THE HEDGEYE BREAKFAST MONITOR

MACRO NOTES

Consumer

Initial jobless claims came in at 388k versus 395k consensus and a revised 393k the week prior.

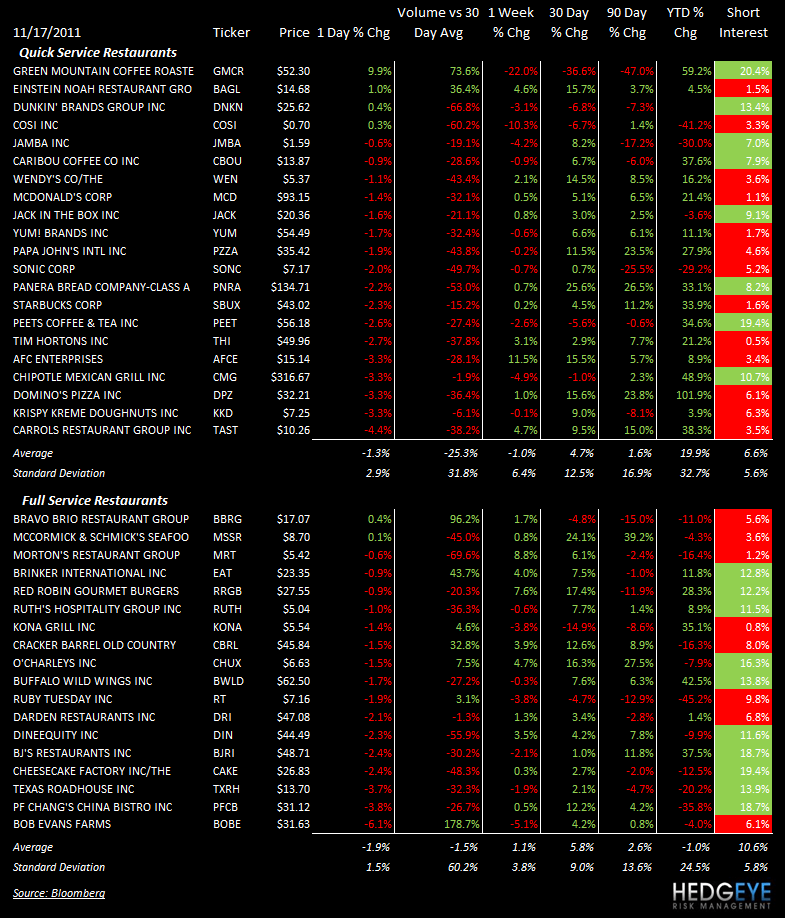

SUBSECTOR PERFORMANCE

QUICK SERVICE

DNKN: Dunkin Brands priced its secondary offering, previously announced on November 1st, at $25.62. In addition, the underwriters have been granted a thirty-day option to purchase up to an additional 3.3 million shares from certain of the selling stockholders.

WEN: Wendy’s is launching the “W” cheeseburger. As we wrote in our Commodity Chartbook, published this morning, WEN and other companies exposed to spot market beef costs are likely to be impacted by what the supply and demand dynamics seem to suggest will be higher prices in 2012.

CASUAL DINING

BWLD: Buffalo Wild Wings announced yesterday that it plans to buy 15 franchise units in Ohio and South Carolina.

Howard Penney

Managing Director

Rory Green

Analyst