THE HEDGEYE BREAKFAST MENU

Notable MACRO data points, news items, and price action pertaining to the restaurant space.

MACRO

There is a great article by Jonathan Maze on Private Equity's Mixed Track Record in the Restaurant Finance Monitor - “The buyout boom years of 2005 to 2007 haven't been good to private equity buyers of restaurant chains. In that period, those investors, buoyed by cheap debt, bought up numerous chains around the country. Yet of the 35 restaurants they bought in those years, 11 have gone bankrupt, and two others are in distress”.

CONSUMER

The employment situation in October was largely unchanged with the unemployment rate dropping slightly to 9.0% from 9.1% prior and the Labor Force Participation Rate was unchanged at 64.2%. Private Payrolls came in below expectations at 104k versus 125k expectations. September’s number was revised from 137k to 191k.

We will be following up with a post this morning on important employment trends that pertain to the restaurant space in particular.

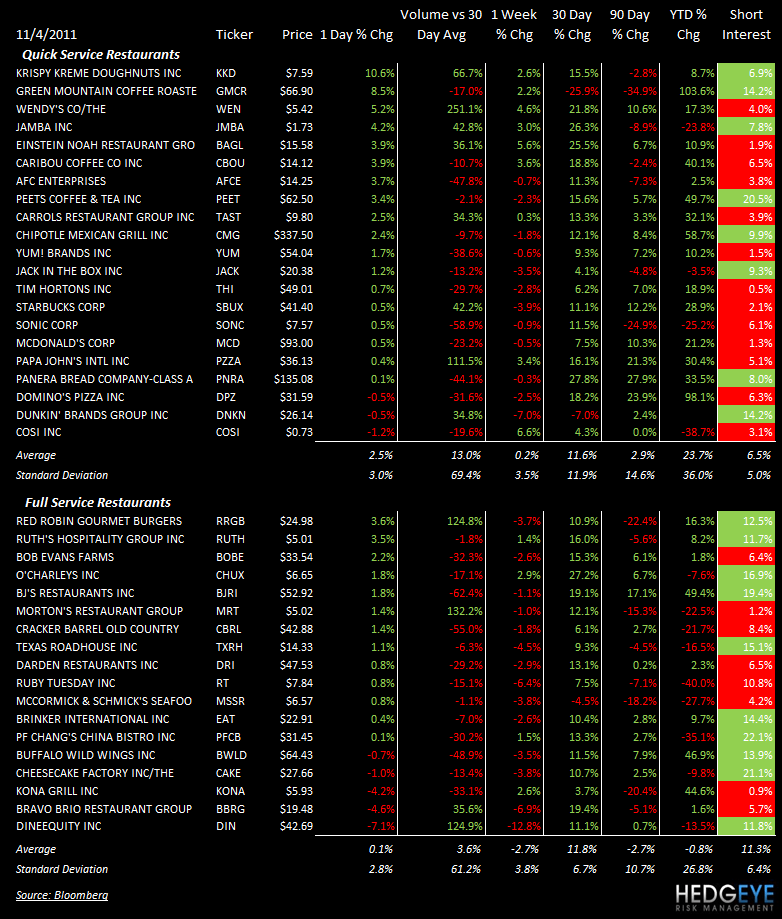

SUB-SECTOR PERFORMANCE

QUICK SERVICE

SBUX: As we wrote this morning, Starbucks posted strong 4QFY11 earnings last night and mentioned that business has been strong in Canada. Tim Horton’s must be feeling the heat. Tim Horton’s has announced the launch of its new specialty coffees, which will soon be available at more than 2,500 locations across Canada. The company said it's the biggest specialty coffee roll out ever in the country. Starting at $2, the lineup includes lattes, mocha lattes and cappuccinos made with premium espresso.

WEN: Wendy’s continues to trade well. We believe that sales at the concept are strengthening.

Howard Penney

Managing Director

Rory Green

Analyst