TODAY’S S&P 500 SET-UP - November 2, 2011

72 handles and -5.6% lower in the SP500 from where we shorted them at 326PM EST on Thursday – now what? As we look at today’s set up for the S&P 500, the range is 35 points or -0.43% downside to 1213 and 2.44% upside to 1248.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

Bullish sentiment increases to 43.2% from 40.0% in the latest US Investor's Intelligence poll; Bearish sentiment down to 36.8% from 37.9%

- ADVANCE/DECLINE LINE: -2153 (-245)

- VOLUME: NYSE 1329.21 (+16.29%)

- VIX: 32.92 +16.05% YTD PERFORMANCE: +95.89%

- SPX PUT/CALL RATIO: 2.29 from 3.02 (-23.99%)

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES: just ran the "but growth is good" camp right over as 10yr yields snap my TRADE line of 2.11% support

- TED SPREAD: 43.68

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 2.01 from 2.17

- YIELD CURVE: 1.78 from 1.92

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage, prior 4.9%

- 7:30pm: Challenger Job Cuts

- 8:15am: ADP Employment, est. 100k, prior 91k

- 10:30am: DoE inventories

- 12:30pm: FOMC Rate Decision

- 2:15pm: Bernanke speaks at Fed press conference

WHAT TO WATCH:

- European leaders convene emergency talks today to tell Greece there is no alternative to budget cuts imposed in bailout plan

- Greek PM Papandreou said referendum on Europe’s rescue package will confirm the nation’s membership of the euro

- Bill Ackman said he isn’t pushing for sale of Canadian Pacific Railway

COMMODITY/GROWTH EXPECTATION

Gold continues to hold TREND line support - new range = 1; back to bullish bias in our model

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- MF Global Funds Are All Accounted For, Lawyer Tells Judge

- Top Gold Forecasters See Rally to Record by March: Commodities

- Paulson Clients to Pull Less Than 8% in Year-End Redemptions

- MF Global Didn’t Segregate Client Collateral, CME Group Says

- Greenlight’s Einhorn Bets Mining Companies Will Beat Gold

- Oil Gains on European Debt Talks as U.S. Fuel Stockpiles Decline

- U.K. Oil Service Stocks Cheap Vs Brent Price: Chart of the Day

- Copper Gains for First Day in Three as LME Stockpiles Decrease

- Gold Gains for Second Day as Debt Crisis Increases Haven Demand

- Oil Falls a Fourth Day on Concern Greek Vote Raises Default Risk

- Saudi Top-Oil Premiums Set to Drop With Naphtha: Energy Markets

- China Copper Demand Growth to Slow Further, Antaike Says

- Bell Financial Seeks to Transfer Positions With MF Global

- Sumitomo Forecasts Copper Price Drop, Seeks Iron and Coal Assets

- Soybeans Climb on Speculation 17% Slump May Attract Importers

- Kinross Misses Gold Rally With October Plunge: Canada Credit

- Copper Climbs in London Before U.S. ADP Jobs Report: LME Preview

- Freeport Says Milling at Indonesia Mine Suspended Since Oct. 22

- Oil Falls a Fourth Day on Concern Greek Vote Raises Default Risk

CURRENCIES

EURO – get the EUR/USD pair right and you’ll get mostly everything else right – that’s glaringly obvious right now in our correlation risk model. I covered the short EUR position at TRADE line support of 1.36 yest and will look to re-short 1.39-1.40 TAIL resistance after the ECB doesn’t cut as much as hoped tomorrow. Bernanke debauchery day for the USD side of the trade will be in full effect for today too.

EUROPEAN MARKETS

Inclusive of a generational squeeze, remember Germany's DAX and France's CAC are down -22% and -26%, respectively from their YTD highs

EUROPE: major breakdowns in the DAX and CAC not recovered this morn; after this last lift in the Euro; European stocks to resume crash

FRANCE – not only did the CAC40 fail at my TREND line of 3401 resistance in the last week, but now it has moved right back into a Bearish Formation (bearish TRADE, TREND, and TAIL) – given that French banks and their super sovereign rating all need to be downgraded further, this makes sense; don’t forget the CAC is still crashing (down -26% from its YTD high inclusive of the squeeze)

ASIAN MARKETS

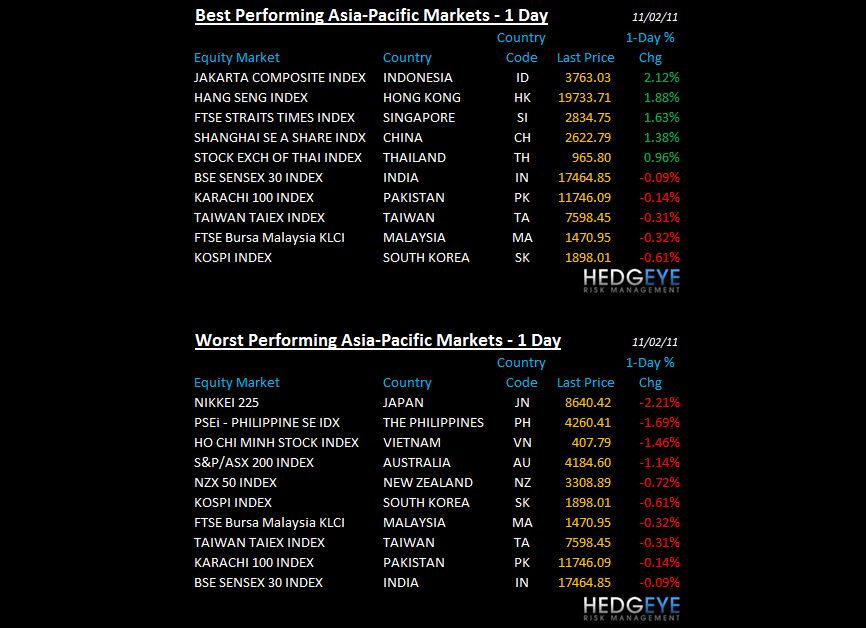

ASIA: stealth move continues in China with stocks up +1.4% on the A-shares and up 7 of the last 8 days; Japan not good.

Australia September building approvals (13.6%) m/m vs cons (4.5%).

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director