Our SIGMA framework is predicated upon the relationship between a company’s sales/inventory levels relative to margins, a major theme headed into the fourth quarter.

Recent incremental shifts in the SIGMA suggest some retailers are better positioned for a more competitive year-end while others are not. The key callouts include WMT, FL, TRLG, SKX & HD looking incrementally more favorable while BKE, M, SKS & LULU look more precarious.

Here are the more noteworthy Q3 shifts (both positive and negative on the margin):

THE GOOD:

WMT: After running negative for 5 quarters, the sales/inv spread turned positive in Q3 with WMT US & Sam’s clubs comps exceeding guidance and inventory growth slowing on the margin (down 4 pts to +7.5%). This comes at a time when WMT is outperforming its peers this holiday and comps are beginning to turn.

“We're very well positioned with inventory in both store and online for the fourth quarter…. We have the assortment our customers are looking for, both in-store and online. We have the inventory they need and we have the prices that can't be beaten.” –Bill Simon, President & CEO WMT US Stores

HD: The Sales/inv spread expanded 3 points in Q3 after making its biggest sequential move in 2Q11 since the start of ‘09. The spread now sits at +7%, the highest point since the first quarter of 2008 while margins have been expanding for 9 quarters in a row. Can it really get much better? This is one of the names where the SIGMA is so bullish that it is almost bearish.

“We're thrilled with our inventory performance, and we've just spent a lot of money transforming our supply chain, so we're hoping to see this come through. As you know, we have committed to get a full turn of improvement over the next several years. If you look at where we are seeing it, part of it is really just in terms of the quality of the inventory. Our clearance levels are as low as they have ever been in our company history.” –Carol B Tome’ CFO

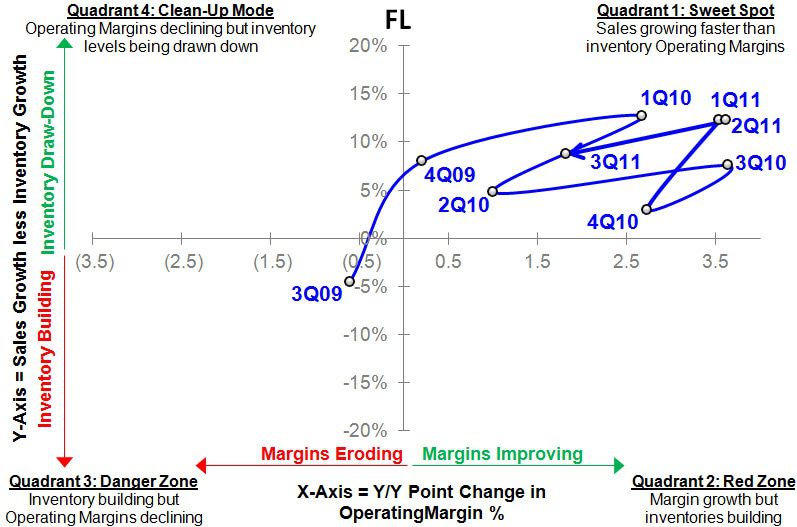

FL: The spread slowed 3 pts to +9% in 3Q11 but has remained positive for 8 quarter in a row with margins expanding in each of those periods. Revenue growth continues to run 2X inventory growth which has driven a reduction in markdowns and as a result has kept margins on the upswing in both apparel and footwear.

“Our clean, fresh inventories have allowed us to keep reducing our markdown rates in almost every division….. Margins remain on the upswing in both categories as well as in accessories and we see ongoing opportunities for further improvement.” – Lauren B. Peters CFO

SKX: The SKX Sales/Inv spread improved 13 points in Q3 as they lapped 70% growth in Q3 inventories LY. As a result, inventories were down 27% on a 26% decline in sales. The SIGMA’s clockwork move suggests trends are improving on the margin, but be mindful of the incremental inventory coming on to support the company’s ramp into fitness in the 1H F12 that will likely curb near-term sales/inventory progress.

