November GGR forecast revised up to HK$21-22BN

This past week, average daily table revenue increased sharply to HK$781 million versus HK$639 million last week. We expect the current week to slow again since many VIP players stay away from Macau during the Grand Prix celebration (race is on Saturday). However, with Cotai somewhat immune to the congestion, the slowdown may not be as pronounced as in prior years and we should see a market share shift away from the peninsula. We are projecting full month GGR (including slots) of $21-22 billion (+25-31% YoY) with a bias at the high end of that range.

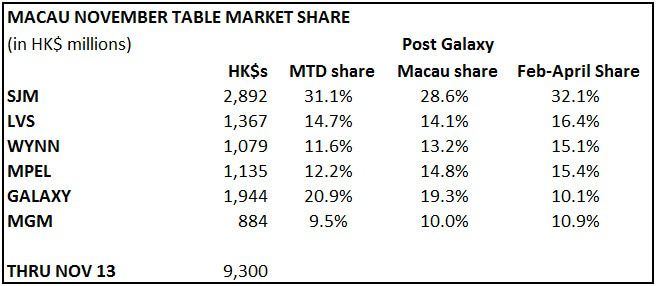

SJM was the clear market share winner, a nice reversal from last year’s hold-affected decline. We think SJM is holding around 3.5% month to date. On the low end, MPEL held around 2.5% at both Altira and CoD so far in November, dragging down overall share. MPEL bears should control their enthusiasm, however. We think MPEL is on pace for over US$200 million in EBITDA and over US$220 million in hold adjusted EBITDA. Street consensus is only US$195 million.