While it appears this morning’s meeting is well-attended, I think others may be underestimating the importance of today’s meeting.

Today in Raleigh, N.C., senior management is showcasing a converted Chili’s. 14 of the 15 restaurants in the market have been converted. It appears that management is very happy with the results they are seeing. My feeling is that some members of the investment community could be underestimating the importance of this meeting; the entire Brinker management team is here including Chief Executive Officer, Doug Brooks.

Having spent the better part of yesterday evening in the remodeled Chili’s talking to regional managers and other employees, I get the sense that there is a lot of positive momentum at the Chili’s brand. I understand that management has a lot riding on the turnaround but it seems that their enthusiasm is matched by the positive energy among rank-and-file employees. It is one of those intangibles that are impossible to quantify but the turnaround initiatives would fail without it.

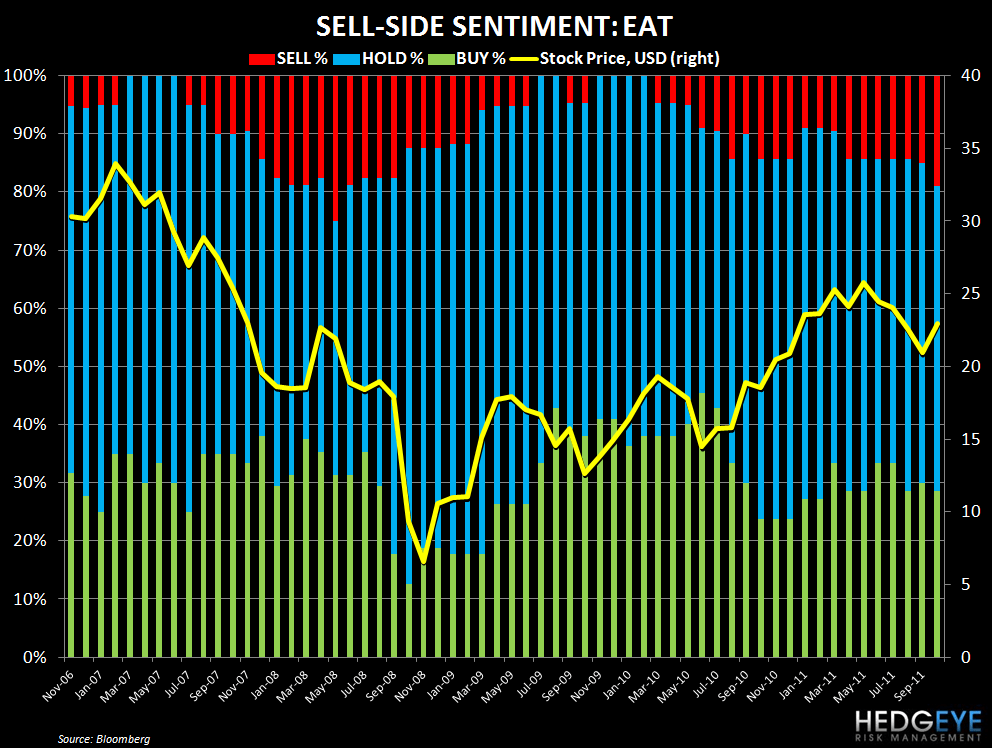

I estimate that October’s Knapp Track Comparable Sales two-year average slowed by 75 basis points from September to 0.85%. I think that a greater proportion of this decline is attributable to Applebee’s than Chili’s. Next to PFCB, EAT remains one of the more controversial names in the restaurant space as the sell-side remains polarized over the company’s ability to sustain current trends. I believe that the company could be in the early stages of a sustained recovery.

Two net positives that could help the stock in the short run are:

(1) The operating performance put it in “nirvana” which should allow for a multiple expansion over time.

(2) The sell-side is very bearish on the name, despite the company taking market share from Applebee’s.

The meeting starts shortly.

Howard Penney

Managing Director

Rory Green

Analyst