THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP – January 6, 2012

Sold my Growth Slowing position in Fixed Income yesterday (US Treasury Flattener – FLAT = +28% gain). I’d held that position for a year and felt all warm and fuzzy about the buy-and-hold on conviction thing. Onto the next - KM

As we look at today’s set up for the S&P 500, the range is 19 points or -1.10% downside to 1267 and 0.39% upside to 1286.

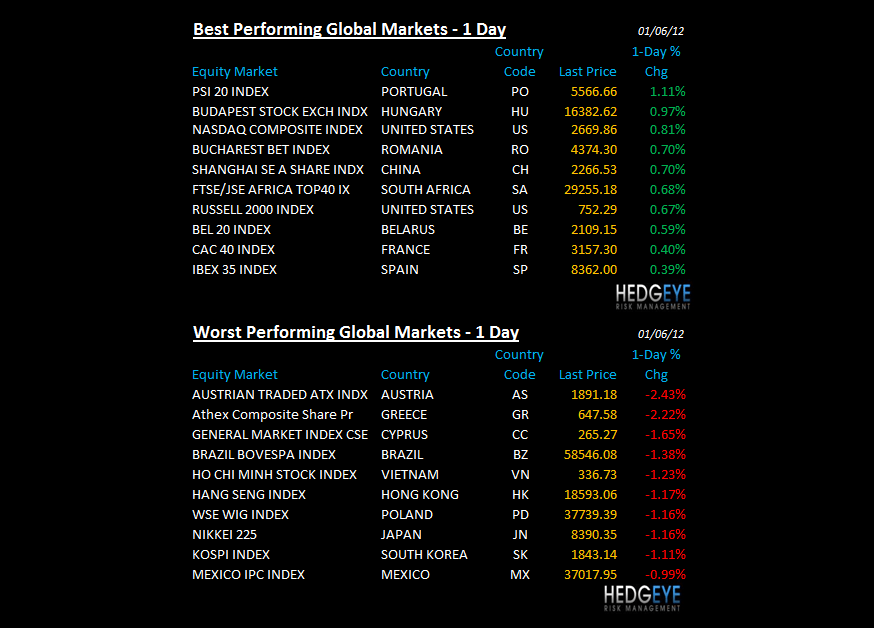

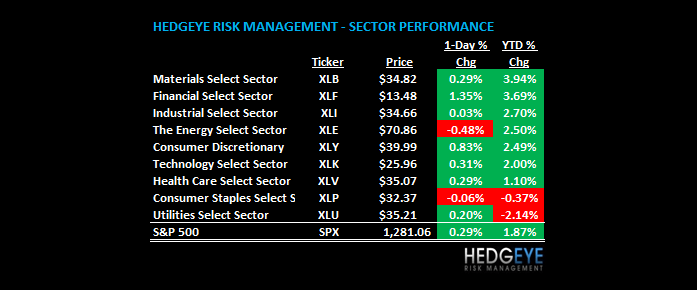

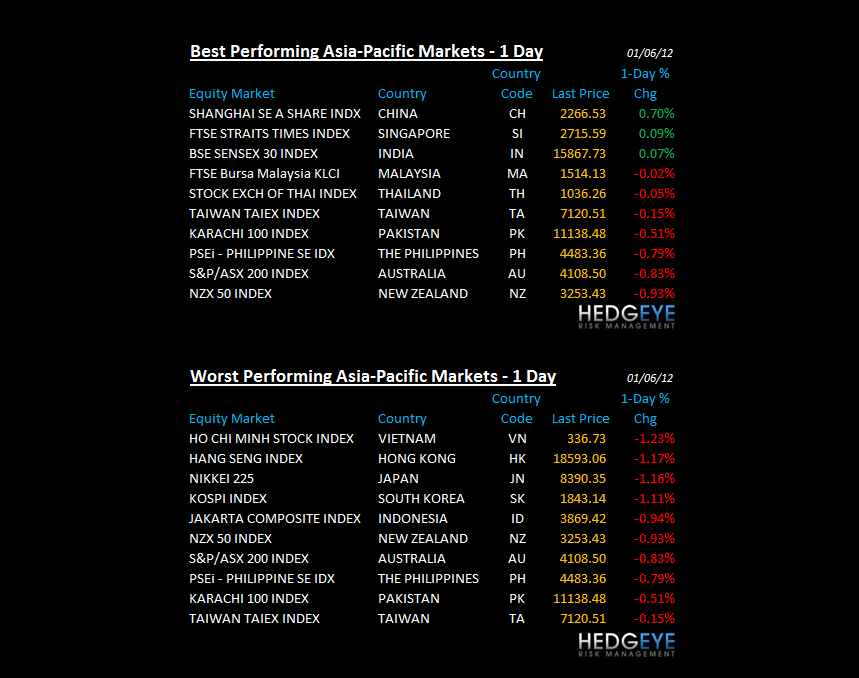

SECTOR AND GLOBAL PERFORMANCE

For the 3rdconsecutive day, the SP500 holds my long-term TAIL line of 1267 support. Not only did it test that level on the lows of the morning, but its bounce was finally confirmed by some volume. I don’t mean real volume. I just mean +19% more volume that my immediate-term average.

Volatility continues to breakdown as the US Dollar continues to breakout. Strong/Stable Currency = Stronger Employment, Confidence, and Consumption. I’ll stay on this until it stops.

All 9 Sectors remain bullish from an immediate-term TRADE perspective and I remain long of 2 of them (Consumer Discretionary, which has been a Top 2 Sector in both of the last 2 days, and Utilities, which I bought back on down move – Citi downgraded Utilities today and XLU closed up).

If tomorrow’s employment report is a bomb, a lot might change in a hurry. If it’s not, we’ll likely move to Day 4 of a bullish confirmation. - KM

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -75 (-1734)

- VOLUME: NYSE 759.44 (-11%)

- VIX: 21.48 -3.33% YTD PERFORMANCE: -8.21%

