THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Notes from CEO Keith McCullough

After Roubini called for Euro “parity” and the Euro appeared on the cover of The Economist (on fire) last wk, the US Dollar was immediate-term overbought and Euro oversold – shocking.

- ASIA – mini-meltup in the markets that have been going down the most (HK, India, Korea – all up +2-3% overnight) as China and Indonesia didn’t care much to rally at all (closing up 0.12% and 0.27%, respectively). Asian Growth is still slowing and all Asian markets remain in Bearish Formations (bearish on all 3 of my risk management durations)

- EURO – immediate-term TRADE oversold at 1.32 is as oversold does (we covered our Euro short there) – now you get the bounce back up toward a lower-high of immediate-term resistance (1.34). Take your time with this and use the USD as your front-runner to fade the Global Macro market’s beta.

- COMMODITIES – same Global Macro trade (Correlation Risk) that’s associated with the USD; what went down last week goes up this morning (with the USD down) – important immediate-term TRADE lines of resistance I am watching are Gold $1726 and Copper $3.45. If both fail there, both are shorts.

Don’t forget that last week was the worst Thanksgiving week for US stocks since 1932 (not a good reference pt, fyi). The SP500 would have to close > 1203 for me to not be selling on green today. Covered all but 6 short positions last wk, so now we can re-populate the bench.

KM

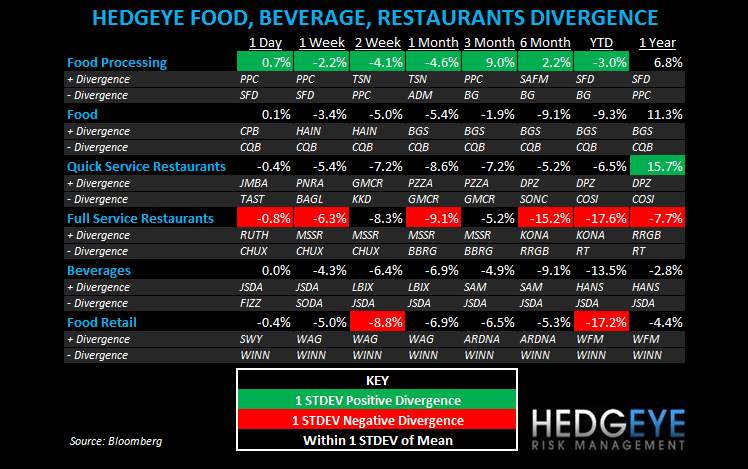

SUBSECTOR PERFORMANCE

QUICK SERVICE

PNRA: Panera Bread is opening its second Manhattan location in 1Q12 after leasing a 4,556 square foot unit at 10 Union Square East in New York.

YUM: Yum! Brands has reached an agreement with Sinopec to open drive-through outlets at its gas stations and expressway service stations in China. Zhu Zongyi, President of Yum! Brands China Division, said, “We expect to expand our business in southwest China because that’s where social economic development is moving and we will open more in Chengdu in the New Year.”

Howard Penney

Managing Director

Rory Green

Analyst