No Current European Positions in the Hedgeye Virtual Portfolio

Asset Class Performance:

- Equities: The worst country index performers w/w: Cyprus -10.7%; France -6.3%; Italy -5.9%; Spain -5.2%; Finland -5%; Germany -4.8%. Best performers w/w: Russia (RTSI) +1.2%; Hungary +0.1%; Ireland -50bps; Switzerland -100bps

- FX: The EUR/USD fell -2.7% w/w. Divergences: RUB/EUR +1.2%; HUF/EUR: -90bps

- Fixed Income: 10YR sovereign yields broadly declined w/w, led by Spain -75bps; Belgium -29bps; and Italy -20bps. [We’ll be keying off this coming Monday’s ECB’s SMP weekly bond purchasing report for the prior week for insight into these waning yields. Last week the SMP bought only €635M vs previous weeks in the low single digit billions of EUR – See our European Banking Monitor on Mondays for follow-up].

Call Outs:

The European week was dominated by three themes:

1.) Credit Rating Agencies downgrades on Sovereigns and Banks post S&P’s CreditWatch Negative rating of 15 Eurozone countries on 12/5:

- (12/12) Moody’s says it will review its ratings of all EU sovereigns in Q1

- (12/14) Fitch cuts Credit Agricole 1 level to A+

- (12/15) Fitch cuts ratings of BNP Paribas (to A+ from AA-), Credit Suisse (to A from AA-), Deutsche Bank (to A from AA-), and Barclays (to A from AA-)

- (12/16) Fitch places Belgium, Spain, Italy, Ireland, Slovenia, Cyprus on rating watch negative

Hedgeye’s Take: The three major credit ratings agencies are classic lagging indicators, yet their downgrades of sovereigns and banks will move the market. We’ve long said that France will lose its AAA status. Solving for how the EFSF, a facility built on its AAA credit status, will continue to raise money at favorable levels will be one more headwind for Eurocrats to address.

2.) Lending disagreements on an additional €200B loan to the IMF from global central banks for troubled Eurozone states

- Legally Complex Problems - ECB President Draghi stated in his press conference on 12/8 that “given the spirit of [the EU] treaty, the ECB can’t channel money to circumvent the treaty. If NSBs want to lend to the IMF, which would then lend to say China, that is fine. But if the IMF uses the money to buy bonds in Euroarea, this is not compatible with the treaty.”

- Increased push back from the US, Germany and the UK on contributions

Hedgeye’s Take: Even under a scenario in which €200 Billion was pledged by contributing members (which we think is highly improbable), it, along with €500B (across the EFSF and ESM) is far short of our $2-3 Trillion estimate to support Eurozone banks and sovereigns. The Fiscal Union proposed in the 8-9 December Summit is far from the Bazooka the market is looking for to support intermediate term gains in capital markets.

3.) Russia’s Cabinet Restructuring:

- (12/4) Putin’s United Russia wins a majority of 238 of the 450 seats in the parliament (Duma), but lost 77 seats, ahead of Presidential elections in March

- (12/10-11) 50k+ anti-Putin protesters over the weekend

- (12/12) Billionaire Mikhail Prokhorov announces he will challenge Putin

- (12/14) Boris Gryzlov, the speaker of Russia's State Duma, the lower house of parliament, resigns. He was speaker since 2003 and a loyal ally of Putin’s

Hedgeye’s Take: It’s difficult to sift through where we’ll be in the next weeks and the ultimate outcome in a few months time. Opinion seems very split with the extremes being A) Russia is having a ME moment (and Putin doesn’t have a chance at winning the Presidency) and B) Putin will rule with an iron fist for the next 12 years. While the latter seems more likely to become reality, an important alternative view comes from Paul Starobin in that what we’re seeing is a “popular rejection of a strongman who has overstayed his welcome [Putin]—not a rejection of the model of strongman rule.”

The 50k demonstration over the weekend was impressive, nevertheless there’s no indication we’re at a tipping point yet. Prokhorov entering the ring adds another element given his money, western know-how, and large public profile, however if Starobin is right that there’s no real support for Russian Liberalism, Prokhorov too doesn’t have a chance. (http://www.tnr.com/article/world/98370/post-putin-russia)

Further commentary worth noting:

- Medvedev “is basically toast,” Jan Techau, director of the Brussels-based European center of the Carnegie Endowment for International Peace, said in a telephone interview. “There’s no chance Medvedev will stay on as prime minister, but they can’t just discard him as a member of the inner circle and will find something nice and meaningless for him to do.”

- Medvedev may resign before the end of the year, Otkritie Financial Corp. said in a note to clients. That would allow Putin to become acting president and remain in power rather than resigning his post as premier in the run-up to the election, as required by Russian law, according to economists led by Vladimir Tikhomirov at the brokerage that is partly owned by state-run VTB Group, the country’s second-largest lender.

In a scenario of a Putin defeat, or defeat of a candidate backed by Putin, we think the risk of it being viewed as a destabilizing event is outsized…read global investors pulling out and Ruble weakness. There are also many questions about just who is running the Finance Ministry. Returning to the idea of the Ruble as the world’s reserve currency we think it is very improbable. If any is to take over the USD, it’s the Yuan, but well off in the horizon.

Interestingly, the WTO announced today that it is set to accept Russia as a member after 18 years of negotiations.

Interest Rate Decisions:

(12/14) Norges Bank Cut Benchmark Rate 50bps to 1.75%

(12/15) Switzerland SNB 3M Libor Target Rate UNCH at 0.00%

Chart of the Week:

-We’d caution against getting overly optimistic about the one month positive inflection in the 6M forward looking German ZEW Economic Sentiment number for December. Germany’s largest trading partners remain its European neighbors – so as long as the region is mired in this sovereign debt and banking crisis, trade will continue to contract. Germany’s growth outlook may simply be the best of a decidedly contractionary group in 2012.

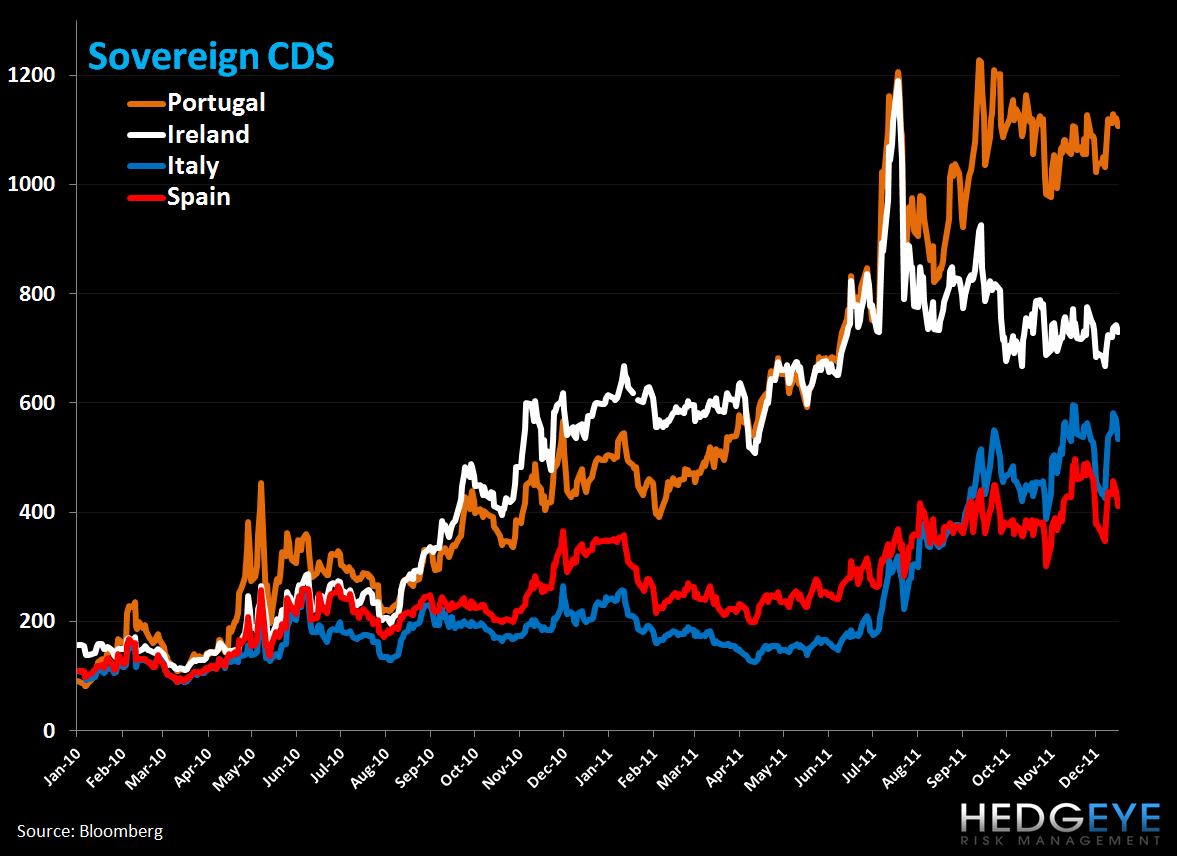

CDS Risk Monitor:

-On a w/w basis, CDS was largely flat across the periphery. Spain saw the largest pullback at -26bps. On a m/m basis, Spanish CDS is down 52bps and Italian CDS is down 37bps.

