THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Comments from CEO Keith McCullough

Consensus expectations for a European solution were what failed this week – this will take time.

- CHINA – just a market mess in Asia overnight led by what we know - an acceleration in Growth Slowing in China – Industrial Production came in at +12.4% (lowest report since 2009) and inflation dropped, sequentially, inline w/ our model’s estimate at 4.2%. Deflating The Inflation (positive) will take time too. Chinese stocks hit a 33 month low (down -24.5% from YTD high).

- GERMANY – the most important Global Macro factor to solve for when analyzing a country = GROWTH. The Bundesbank cut their Growth estimate huge this morning for 2012 to 0.6% (from 1.8% prior). European Stagflation is what kills Equity multiples, and there is no central plan that can stop gravity (Growth Slowing). Next line of DAX support = 5776.

- RUSSIA – I’ve been up for 2 hrs and have yet to see or hear someone mention that the Russian stock market is crashing (that doesn’t mean it ceases to exist) – down -4.3% this morning and down -33.5% from YTD high confirming 2 Big Mac-ro calls we had yesterday: A) Strong Dollar and B) Cutting our Asset Allocation to Commodities back to 0%. Brent Oil snapped its TAIL line of $110.42.

With US Stocks down for both November and December, Santa is going to have to have one heck of a rally in the next 2 weeks for us to be wrong. I am hearing that central planners are considering moving the date on Christmas however.

SP500 support 1231; TAIL resistance 1270. Manage your risk around that range.

KM

SUBSECTOR PERFORMANCE

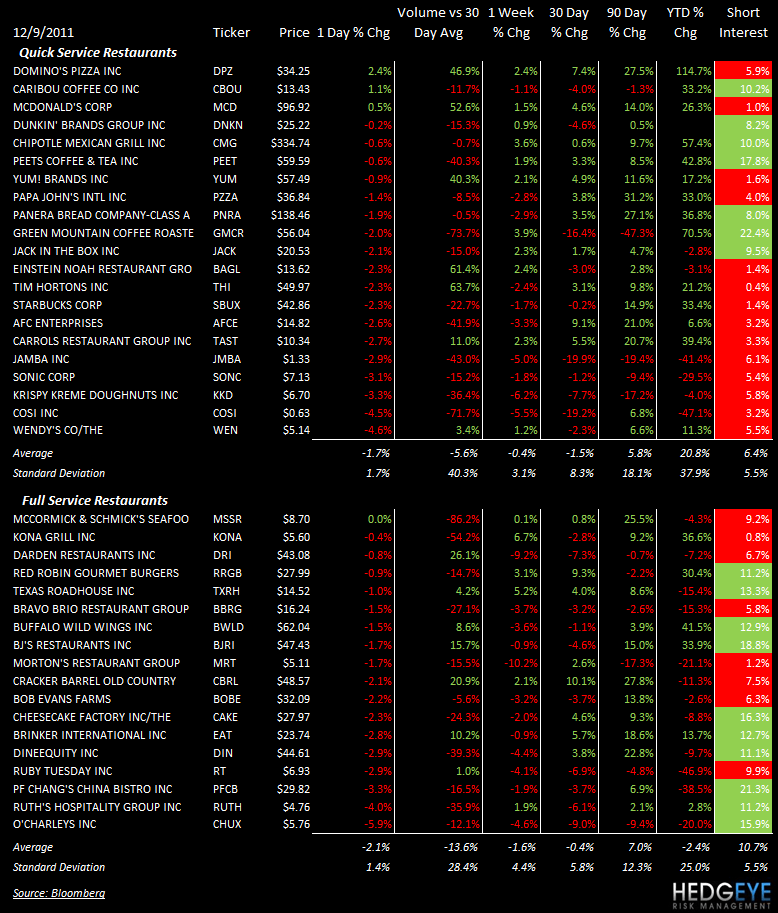

QUICK SERVICE

YUM: Yum! Brands was upgraded from Market Perform to Outperform at Bernstein.

WEN: Wendy’s tweet related to the annual promotion the company does to raise money for the Dave Thomas Foundation for Adoption was the most retweeted tweet in 2011.

Howard Penney

Managing Director

Rory Green

Analyst