THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP – December 27, 2011

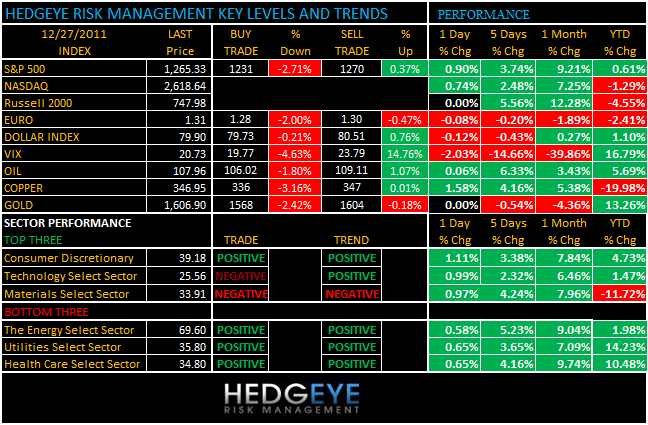

As we look at today’s set up for the S&P 500, the range is 39 points or -2.71% downside to 1231 and 0.37% upside to 1270.

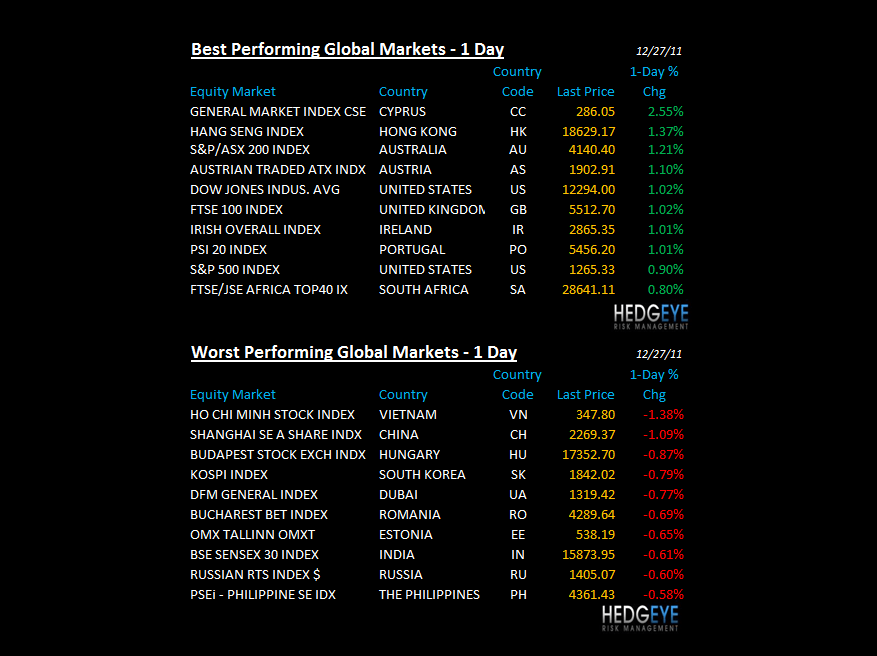

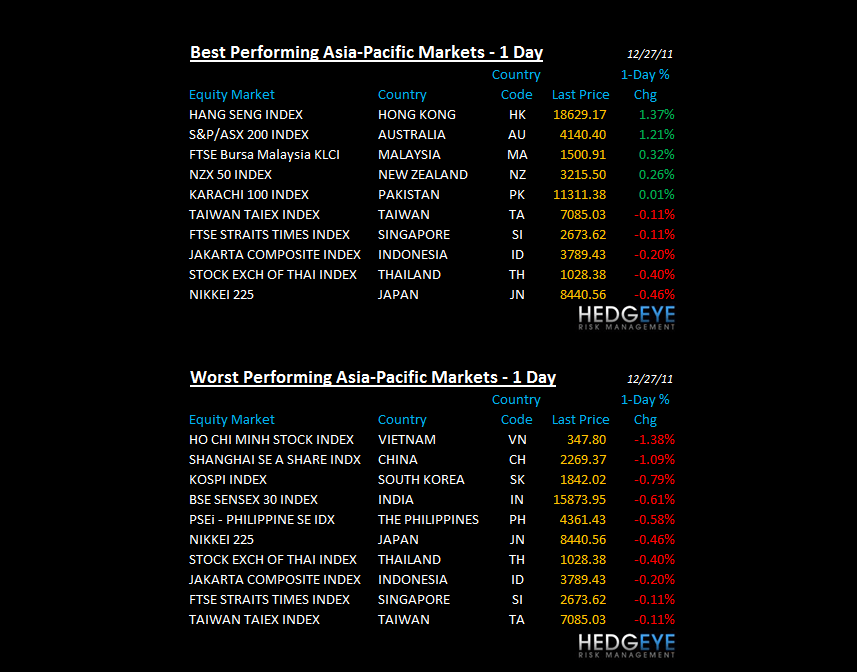

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 1151 (-389)

