“In a time of turbulence and change, it is more true than ever that knowledge is power.”

-John F. Kennedy

Contextualizing market moves within the scope of Global Macro fundamentals is as critical right now as it’s ever been. That’s why we built a firm around our multi-factor, multi-duration, Global Macro risk management process.

Every morning we wake up at the same time and do the same thing. We Embrace Uncertainty. Functionally, what that means is that price, volatility, and volume factors strike our models on a real-time basis – and we accept them for what they are.

Much like the rain and tide pounding the contour of an ocean line, what you end up seeing is what you get – patterns. Time and patterns create a series of probabilities, scenarios, and ranges. This is how we apply Chaos Theory to markets.

Back to the Global Macro Grind…

This morning’s embrace of uncertainty issued me a not-so-friendly risk management kiss. I’m in a hotel room on the road – and that’s not cool coming from a laptop. But I guess that’s too bad for me – the market doesn’t care about how I am positioned.

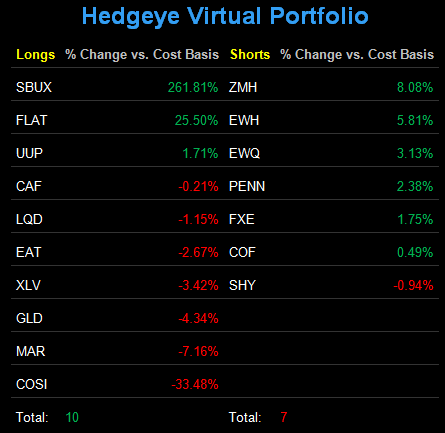

I am long the US Dollar and short the Euro.

The Germans decided to support the Euro this morning by telling the rest of the world’s Bailout Beggars to go pound sand. This isn’t the kind of sand in Benoit Mandelbrot’s fractal model (falling one grain at time). This is the big beachhead of fluffy expectations stuff.

“We don’t have any new bazooka to pull out of the bag… we see no alternative to the policy we are following… we need to tell markets very clearly – and this must be done soon – that there is no other way forward than the one we’re pursuing.” –Michael Meister

Meister, one of Merkel’s senior guys, went on to add that if Italian and the French central planners don’t like that, they can go pound some more sand, and “sit tight through the turbulence.”

The Euro finally bounced on that (I know – how dare the Germans defend the common currency and purchasing power of their people!), rallying straight back up to an immediate-term TRADE zone of resistance ($1.35-1.36).

In turn, the US Dollar sold off, holding immediate-term TRADE support of $77.07 (US Dollar Index).

Thankfully, it will take more than one morning, week, or month of Powerful Turbulence to take me out of this globally interconnected game of risk. Pursuing its outcomes is what I love to do. And I love being long our King Dollar theme on red.

Dollar Down = reflation of some of yesterday’s deflation. Dollar up = Deflates The Inflation.

Since 71% of US GDP = Consumption, that’s what we need to see more of to bring growth back in the country – not another super-committee of central planners. Newt has that part of it right.

Strong Dollar = Strong America. Period.

While that may create some Powerful Turbulence in the stock market in the short-run, in the long-run most of our children and grandchildren won’t be dead.

The short-run performance of the stock market doesn’t reflect the long-term health of the country – full employment and price stability do.

US stocks are down -12.5%, -7.6%, and -5.6% from their April, October, and November highs, respectively. Volatility (VIX) is up +120% since April’s SP500 price of 1363. Unemployment in America hasn’t moved off of 9%.

Having learned the 1920s lessons of structural unemployment and price volatility the hard way, maybe there’s a part of this that the Germans have right for the long-run too.

My immediate-term support and resistance ranges for Gold, Oil, German DAX, and the SP500 are now $1, $95.35-98.42, 5, and 1186-1203, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer