The important commodities, at least for the restaurant industry, moved higher over the last week. Tellingly, corn moved higher despite outside market pressure.

Please scroll down to view the charts below the commentary.

STOCK THOUGHTS

Corn is an important commodity for all of the restaurants that we cover because either the companies have direct exposure or have exposure to protein costs (which are driven by feed costs). Corn has moved higher despite outside market pressure from the strong dollar, weak equity market, and weak crude prices. At the SAFM Investor Day recently, we learned that Illinois has the largest corn crop relative to its annual ethanol capacity of the major corn-producing states. Therefore, Illinois is a good state to monitor watch in terms of its corn crop fundamentals. News emerging today that the USDA has declared 44 Illinois counties disaster areas due to the effects of drought is bullish for the price of corn and negative for restaurant margins. Farmers and ranchers in an additional 33 counties also qualify for assistance because they are contiguous to the affected areas. The impact of dry summer weather is impacting much of North America’s corn and cattle country.

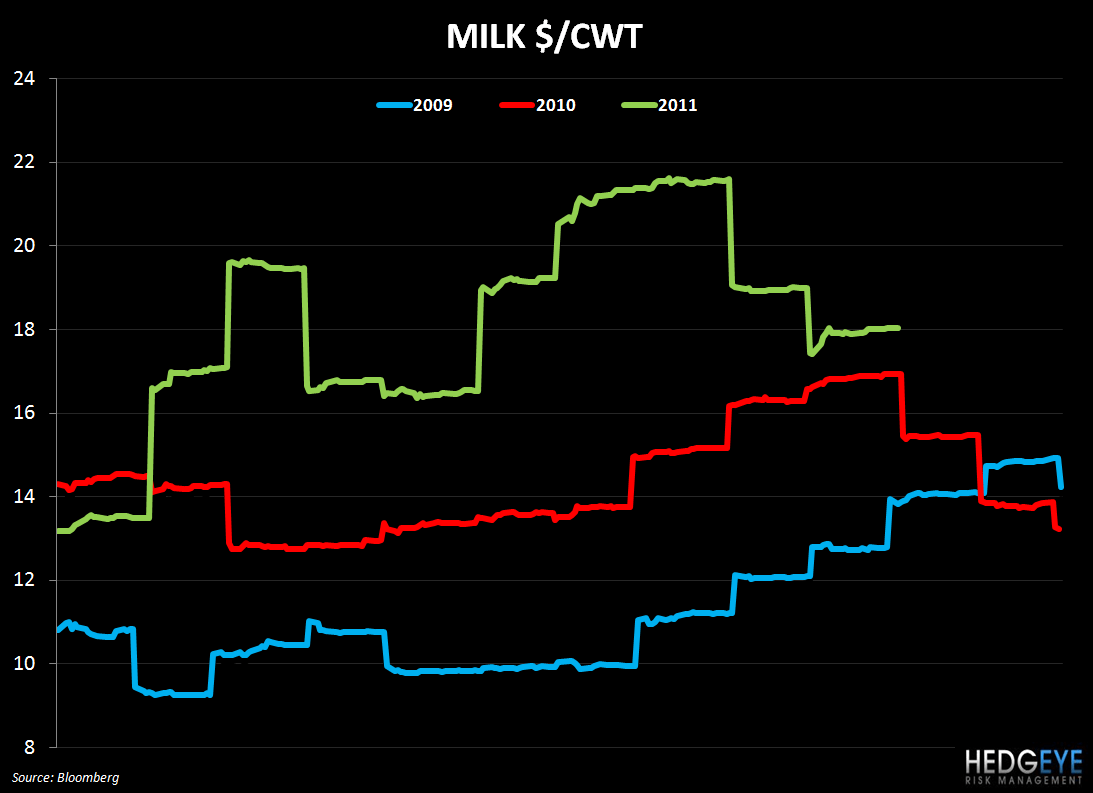

Cheese prices gaining 4.2% week-over-week is a negative for CAKE, DPZ, and PZZA given that all three have (varied degrees of) exposure to dairy prices in the fourth quarter. CAKE had guided to year-over-year deflation in dairy for the fourth quarter but, despite significant volatility, it seems that dairy may be a headwind for the company in the fourth quarter.

Chicken wing prices have continued their march higher. As we wrote recently, food industry experts’ commentary as well as our own analysis gives us confidence that BWLD could have year-over-year inflation in wing prices beginning in the first quarter of 2012. Replicating the 3Q11 strategy of driving comps via a promotion would be difficult in 2012 if the company faces significant inflation. Some industry experts see $1.50 wings next year and sustained year-over-year inflation versus 2011 next year.

Coffee prices have been moving lower on the dollar strength and economic concerns stemming from Europe.

CORRELATION TABLE

CHARTS

Coffee

Corn

Wheat

Beef

Chicken Whole Breast

Chicken Wings

Cheese

Milk

Howard Penney

Managing Director

Rory Green

Analyst