- SPX PUT/CALL RATIO: 1.69 from 1.99 (-15%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – let the masses focus on whatever it is they flip to day to day; today, I’ll be focused on 1 line in the sand and that’s the intermediate-term TREND line of 2.03% resistance on the 10yr UST; a sustained close > than 2.03%, combined w/ repeated closes > 1267 for the SP500 will have me doing more of what I have been doing for a month (buying stocks, selling bonds).

- TED SPREAD: 57.23

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.02 from 2.00

- YIELD CURVE: 1.75 from 1.75

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- Eurozone Nov Retail Sales (2.5%) y/y vs consensus (0.8%) and prior revised to (0.7%) from (0.4%)

- Payrolls may have climbed by 155k workers in Dec. after rising 120k the previous month, economists est.

- Fed officials are nearing agreement on adopting inflation goal as Bernanke extends his push for improving transparency

- Eurozone Dec consumer confidence (21.9) vs consensus (21.2) prior (20.4)

- Eurozone Nov unemployment rate +10.3% vs consensus +10.3% and prior +10.3%

WHAT TO WATCH:

- 8:30am: Nonfarm Payrolls, Dec., est. 155k (prior 120k)

- 8:30am: Unemployment Rate, Dec., 8.7% from 8.6%

- 9am: Fed’s Dudley speaks in N.J.

- 10:20am: Fed’s Rosengren speaks on economy on Connecticut

- 12:40pm: Fed’s Duke speaks on economy in Richmond

- 1pm: Baker Hughes rig count

- 1pm: Fed’s Raskin speaks on community banking in Baltimore

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- China Forestry Auditor KPMG Resigns Citing Valuation Concern

- Gold Traders More Bullish After Bear Market Averted: Commodities

- Thieves Defy Death to Tap Metal Price Boom as U.K. Cracks Down

- Resilient Pubs May Appeal to Investors More Optimistic on U.K.

