Positions in Europe: Short EUR-USD (FXE); Short France (EWQ)

Crowds cheered the news of Italian PM Silvio Berlusconi’s resignation and Mario Monti’s appointment on Saturday, however let’s not forget what’s left in the balance—public debt at 120% of GDP; pushback on austerity that will not help to curb the deficit; a technocrat government in which new elections aren’t scheduled UNTIL early 2013; debt maturities north of €200 Billion over the next 6 months; poor growth prospects that should result in declining tax revenue; worries about core Italian bank leverage to European sovereign paper; rising government bond yields increasing the cost to raise capital; and market participants looking for a quick fix to Italy’s (and the rest of Europe’s) problems with a quick flick of the wrist.

The Italian economy and more broadly European capital markets are going to need Super Mario to save the day—well frankly, we don’t think Mario squared (+Mario Draghi) can save the day. Don’t forget that we don’t have any major planned catalysts into year-end around which Europe’s unanswered questions: expansion (leverage) of the EFSF, bank recapitalization, Greek haircuts will be solved for.

Talks that China would come to Europe’s rescue have faded—not surprisingly given the less obvious benefit to them—and the expansion of the role of the ECB and IMF are still undecided.

Today, at her Christian Democratic Union party’s annual congress in the eastern German city of Leipzig, German Chancellor Angela Merkel told leaders they must create a “new Europe” by deepening ties in the 27-nation EU, yet reiterated her rejection of jointly sold euro bonds.

She said: “The task of our generation now is to complete the economic and currency union in Europe and, step by step, create a political union… It’s time for a breakthrough to a new Europe… If the euro fails, Europe fails.”

In response, we don’t want to discount the resolve of Eurocrats to maintain the Eurozone project—after all the last two years have proven this out well—however we do want to sound the horn that the credit markets are telling a very different story around the risk of this very project. And more rhetoric without action is going to see investors punish most European capital markets.

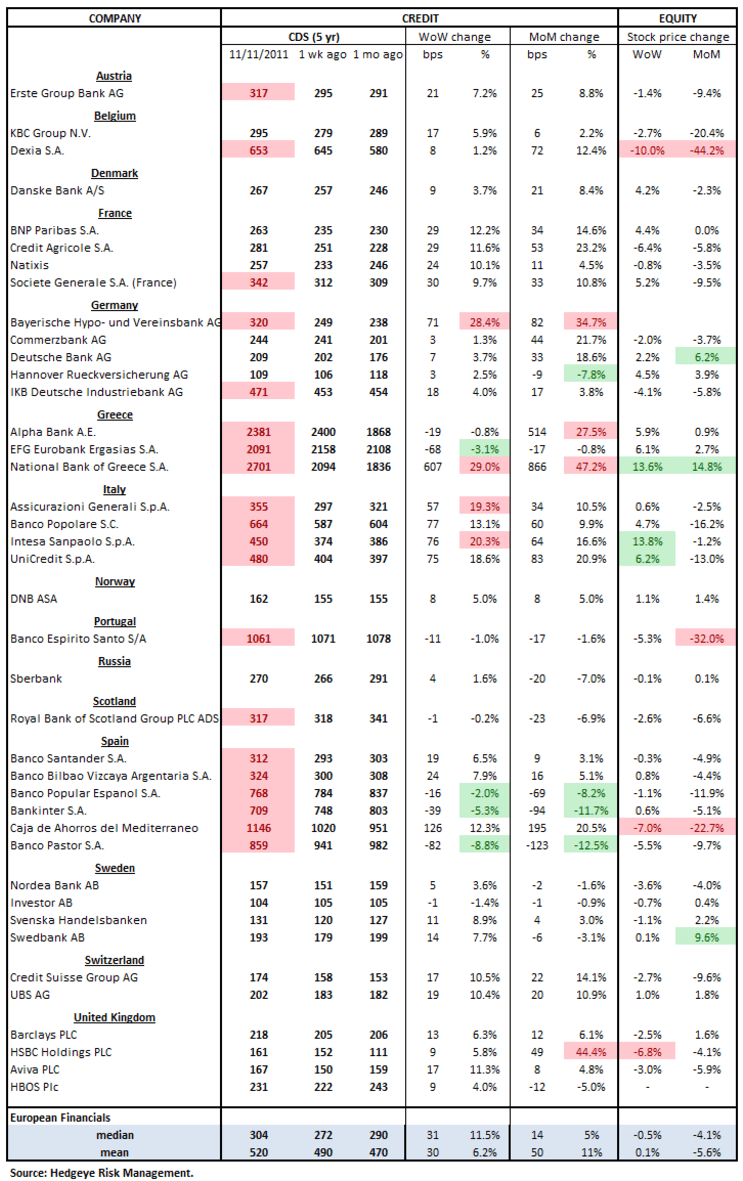

Our weekly European Risk Monitors are included below. We remain short the EUR-USD via (FXE), which remains broken TRADE ($1.37), TREND ($1.42), and TAIL ($1.40), and short France (EWQ) in the Hedgeye Virtual Portfolio. For more specifics on both positions, see our recent work on the Hedgeye portal.

European Sovereign Yields – European 10YR yields were mostly higher last week. Greek yields shot up 228bps, Spain +44bps, Italy +35, while Portugal declined -62bps and Germany -12bps. As always, we’re keying off the 6% Lehman line as a critical breakout line. Italy has held tight above the 6% for the last three weeks, currently at 6.57%.

In its SMP bond purchasing program, the ECB bought €4.5 Billion in secondary bonds last week (vs €9.5B in the week prior), taking the total program to €187 Billion. Look for Super Mario (Draghi) to increasing buying alongside heightening Italian yields.

European Sovereign CDS – European sovereign swaps mostly widened last week. Spanish sovereign swaps widened by 7% (+28 bps to 427) and French by 11% (+20 bps to 202).

European Financials CDS Monitor – Bank swaps were wider in Europe last week for 32 of the 40 reference entities. The average widening was 6.2% and the median widening was 11.5%. The German bank Bayerische Hypo- und Vereinsbank saw swaps widen by almost 30%. In addition, the four Italian banks we track saw swaps widen an average of 18%.

Matthew Hedrick

Senior Analyst