THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - November 9, 2011

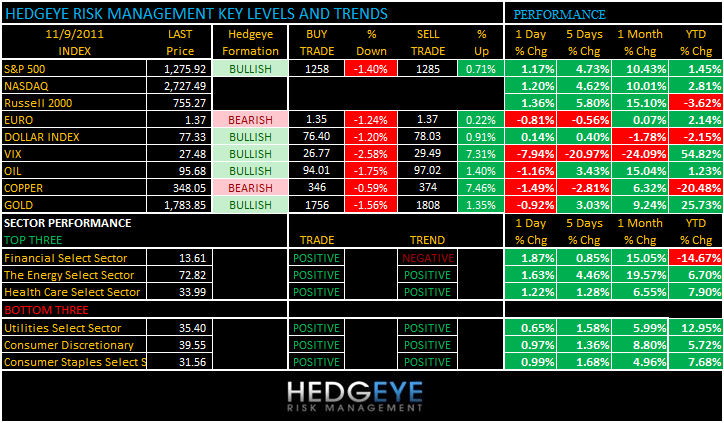

As bad as Hedgeye was positioned from a Global Macro perspective into yesterday’s close will be as well positioned as I am this morning. As we look at today’s set up for the S&P 500, the range is 27 points or -1.40% downside to 1258 and 0.71% upside to 1285.

SECTOR AND GLOBAL PERFORMANCE

In the very immediate-term, bullish is as bullish does. If I were to use a 1-factor model (like the 200-day moving average), there would be no mincing of those words as of tonight’s close. Fortunately, I’ve learned not to use 1-factor/1 duration models.

The bottom line from here is that VOLUME and VOLATILITY signals need to confirm this PRICE move to make it 3 for 3 on the factors that matter to me most (Price/Volume/Volatility). PRICE was a head-fake at the October 31stclosing high of 1285, so stay tuned.

Yesterday’s volume was 25% below the 30-day average. Today’s was down -13%. Tomorrow we need to see the juice. Volatility’s TREND and TAIL lines of support are 26.77 and 22.11, respectively.

All 9 Sectors in this model are bullish immediate-term TRADE (that’s not new) and 7 of 9 are bullish TREND (Financials and Basic Materials are the 2 bears on TREND and TAIL – Small Caps (Russell 2000) are also bearish TAIL w/ resistance up at 778. The SP500’s TAIL line remains 1268.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1459 (+1153)

- VOLUME: NYSE 879.63 (+12.38%)

- VIX: 27.48 -7.94 YTD PERFORMANCE: +54.82%

- SPX PUT/CALL RATIO: 1.91 from 2.30 (16.85%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – long-bond investors in the US have not been suckered into this hope that Global Growth is just fine. 10yr yields already broke the TRADE line of 2.12 supports last week (that’s why we are were long TLT) and are trading 1.98% last as the Yield Spread compression continues.

- TED SPREAD: 44.42

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.10 from 2.04

- YIELD CURVE: 1.85 from 1.79

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage (prior 0.2%)

- 9:30am: Bernanke speaks at Fed conference on small business

- 10am: Wholesale inventories, est. 0.5% (prior 0.4%)

- 10:30am: DoE inventories

- 12:15pm: Fed’s Tarullo speaks on regulation in NY

- 1pm: U.S. to sell $24b in 10yr notes

WHAT TO WATCH:

- Italian 2-yr note yield rises above 7%, more than 10-yr rate

- Ohio voters repealed a law limiting collective bargaining for public employee

- HSBC said outlook for global economy is “challenging”, profit at its investment bank shrank by 53%

- American Airlines, its pilots union said the two sides may reach a labor agreement within days

- President Obama to meet with Portuguese President Anibal Cavaco Silva, then speak at National Women’s Law Center

- SEC’s Robert Khuzami speaks at National Conference on the Foreign Corrupt Practices Act, 8:45am

COMMODITY/GROWTH EXPECTATION

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Aluminum Slump Means 25% of Smelters Losing Money: Commodities

- Noble Said to Plan $700 Million IPO for Agriculture Business

- ArcelorMittal Outlook Cut to Negative by S&P on Steel Market

- Oil Increases a Sixth Day as Iran Nuclear Work Poses Supply Risk

- Sand Like Gold Boosts Greenbrier’s Railcar Production: Freight

- U.K. Gas Spread to U.S. Rises on Japan Demand: Chart of the Day

- Nestle Uses Sandbags as Thai Floods Threaten 322 Factories

- Wilmar’s Profit Misses Estimates on Foreign-Exchange Losses

- MF Global Settlement Over Losses in Doubt After Bankruptcy

- Diesel Ending Biggest Gain in Asia Since March: Energy Markets

- Oil Drops on Concern Italy’s Turmoil May Derail European Economy

- Copper Advances First Day in Four as China Inflation Cools

- China Aluminum Output Falls to Eight-Month Low; Copper Drops

- Freeport Indonesia Workers to Extend Strike for Third Month

- Corn Futures Advance on Concern USDA May Lower Harvest Estimate

- Sumitomo Risk Unit Asia Clients Up 67% as Europe, U.S. Slow

- MF Global Commodity Traders Ask Permission to Access Cash

CURRENCIES

EUROPEAN MARKETS

ITALY – ring the royal Rubicon’s gong – because how people are chasing beta around this Berlusconi event is a certified gong show. They loved chasing yesterday’s US Equity close, now they hate everything Italy. Bond yields have gong parabolic as the MIB Index snaps its only remaining line of support (TRADE line of 15,894). Italy is crashing don’t forget – down -34.5% since its YTD high. Bullish?

ASIAN MARKETS

CHINA – Growth continues to slow. Period. Not falling off a cliff slow, but slower is what matters in our macro model and we don’t see Chinese GDP growth arresting the slope of its decline until Q1 of 2012. Inflation data came in right on our estimate at 5.5%, but look for that to shoot up again sequentially in November with Oil prices up here.

MIDDLE EAST

MOST POPULAR MIDDLE EAST HEADLINES FROM BLOOMBERG

- Israel May Lack Capability for Effective Iran Military Strike

- Iran Continued Nuclear Weapons Work Seeking Warhead Design

- Oil Increases a Sixth Day as Iran Nuclear Work Poses Supply Risk

- Syrian Monitoring Project May End as Italy Firm Weighs Options

- Iran Nuclear Report Prompts U.S., Europe to Move for Sanctions

- Qatar Dismisses Architect Concern on World Cup Air-Conditioning

- U.K. Regulator Levies Highest-Ever Fine Against Dubai Investor

- Dubai Shares Rise as Berlusconi Quit Offer Boosts Europe Outlook

- Aluminium Bahrain Racketeering Case Against Alcoa Reopened

- Standard Bank Wins U.K. Case Against Saudi Billionaire Over Loan

- U.A.E. Stock Markets May Allow Short-Selling in First Half

- OPEC Boosts 2015 Oil Demand Forecast Following ‘Swift’ Recovery

- Iran’s Ahmadinejad Says He Won’t Retreat From Nuclear Program

- Abu Dhabi Islamic Bank to Hold Investor Meetings for Sukuk Sale

- Gulf General Reports Third-Quarter Loss as Finance Costs Rise

- Iran 'Will Not Budge' From Nuclear Path, Says Mahmoud Ahmadinejad

- OPEC to Account for 51 Percent of Oil Supply by 2035, IEA Says

- Mideast Oil-Tanker Charters May Reach 2011 High, Marex Says

The Hedgeye Macro Team

Howard Penney

Managing Director