- Nestle Gains With Heinz as China Fears Local Food Safety: Retail

- Alcoa to Cut Smelting Capacity by 12% After Aluminum Decline

- Oil Little Changed as Europe’s Economy Limits This Week’s Gain

- Stocks Reverse Declines as Banks Rally; Treasuries, Euro Retreat

- Palm Oil Output in Malaysia Seen at Nine-Month Low on Floods

- Gold Set for Best Week Since December as Haven Demand Increases

- BHP’s Ekati Mine May Fetch Less Than $500 Million, Investec Says

- ENRC to Buy First Quantum’s Congo Assets for $1.25 Billion

- Oil Heading for Weekly Gain on U.S. Economy, Iranian Tensions

- Gold to Outperform Dow Index on ‘Fear Trade,’ SICA Wealth Says

- Rich to Invest More in Commodities, Reduce Cash, Survey Says

- Copper Trims Weekly Loss as U.S. Data May Lift Demand Prospects

- Platinum-Gold Ratio Drops to 0.8677, Lowest Since at Least 1987

- Soybeans, Corn Advance as USDA Seen Paring Stockpiles Estimates

- Raw Sugar Declines Most Since Mid-September; Coffee, Cocoa Drop

CURRENCIES

EUROPEAN MARKETS

GERMANY – both bunds and stocks starting to act like the fiscal champ Germany has become; no matter what the fanfare and/or finger pointing is here in the US re the Europeans, Germany’s employment and fiscal position is better than USA’s and now the DAX is holding TRADE and TREND lines of support. Haven’t bought it yet, but I will.

ASIAN MARKETS

JAPAN – down -1.2% last night puts Japanese Equities into the cellar of the major/liquid markets for the 1st week of the year. Away from being grounded by Keynesian policy, Japan has more issues than Time Magazine – so watch this market (because consensus isn’t). Japan needs to rollover 31.2% of its sov debt in 2012 – that’s 3 TRILLION Yens (a lot of yens = $566B USD)

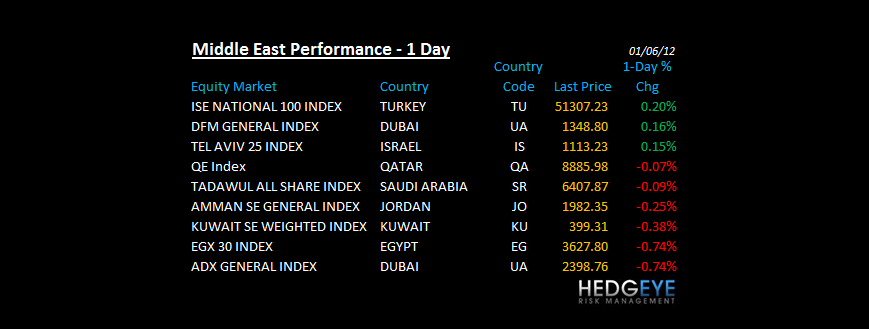

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Sheikh Holding IPad Gazes at Breitling Before Winning Melbourne

- Obama Returns to Bush Plan for Cutting U.S. Troops in Europe

- Dana Gas Sukuk Sink on Debt Payment Concerns: Islamic Finance

- Fewer, Better Nuclear Weapons Can Make the U.S. Stronger: View

- Mubarak, El-Adli Should Be Executed, Egypt Prosecution Says

- Japan to Express Concerns to U.S. Over Possible Iranian Oil Ban

- Oil May Fall Amid Iranian Threat and Rising Dollar, Survey Shows

- Oil Heading for Weekly Gain on U.S. Economy, Iranian Tensions

- MTN Drops on Nigeria’s Doubling Fuel Costs, Iran Concern

- Saudi Arabia Moved 6 Million Barrels of Oil a Day Through Hormuz

- U.K. Opposes Pre-Emptive Strike on Iran, Will Act If Hormuz Shut

- Gold Has Longest Rally in 10 Weeks on Iran ‘Fear,’ U.K. Warning

- European Refiners Seek to Replace Iran Crude as EU Nears Ban

- Formosa Buys Extra Crude, Naphtha in Case of Iran Supply Cut

- Iran’s Revolutionary Guards Plan Naval Exercises, General Says

- Dubai, Fujairah Ports Busy as Usual Amid Hormuz Passage Threat

- As Currency Crisis And Feud With West Deepen, Iranians Brace for War

- Italy’s Monti Questions Scope, Timing of EU Ban on Iranian Oil

The Hedgeye Macro Team

Howard Penney

Managing Director