December sales didn’t quite materialize as many had hoped. While the ratio of beats-to-misses was net positive at 2:1 (16 companies beat to 8 misses) the resounding takeaway this morning is the cost at which these sales came. With the majority of retailers looking to clear inventories in the midst of an unseasonably warm holiday selling season (least snowfall in over 50 years) coupled with consumers coming in later to purchase, promotional activity accelerated into month end crippling margins across the industry.

The result is ‘guide-down’ activity outpacing ‘guide-ups’ by a count of 8-to-6 this morning. More important is the magnitude of Q4 revisions i.e. JCP (-38% consensus/prior guidance), PLCE (-26%), AEO (-19%), and KSS (-14%). Consistent with last month’s sales performance and our Key Q4 Themes, margins continue to come in weaker than expected particularly at the mid-tier where there is clearly blood in the water. Just a week after SHLD lowered its guidance, both JCP and KSS lowered their own while GPS missed comp expectations yet again.

Volatility continues to increase in retail and is expanding the bifurcation between upward and downward revisions as is clearly evident through the first two months of the quarter. We expect Q4 results to reflect this reality and for volatility and this bifurcation to remain clear and present through the 1H at a minimum in an increasingly more competitive pricing environment.

A few additional callouts in December:

- The High/Low-end performance spread remains divergent. Within department stores, JWN +8.7%, M +6.2%, SKS +5.8% were solid while JCP +0.3%, KSS -0.1% came in slightly above and below expectations respectively, but both materially lowered Q4 guidance. BONT -0.7% continues to be the department store laggard.

- Food/Grocery continues to outperform driving results at discounters. Both COST and TGT reported the food/grocery up LDD outpacing all other categories. While COST came in better than expected, TGT came in light as home and hardlines weighed on sales. Notably, TGT was one of only a handful of retailers highlighting its inventory position noting they were in ‘very good condition’ at month end.

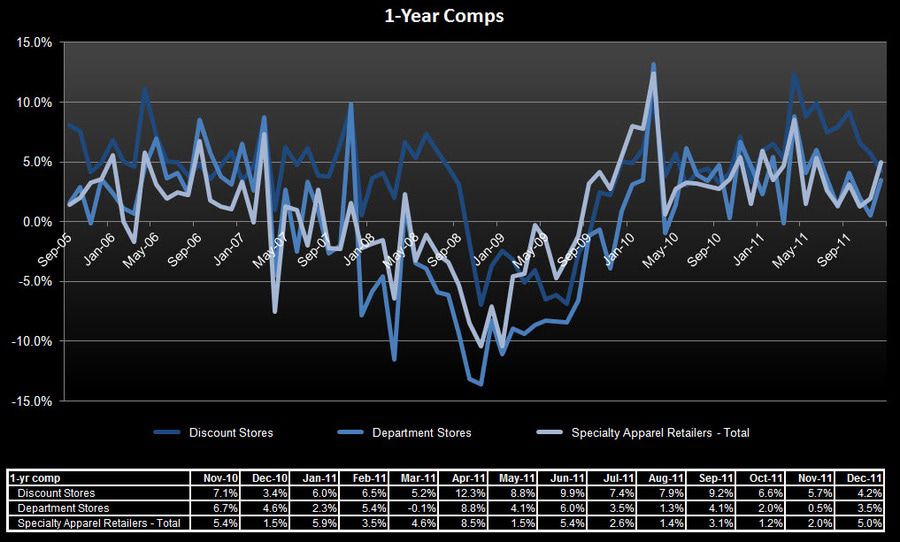

- TGT’s results mark its second consecutive sequential comp decline since Aug11 and its lowest 2yr comp of +1.3% since Jan11. This was perhaps the only negative earnings revision due to weaker sales instead of margins imploding in December. The key here was TGT’s favorable inventory position headed into the holiday that allowed it to be less promotional. Weakness on the margin at TGT a net positive for WMT.

- GPS posted the biggest miss of the month coming in -4.0% vs. -1.9%E. Perversely, this could be viewed as incrementally positive reflecting lower promotional activity = stronger margins; however, we would strongly caution against such optimism given the visible stress in GPS’ competitive set.

- JCP & KSS reported the most significant negative Q4 earnings revisions of the monthly contributors. Of the companies to report seasonal results, PLCE and AEO took the honors. Consistent with the rest of retail, both highlighted sales coming in as or better than expectations with ‘margins down due to increased promotional activity.’ That was clearly the tag-line du jour this month.

- The clear positive standout of December was M. Not only did comps come in better than expected (+6.2% vs. +4.7%E), they also raised guidance (i.e. not at the expense of margins). Online continues to drive sales coming in up +36%. More importantly is the company’s more aggressive stance towards capital allocation. Macy’s announced it would double its dividend as well as significantly increase its share repurchase authorization by $1Bn from the $850mm, which was just reinstated in Aug11. Good for PVH, RL and others over-indexed to M.

- At the category level, hardlines were negative while softlines/apparel was positive at both COST and TGT. Despite SHLD noting weakness in appliances sales were up at COST and home was up at both KSS and TGT.

Longs: LIZ, WMT, NKE, RL

Shorts: HBI, CRI, JCP, BBBY, SHLD

Casey Flavin

Director