“We cleared out excess inventory in the third quarter and are pleased that our margins which were 42.5% for the third quarter of 2011 have returned to their historical norm, a reflection of selling more inline product.” – David Weinberg, COO/CFO

TRLG: Inventories improved sequentially for the third quarter in a row down 14 points to +5% YoY. While the top-line mirrored the inventory trends and decelerated on both the 1 and 2 yr, the spread jumped 11 points to +12% with EBIT margin improving incrementally as well.

“Well, some of the things we've been doing from an inventory perspective is really just pulling together the team to analyze our production plans in relation to our sales plans….. We're comparing our balance this year to last year, we just got a better approach to managing the production, linking it up with current sales forecasts and trends to avoid building any type of excess position especially in the warehouse.” – Peter F. Collins, CFO

GCO: Sales growth continues to outpace inventory growth despite inventories up over 20% YoY for the 5th quarter in a row. The spread improved 8 points to +12% marking the strongest relative growth position since the beginning of 2008 reflecting both better assorted inventories as well as stronger performance across all channels of late.

“So, right now, we're in a position where we are less broad, more deep. That should help sell-throughs, both in terms of having a greater percentage of hot products in the stores, but also when you get down to the final run, you have much more efficient use of your inventory. So, we are in that very good position.” – Robert J. Dennis CEO

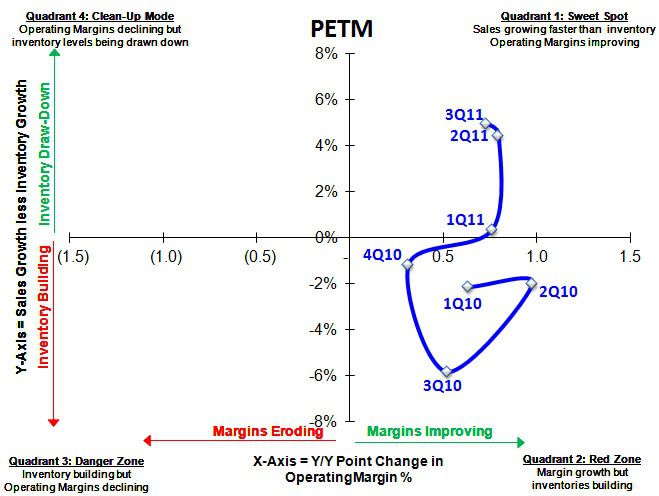

PETM: The sales/inventory spread has been improving on the margin for 4 quarters while operating margin expansion has consistently improved to the tune of 30-80bps. Average inventory/store continues to be well controlled coming in flat YoY which is meaningful given guidance for a more promotional fourth quarter.

“The second drainer (referring to negative impact on margins) was we were a little bit more promotional in some of our traffic-driving items this quarter. We made some decisions early in the quarter to go that direction. And that'll continue through probably the end of December.” – Lawrence P. Malloy, CFO

THE BAD:

BKE: Buckle’s inventory position was up 27% on 12% growth in sales. The company increased its denim inventory to avoid missing out on sales a la Christmas 2010. The opportunistic approach drove the sales inventory spread down 10 points to -14%, the company’s lowest position since 2003. This is the most aggressive bet on Holiday 2011 we’ve seen in retail hands down. Given the company’s posture into year-end, the outcome will be binary.

“Well, last year, we felt like we missed some business by being too low on our denim inventory, as well as certain top categories. And also, in the Men's outerwear, we did not have everything shipped to us last year. So we improved our inventory position there. So we felt that our inventory – we wanted to capitalize on some of the opportunities for holiday on several of those categories.” – Dennis H. Nelson CEO

GIL: Inventories were up 73% in Q4, up 13% sequentially on +30% sales growth – not good. With screen-printing demand off sharply, both the sales/inventory spread and margins are likely to remain under pressure through the 1H of F12.

