

BWLD

Our bearish thesis that we laid out for Buffalo Wild Wings’ stock in October was based on wing prices of $1.40 in 1Q12. Prices are currently at $1.70 and we think downgrades and a change in tone from management are likely as the investment community looks to 2012.

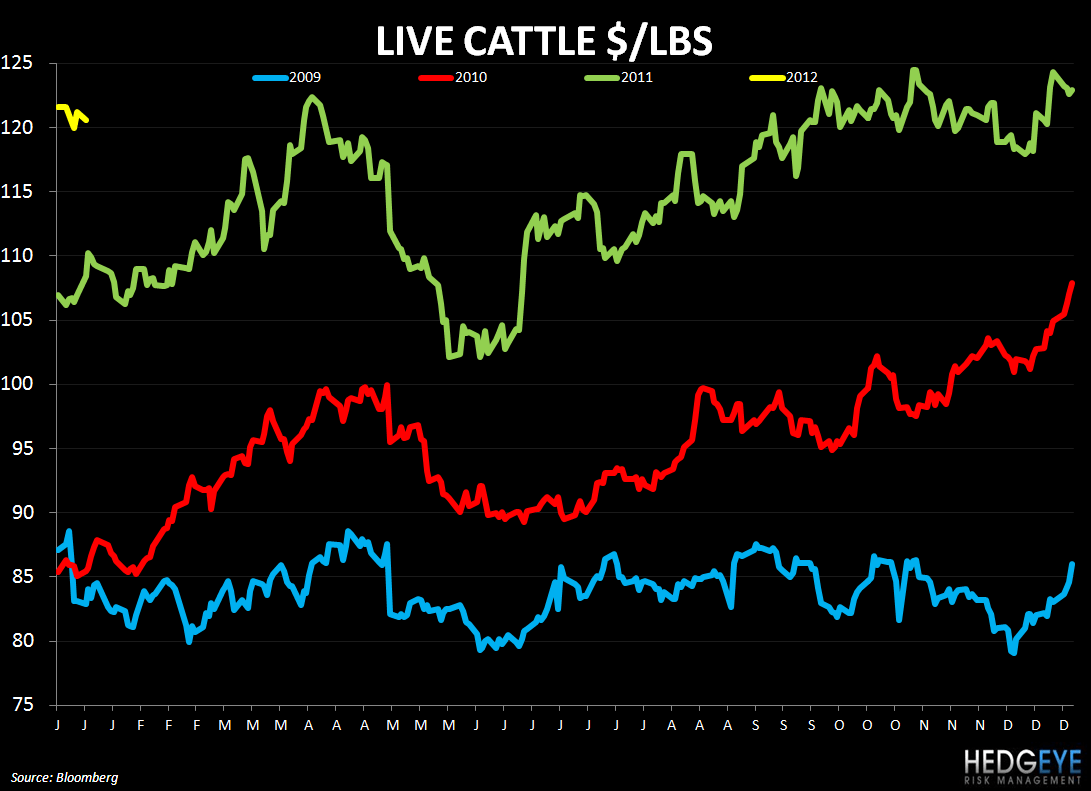

Beef – WEN, TXRH, JACK, CMG

Supply & Demand

Beef prices declined on the week as rains in Texas boosted winter wheat and cattle pastures. 2011 was the driest year on record in Texas and the domestic herd size is depleted due to high feed costs coinciding with the drought in the Lone Star State and high feed costs. Feed costs remain high but, if corn prices come down then margins for processors could improve over the intermediate to long term.

Demand for beef continues to grow as changing diets in emerging markets and fading BSE-related restrictions on U.S. beef are bullish tailwinds over the long term.

WEN, TXRH, JACK, CMG

As this week's beef chart shows, companies with exposure to beef prices are facing significant year-over-year cost inflation for at least the first quarter.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken – Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst