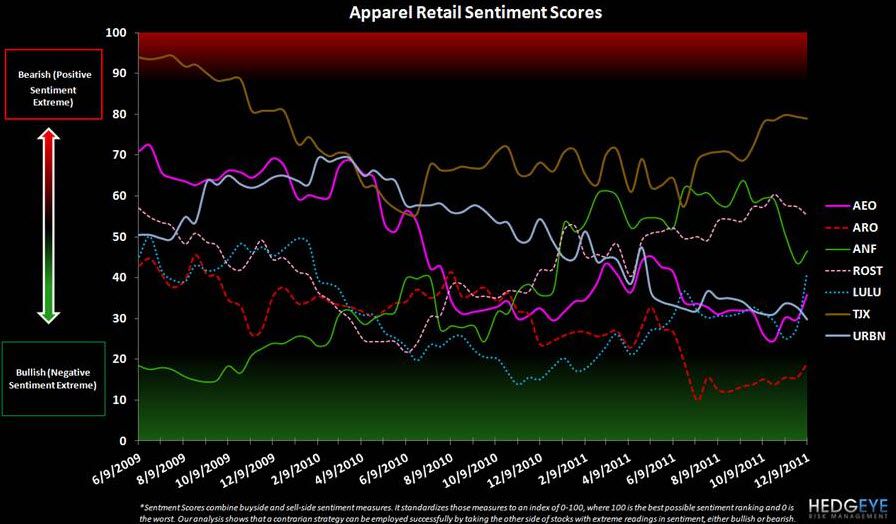

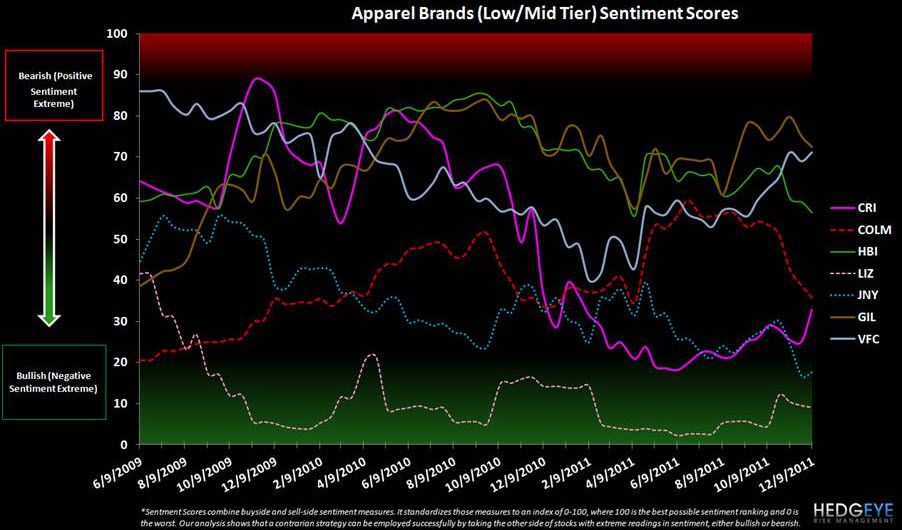

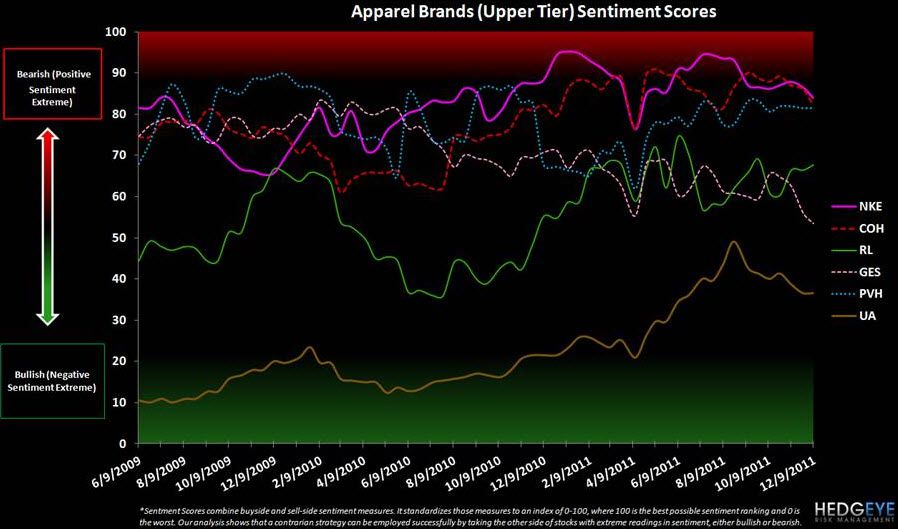

We’re seeing some very notable sentiment changes. Great setup for WMT on the margin. Also looking good – LIZ, GES, COLM, URBN. Negative callouts include M, DECK, TJX. Keep an eye on NKE and JCP. They can go either way.

Here are some interesting callouts in our Hedgeye Retail Sentiment Scoreboard. As a reminder, our Scoreboard combines buy-side and sell-side sentiment measures. It standardizes those measures to an index of 0-100, where 100 is the best possible sentiment ranking and 0 is the worst. We won’t belittle the art of stock picking by implying that simply going counter to what a chart says will make money. But this analysis is heavily quantified, back-tested, and most of all…accurate. We use it as a part of our process to flag the outliers. (Think of it like the manager of a baseball team sending a batter to the plate and starting off with a 2-0 count).

Here are some important notables:

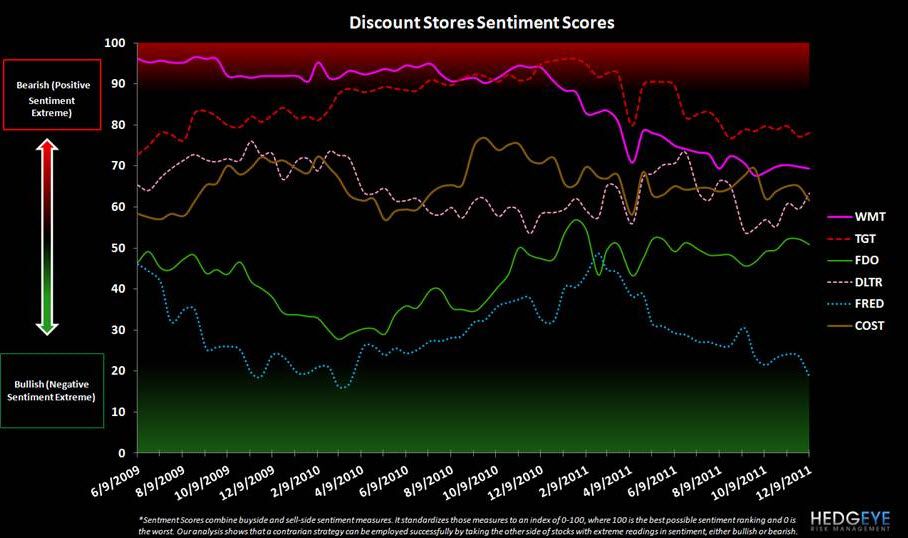

WMT: The fact that WMT went down to 74 from 92 over the past year is stunning – though it appears that this negative trend has stabilized. WMT remains one of our top picks.

NKE: While Nike’s Sentiment has come down meaningfully to 84 from 94 in July, it still has the highest sentiment score on our radar.

URBN: The contrarian bull case has been building for URBN for over a year now. Sentiment has steadily eroded from a high score of 70 down to 30. Now that all the bears are out of hibernation, we think that the incremental shifts will be on the positive side.

LIZ: LIZ was one of our favorites when its score was a 5. A few asset sales later as well as a more clearly defined brand strategy moving forward have gotten more people involved; the score is pushing double digits – but still among the lowest in all of retail (ie people are still not bullish enough).

CRI/GIL/HBI: Scores for the perceived commodity-heavy names improved throughout September and October. More recently however, GIL and HBI have declined sharply while CRI accelerated 8 points last week. Sell-side upgrades and expectations of a minimally promotional holiday shopping season have had no impact on our thesis. We’re still bearish on all three.

LULU: This week’s score jolted up 13 points to 41. The quarter definitely raised flags, but the stock saw immediate upgrades and short covering, which took sentiment higher.

GES: The long term merchandising and geographic opportunities for GES remain positive but short term headwinds in Europe and rising concerns around North America have driven the sentiment score down 10+ points over the past month. As it heads lower, we like it more.

COLM: Over the past 6 weeks, Columbia’s score has deteriorated by 20 points to 36. Someone is making a big negative bet here – likely on its tremendous International exposure (45% of EBIT).

DECK: The perennially bearish sentiment on DECK is now sitting at its most bullish position in years. Are people finally giving in to the idea that UGG is not a fad?

M: Macy’s is hitting peak sentiment. Yes, the name is cheap if you believe numbers. But we don’t believe numbers.

UA: Retraced 10 points over the past two months. Still bearish overall with a score of 40, but not bearish enough.