“He saw his parents’ savings melt away.”

-Nicholas Wapshott

Yesterday was not a good day for me. You couldn’t have had a good day if you were having a good month.

Yesterday was not a good day for American, German, or British people who have savings accounts either. That’s what centrally planned policies to inflate do – they punish the conservative saver. They pay the debtor.

Bernanke gets that and so do The German People who are paying the German Government to lend Germany money this morning (short-term yields on German Bunds have gone negative). I guess the upside to the Bernanke model is that 3-month US Treasuries are yielding 0.00%. That way no one wins or loses. Fair share “free-market” capitalism baby.

The aforementioned quote comes from a book I cracked open this past weekend by Nichalas Wapshott titled “Keynes vs Hayek.” Plenty of people have written on this topic since the debate between the two schools of thought emerged in the 1920s. Wapshott’s is the most recent. So far, it’s a healthy reminder of how history rhymes.

I fundamentally believe it’s very difficult for a human being not to superimpose his or her personal experiences in life into the passions of their opinions. Call it context or perspective – it’s all one and the same thing to me. If you’ve studied enough economic history, you provide yourself an opportunity to walk down life’s path in other people’s shoes.

Keynes was born into a British family of the academic elite who found himself scaling the wall of the Ivory Tower by the time he was in his teens, whereas Hayek was more of a commoner solider “in the Austrian army on the Italian front who returned to find his home city of Vienna devastated and its people’s confidence broken.” (Wapshott)

“The Austrians mostly read English and were conversant if not persuaded by the English tradition; the English on the whole could not read German and largely ignored the works of Austrian and German theorists.” (Wapshott)

Hayek wasn’t an elite student. He actually didn’t start studying the “political economy” (reading Marshalian and Keynesian economics) until he went to war. Eventually, his views came to be shaped by his personal experience (inflation melted his parents savings away). His critique of an inconclusive social science experiment (Keynesian Economics) remains as relevant today was it was in the 1920s.

It’s a good thing Einstein figured out how to communicate in English.

Back to the Global Macro Grind…

My introduction this morning isn’t meant to proclaim my mystery of Hayekian faith. I’m not a Republican or a Democrat. I’m not a Keynesian, and I’m not a Hayekian. My name is Keith McCullough and I do my own work.

I do not believe that policies to A) Inflate B) Pile-debt-upon-debt, or C) Bailout losers, is the long-term path to American economic prosperity.

To the contrary, I think debauching the US Dollar does exactly what it did yesterday - it stimulates inflation in asset prices and, as a result, slows Consumption Growth.

US GDP = 71% Consumption Growth.

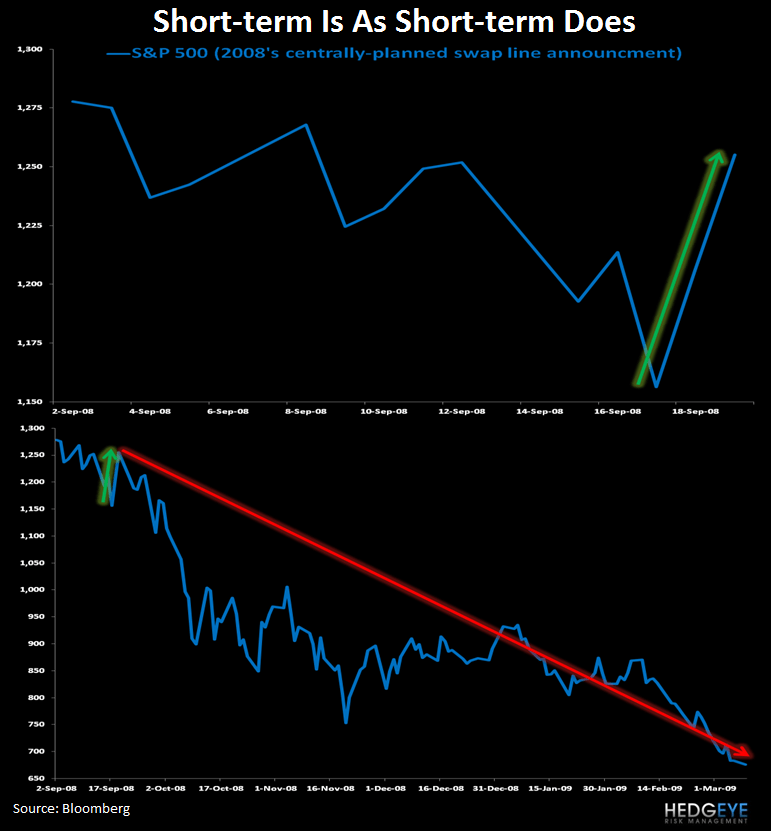

Last time Brent Oil prices spiked like this, US GDP Growth slowed to 0.36% (Q1 of this year). And while that seems like a long time ago versus yesterday’s no-volume stock market reflation, that is not something I am going to let the Keynesians forget.

It’s the Policy To Inflate, Stupid.

As the US Dollar strengthened throughout Q2 and Q3, we saw some Deflation of The Inflation and, presto! US GDP growth recovered sequentially:

- Q111 US GDP Growth = 0.36%

- Q211 US GDP Growth = +1.34%

- Q311 US GDP Growth = +2.01%

The interconnectedness doesn’t lie; central planners do.

And no, I don’t feel shame in calling out these policies to inflate as stupid. Forrest Gump could tell you that stupid is as stupid does too. And there are a lot of “smart” people in the Ivory Towers of Keynesian economic forecasting that don’t look so smart anymore.

The economy is a globally interconnected ecosystem that could not care less about the short-term “political economy” of a few European bankers yesterday who begged Bernanke for a bailout.

The Global Economy of supply and demand ticks on this morning (in real-time):

- China reported their lowest level of manufacturing (PMI) strength since 2009 (47.7 for NOV PMI vs 50.4 OCT)

- Britain reported their lowest level of manufacturing (PMI) since June of 2009

- South Korea reported a 3-month high in inflation (CPI) of 4.2% NOV vs +3.6% OCT

Growth Slowing and Inflation Rising. Do the Keynesians get it? They will when they see Q4 US GDP Growth Slow, sequentially, again like it did in Q1 as Consumption Growth slows.

In the meantime, while there seems to be a language barrier between Mr. Macro Market’s real-time messaging and the Fed’s central mandate for “full employment and price stability”, the common man’s savings are being melted away as the precious few pander to their banking losses being saved.

My immediate-term support and resistance levels for Gold (back above $1736 TRADE support), Brent Oil (Bullish Formation), France’s CAC40 (Bearish Formation), and the SP500 (bullish TRADE; bearish TAIL) are now $1, $109.42-111.37, 3074-3208, and 1, respectively.

Best of luck out there in December,

KM

Keith R. McCullough

Chief Executive Officer