Data - The West:

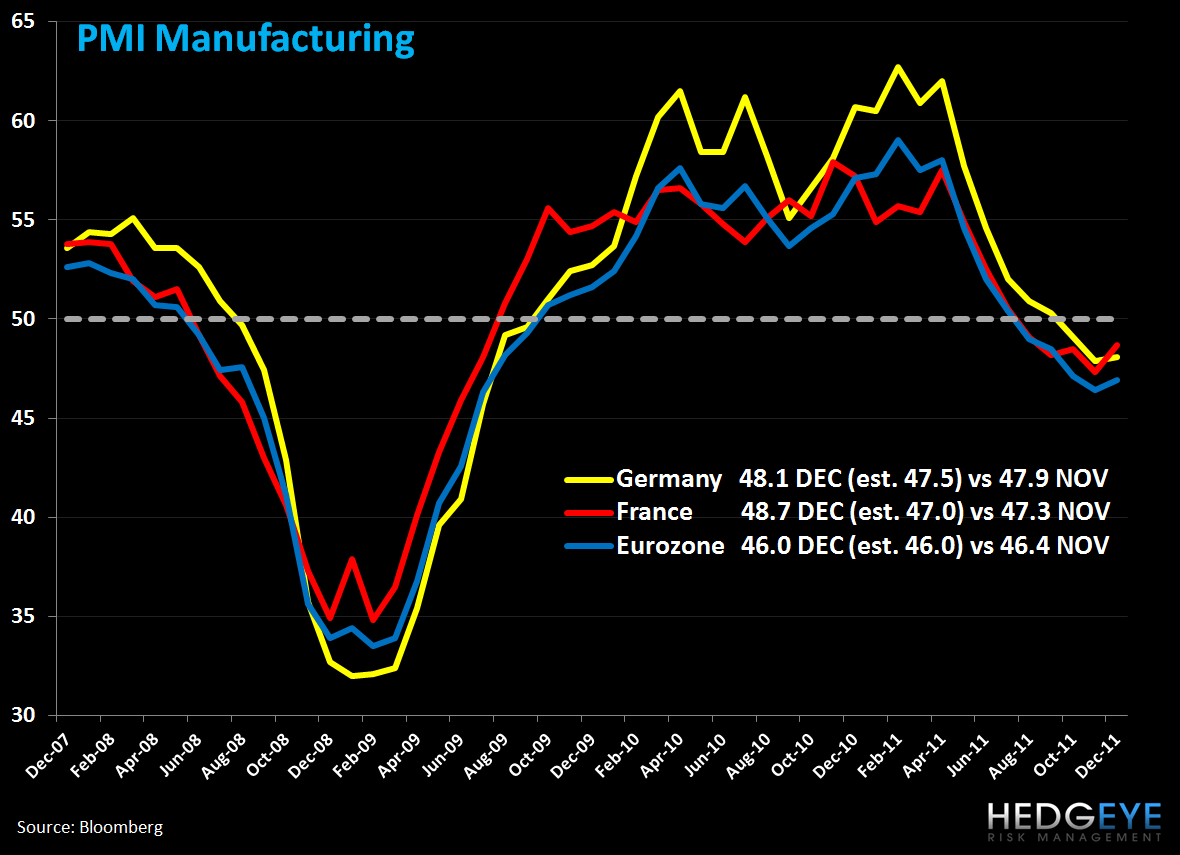

-Dec flash PMIs of Services and Manufacturing came in better than expected, and largely improved M/M, yet remain at or below the 50 line that divides contraction (below 50) and expansion (above).

Eurozone Composite 47.9 DEC vs 47.0 NOV

Eurozone CPI was unch at 3.0% NOV Y/Y vs the previous month

Data - The East:

-ZEW released its December market survey for Eastern Europe (EE). We key off of the 6-month forward looking “Economic Expectations”. Of note is that EE will be held hostage to:

- Weak trade demand from Western Europe (WE)

- Foreign currency loan leverage, in particular to the CHF and EUR, especially as domestic currencies are under pressure

YTD vs EUR:

Polish Zloty -12.0%

Hungarian Forint -8.4%

YTD vs CHF:

Polish Zloty -13.6%

Hungarian Forint -10.0%

Romania Leu -2.7%

Czech Koruna -2.5%

-Alternative View: Could EE and its currencies benefit from capital flows exiting the US and China?

EUR-USD

-We’d short the cross at $1.33 for an immediate term TRADE. The EUR/USD remains broken long term TAIL ($1.40) and intermediate term TREND ($1.42) in our models and we think the lack of resolve from the newest proposals for a fiscal union will encourage greater downside.

The European Week Ahead:

Monday: Oct. Eurozone Current Account; Dec. UK GfK Consumer Confidence Survey

Tuesday: Jan. German GfK Consumer Confidence Survey; Oct. Greek Current Account; Riksbank Interest Rate Announcement

Wednesday: Nov. Dec. Eurozone Consumer Confidence; Bank of England Minutes Released; Q3 Italian GDP

Thursday: Q3 UK GDP and Current Account; Q3 Denmark and Netherlands GDP

Friday: Q3 France GDP and Producer Prices; Dec. Russian Money Supply

Matthew Hedrick

Senior Analyst