“Weak demand and increasing competitive pricing pressure in the screenprint markets have continued into the first quarter of fiscal 2012….. The significant destocking of distributor inventories in the first quarter has resulted in excess inventories building up at the manufacturer level and to further discounting in order to try to maintain capacity utilization at capital-intensive producing mills.” – Laurence G. Sellyn CFO

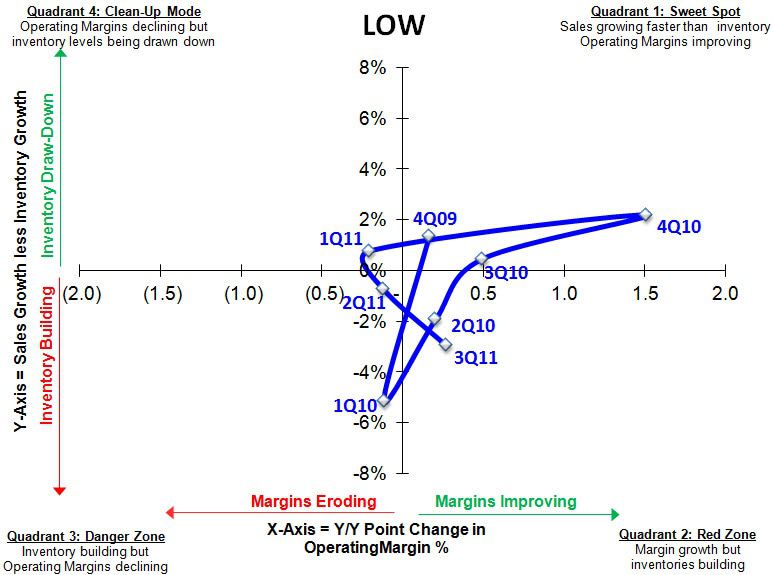

LOW: The sales inventory spread eroded 2 points to -3% in Q3. While the deterioration in itself is minor, the swing from the danger zone into the red zone to preserve margins while allowing inventory growth to exceed the top line is dangerous. Unlike Home Depot’s more aggressive approach to pricing, LOW has kept promotional activity subdued at the expense of sales while guiding to an improved inventory position at year end.

“Within appliances we chose not to match some competitors' extremely aggressive third quarter percent off promotions.” – Rick D. Damron, EVP Store Operations

LULU: LULU’s sales inventory spread fell over 50 points in Q3 due to inventory growth accelerating from +34% in Q2 to +77% in Q3; the spread now stands down (46%). The last time LULU saw inventory growth exceed sales growth, its behavioral response was far better than it should have been for such an immature company. We should see the same this time around. For additional insight on the massive swing in the SIGMA, see our 12/1 research note “ LULU: Respect History.”

“So that's the cycle we're committed to really ending and I'd rather be sitting here telling you we're in a great inventory position that's up than be sitting here quarter-after-quarter talking about being down, because then the cost is big to our guests and it's big to our brand long term. So we really are excited about where we are for inventory because it's with relief we can turn our energies to other things and we know what we have in the mix for Q4 and into Q1 is what the guests wants.” – Christine McCormick Day, CEO

M: After 8 quarters in the sweet spot, Macy’s sales/inventory spread fell 6 points into what we refer to as the “denial quadrant.” Shifts into the red zone suggest a company is propping up margins while allowing inventories to build- this is not sustainable. History proves that higher inventories are manageable if profitability is up… until they aren’t. For more detail on Macy’s Q3 SIGMA move, see out 11/9 post “M: Bad Risk Reward.”

“Planned promotions tend to be profitable. It's only when inventory is out of line with sales, which in our case is not the case, where you get excessive markdowns and margin hits. But in terms of promotions, I think it's going be pretty much as it's been the last couple of years, which is very heavy.” – Karen M. Hoguet

