Underlying sales trends look quite good for athletics, but the 1 year growth rates are reflecting increasingly difficult comps.

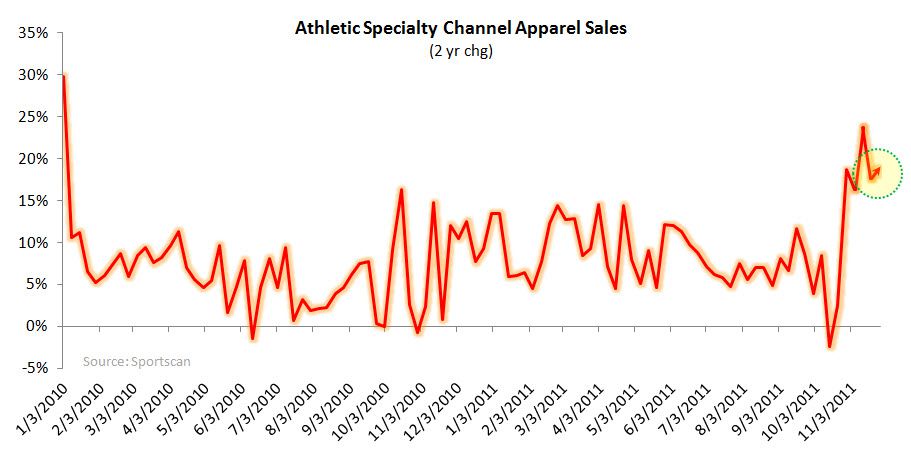

Athletic apparel growth slowed last week as the industry lapped a 20% comp but the underlying trailing 3 week and 2 yr trends accelerated. Alternatively, Footwear trends improved incrementally in spite of tougher year over year compares after three weeks of deteriorating trends. Improvements here are notable as the industry approaches a stretch of easier compares to close out 2011.

Here are some additional highlights on last week’s trends:

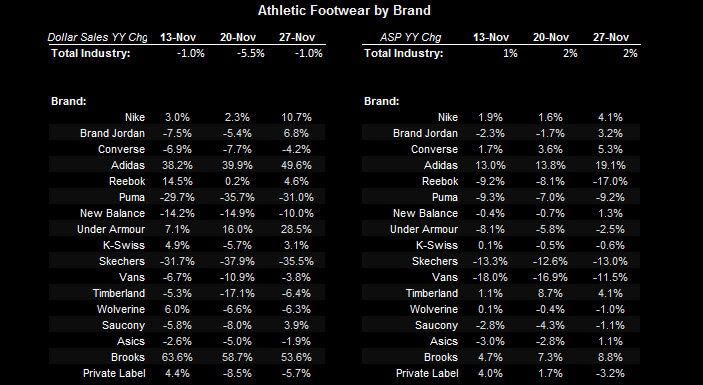

- Nike (including Brand Jordan and Converse) gained an aggregate 416bps of share on a base of 43%. Nike has been a consistent share gainer, but Brand Jordan added an incremental 105bps of share last week

- Basketball footwear has been down since an NBA-prompted slump in sales throughout October, but perked its head into positive territory along with the announcement of the season being brought back from the grave.

- Outerwear, which outperformed in Q3 continues to show strong growth (up 27% last week & 30% YTD) however there was a notable slowdown in the category’s share of athletic apparel (see chart below) which was 13.4% vs. 12% LY. The YoY spread remains up 140 bps however the spread has been running at a full 3 points for 2 months. While the unseasonal ramp in the category’s sales as a percent of total has been hugely positive for VFC (TNF) and COLM, Columbia lost 100 bps of share this week with VFC’s gains slowing to 61 bps. This could be an anomalous week for a trend that will continue through the holidays but it could also be the beginning of the snapback in unit sales as the channel begins to recognize the pull forward in sales

- Champion Sales continue to deteriorate – posting a 17% decline on the week (Champion accounts for ~15% of HBI sales). We highlighted the LSD declines a few weeks back as a potential anomaly however the sharp acceleration to the downside has confirmed a trend here. What’s notable is that Target has noted the strength in Champion’s C9 program, which is exclusive to target. TGT is not represented in this data, which suggests that the company may be robbing Peter to pay Paul. We’ll have to look into this further. If true, definitely not good for HBI.

- The Department Store and Family Retail apparel channels had strong weeks with sales up 18% and 23% respectively on incrementally more difficult comps. These channels only account for an aggregate 25% of the Athletic specialty apparel market but are notable for JCP, M & KSS. The athletic specialty channel’s year over year growth slowed to ~8%, which by any measure is a very healthy rate as it is lapping a 30% compare. Nonetheless, deceleration is what it is. We like FL in the athletic specialty channel; see our recent note "FL: We're Getting more Cautious."