This note was originally published at 8am on November 25, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Capitalism isn’t scarce; vision is.”

-Sam Walton

Get GDP Growth and the US Dollar right and you’ll get mostly everything else right. Happy Thanksgiving.

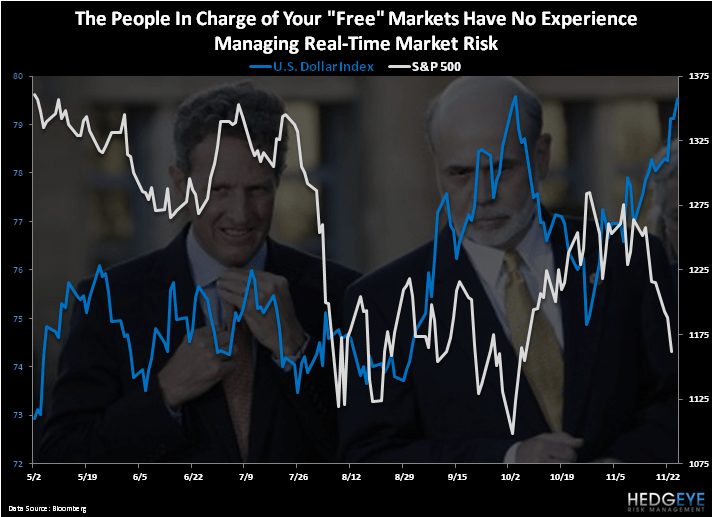

The US Dollar is up another +0.5% this morning to $79.52 on the US Dollar Index, taking its week-to-date gain to +1.7%, and its cumulative gain since Bernanke signaled the end of Quantitative Guessing II to +8.9% (since April).

Given the generationally high inverse-correlations between the US Dollar Index and everything else, we continue to see what we’ve coined as a Correlation Crash across asset classes as a direct result of this bullish Buck Breakout.

This morning’s Global Macro Grind amplifies the deep simplicity of this risk management point:

- S&P Futures are down another 9 handles to 1150 = down -15.6% since the US Dollar stopped going down in April

- EUR/USD testing its early October lows of $1.32

- European Equities selling off, across the board, to down -22-42% since February-April (pick your country)

- Asian Stocks continuing their crash (down > 20% from their YTD highs) with HK and India down -27.5% and -23.5%

- Commodities breaking down toward their October lows as the CRB Index’s correlation to the USD = -0.82

- Gold is down another -1.1% to $1679 = down -11.6% from its all-time high in August

Correlation does not always imply causality. We get that.

But A) sometimes it does and B) it can be very reflexive in the immediate to intermediate-term.

Keynesian economists/strategists try to avoid Soros’ concept of “Reflexivity” in markets and economies as much as Global Macro investors are avoiding the Hungarian-American’s birthplace this morning (Hungary’s stock market trading down -4.6% after Moody’s cut Hungary’s credit rating to junk).

Academic types have a hard time using markets as leading indicators because they have no experience managing real-time market risk. That’s a problem - a really big problem with US economic policy.

Policy = Causality.

That’s why you’ve never heard Ben Bernanke or Tim Geithner use these 2 words - Correlation Risk – to attempt to explain anything about nothing that’s happening in either Global Macro markets or the economies that underpin them.

Accepting responsibility for causality, after all, would be an admission of failed policy. At least Greenspan admitted this in 2008. Maybe Bernanke will by the time he is retired from the Fed too…

The Germans kind of get this. That’s primarily because they have to. The German People will not give the fiscally conservative leadership of the Bundesbank a hall pass on forgetting the history of hyper-inflation. At least not yet.

German stocks are down another -0.54% this morning, taking the DAX down to 5398 (down -28.2% since the US and German stock markets put in their 2011 YTD highs). If the SP500 was down that much from its April 2011 closing high (1363), it would be trading at 979 this morning. The German People aren’t as hyper about their stock market as our manic media culture is.

If I’ve said this 100 times in the last 4 years, I’ve written and/or said it 1000 times – the immediate to intermediate-term moves in a country’s stock market does not exclusively reflect a country’s long-term health. Currency stability, inflations/deflations, and employment levels are, collectively, much better long-term barometers for purchasing power and prosperity.

I could write a book about that – and maybe I will – but that’s not going to happen in the remaining 10 minutes I have to finish this note this morning. So hopefully it continues to provide a basis for long-term economic debate.

The Scarce Vision that policy makers in this country have displayed over the course of the last decade is not what we should be thankful for this Thanksgiving. What we should all be thankful for is a generational opportunity in America to change that.

My immediate-term support and resistance ranges for Gold (bearish TRADE and TREND), Brent Oil (bearish TRADE and TREND), German DAX (Bearish Formation) and the SP500 (Bearish Formation) are now $1657-1724, $105.13-109.98, 5243-5657, and 1154-1196, respectively. With the US Dollar immediate-term TRADE overbought today, plenty of market prices will be oversold.

Happy Thanksgiving to you and your loved ones,

KM

Keith R. McCullough

Chief Executive Officer