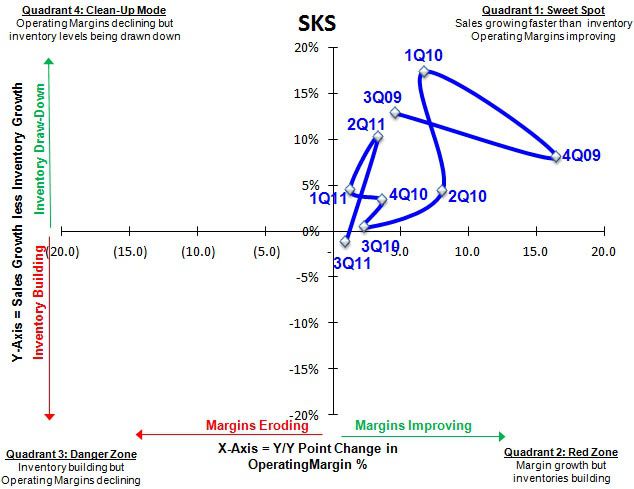

SKS: The sales inventory spread was down 1% in Q3 following 8 quarters in the “sweet spot”. Year-end inventory growth has been guided to slow below expected top line growth in Q4; however, current levels have driven incremental discounting into the holidays.

“Consequently, we believe that higher than planned inventory levels in these areas may require incremental year-over-year markdowns as we move through the traditional end of season clearance period.” – Ronald L. Frasch, CMO

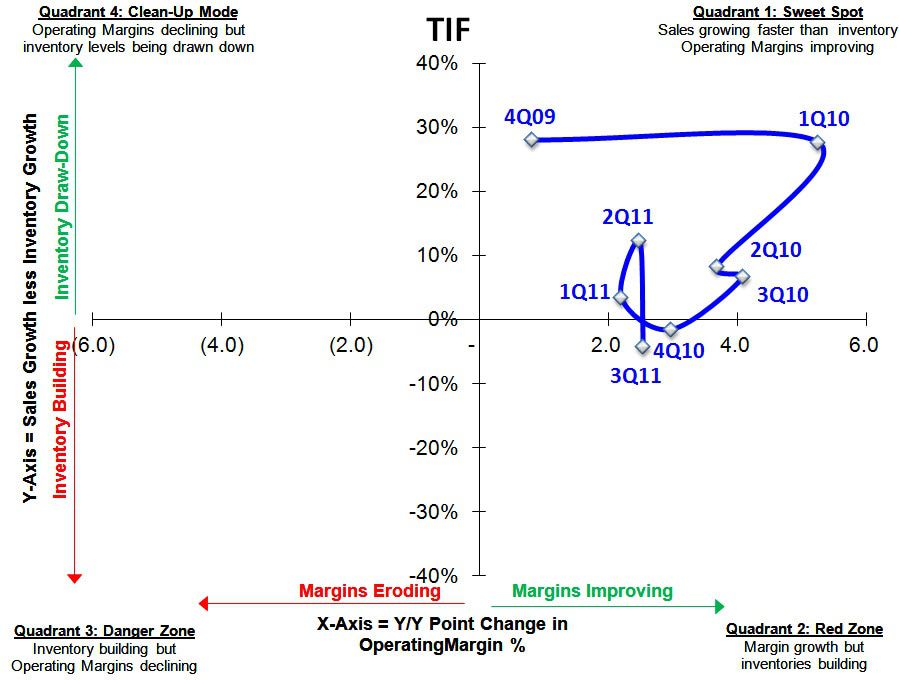

TIF: Inventories were up 25% in Q3 despite favorable compares due to a 58% increase in raw material inventories. While the increase in raw materials has been to facilitate the expansion in jewelry assortment and drive sales, the sales/inventory spread fell 16 points to -4%.

“The Tiffany & Co. brand remains strong, customers are increasingly attracted to our well-designed high-quality products, our stores have strong inventory positions, we have a well-developed and efficient infrastructure, and we have a solid balance sheet to pursue our expansion plans.” –Patrick McGuiness, CFO

All in, there has been a considerable shift of positive sales/inventory spreads turning negative in Q3. While this has been due in some part to lighter than expected sales growth, inventory growth is the real callout here and one of several reasons for our continued concern over industry margins headed into the 1H of F12. The companies we’ve highlighted above include those we see as more favorably positioned as well as those in a more precarious position given the current environment.

We have a library of SIGMAs for each of the retailers listed below. We’d be happy to pass these along at clients' request.

<chart16>