- VOLUME: NYSE 477.81 (-38.31%)

- VIX: 20.73 -2.03% YTD PERFORMANCE: +16.79%

- SPX PUT/CALL RATIO: 1.84 from 3.06 (39.95%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 58.03

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.03 from 1.97

- YIELD CURVE: 1.75 from 1.69

GLOBAL MACRO DATA POINTS (Bloomberg Estimates):

- U.S. holiday sales will rise 3.8% vs 5.2% advance last year: National Retail Federation

- U.S. SEC sided with the bankrupt Lehman brokerage in $3b dispute with Barclays over assets

- German govt is revising forecast for 1% economic growth in 2012 and will present a lower figure in mid-January, Focus magazine reports

- Republican presidential candidates step up campaigns as Iowa caucuses near (Jan. 3)

- Online gambling could be poised to flourish – WSJ

- Strong Christmas weekend performance insufficient to rescue 2011 box-office performance for movies – WSJ

- Apple iTV sets to be launched in Q2 or Q3 - DigiTimes

WHAT TO WATCH:

- 9:00am: S&P/Case-Shiller Y/y, Oct., est. -3.22% (prior - 3.59%)

- 10:00am: Consumer Confidence, Dec., est. 58. (prior 56)

- 10:00am: Richmond Fed Index, Dec., est. 5 (prior 0)

- 10:30am, Dallas Fed Manf., Dec., est. 4.5 (prior 3.2)

- 11am: Export inspections, Dec. 22: corn, soybeans, wheat

- 11:30am, U.S. to sell $29b 3-mo. bills, $27b 6-mo. bills

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge-Fund Managers Miss Biggest Rally in 10 Weeks: Commodities

- Mildewed Feed Caused Tainted Mengniu Milk, Regulator Says

- Oil Trades Near Highest in Two Weeks on U.S. Recovery Forecasts

- Gold Declines to One-Week Low as Europe Woes Damp Growth Outlook

- Mechel Faces Record Yields After Net Debt Surges: Russia Credit

- Copper Drops First Day in Five in New York on China Slowdown

- India’s Gold Imports Seen Dropping 50% in December on Rupee

- Corn May Extend Rally From Two-Month Low: Technical Analysis

- India May Curb Potash, Phosphate Fertilizer Prices, Jena Says

- Most Stocks Gain as Dollar Holds Losses on U.S. Economic Outlook

- Russian Gold Output Rises 4.5% to 193.8 Tons in January-November

- China 2012 Rare-Earth Export Quota Almost Same as This Year

- Aluminum Shipments by Japan Drop as Overseas Demand Weakens

- Rubber Falls to One-Week Low on Concern Chinese Demand May Drop

- Palm Oil Drops From One-Month High as Investors Lock in Gains

- Noble Group - Unlocking value in Gloucester Coal (Buy, S$1.195 - TP S$

- Paulson’s Gold Fund Said to Fall 10.5% in 2011 as Metal Rises

- China Gold Trading Limited to Shanghai Exchanges, PBOC Says

- Gold Climbs in London as Dollar Decline Boosts Investor Demand

CURRENCIES

EUROPEAN MARKETS

<CHART9>

ASIAN MARKETS

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Iran Regime Profiting From Currency Decline, U.S. Treasury Says

- Oil Traders Flee as Crude Price Swings From $100: Energy Markets

- Iraq War Lives on as Second-Costliest U.S. Conflict Fuels Debt

- Dubai’s Sukuk Trails 2010 Gains on Debt, Europe: Islamic Finance

- Qatar Plan to List Debt May Boost Local Bond Sales: Arab Credit

- Saudi Arabia Forecasts $3.2 Billion Surplus in 2012 Budget

- Saudis Need $74 Oil Price to Balance 2012 Budget, Jadwa Says

- Abu Dhabi’s Aldar Board to Discuss Selling Assets, Projects

- Renaissance Plans to Raise $130 Million Via Private Placement

- Aldar’s May 2014 Bond Yield Drops to Almost Five-Month Low

- Libyan Output Exceeds 1 Million Barrels a Day: Persian Gulf Oil

- U.S. Considering Yemen’s Saleh Request to Visit for Medical Aid

- Aldar Declines as Board Plans to Meet to Discuss Asset Sale

- Saudi Oil Break-Even Price Rise to $71.5 Next Year, NCB Says

- Savola to Sell Stake in Land Plots for $168 Million

- Syria Producing 260,000 Barrels a Day as Oil Sanctions Bite

- Savola Surges Most Since March After Land Sale, Egypt Stake Buys

- Qatar Fertiliser to Supply Mitsubishi Ammonia, Al Raya Says

- Iran Government Saves $15 Billion on Subsidy Cuts, State TV Says

The Hedgeye Macro Team

Howard Penney

Managing Director