P.F. Chang’s reported a disappointing third quarter results before the market this morning. Our takeaways from the numbers and the conference call that followed only confirm our cautious stance on the stock. We believe that the acceleration of unit growth of Pei Wei restaurants with poor fundamental performance is – simply – a mistake. The company’s answer to a question on the possibility of store closures was particularly telling in that our interpretation was that it was not a strong possibility. Like Tennyson’s light brigade, PFCB is not reasoning why – or at least not reasoning enough.

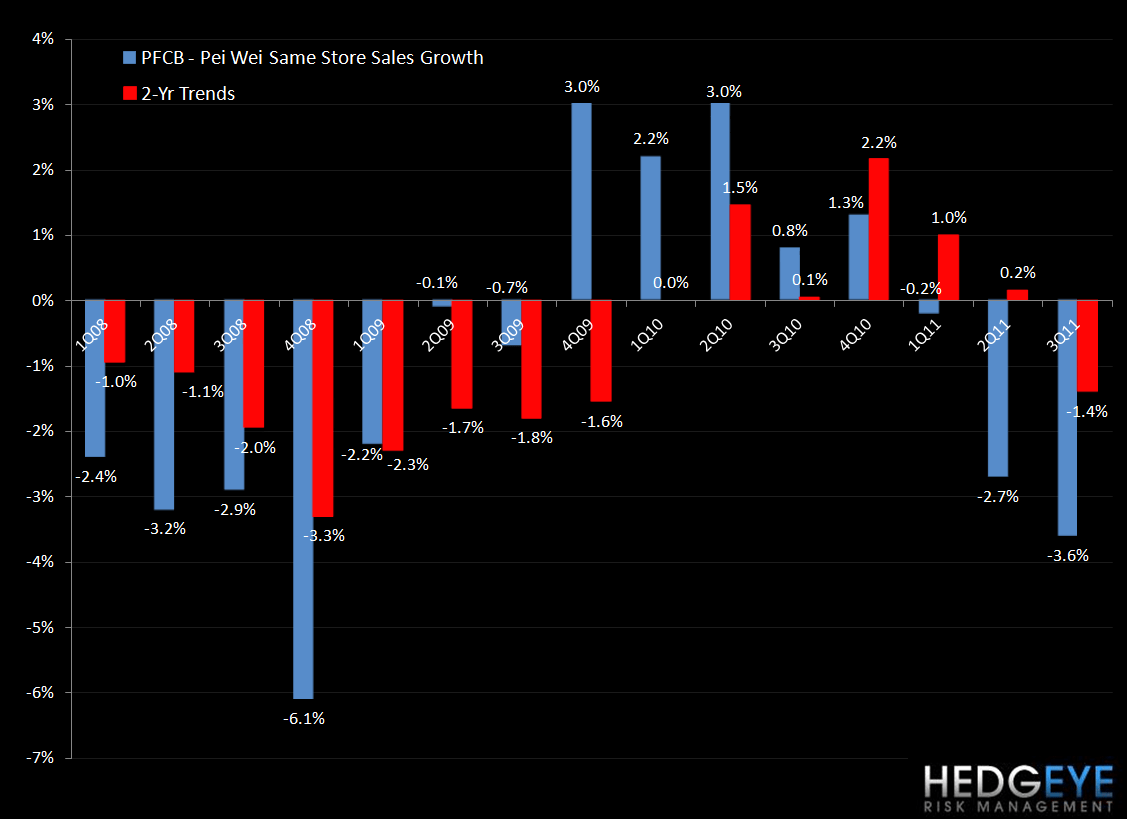

PFCB’s stock has been beaten up badly over the last six months as concerns mounted over softening sales and then continued as the trend failed to reverse. The two charts below show a fairly unmistakable downward trajectory in both concepts’ comparable sales trends.

From a margin perspective, the company experienced inflation in the quarter of approximately 50 basis points due to beef, broccoli, and Asian import prices offset by the benefit of a contractual price rebate on poultry. Without the 50 basis point impact from the poultry rebate, cost of sales would have been up more than 100 basis points, but still in line with 4-5% company expectations for the quarter. Operating costs were negatively impacted by supplies and printing costs related to Happy Hour, according to management. Restaurant operating margins decreased 340 basis points at the Bistro and 200 basis points at Pei Wei. The charts below show, first, the margin contraction that the company has seen in restaurant operating income and, second, that the company is in our “Deep Hole”, that is to say it is operating with negative same-store sales and declining margins. Until we have conviction that the company is turning around one or both of these metrics, we would not consider it on the long side.

We do not subscribe to the belief that the company can continue to grow at the rate that it is with the fundamentals behind the concepts being so poor.

TOP TAKEAWAYS FROM THE EARNINGS CALL:

- Management faces a struggle to drive traffic and seems to be trying many different things at once in order to do so. Initiatives like small plates at Pei Wei for $3.95 and other lower priced menu offerings are having initial success driving some traffic while not damaging check. It seems that progress on this front is slow as October’s trends are also soft. The -3.7% comp at the Bistro in 3Q11 was against a +2.3% print in 3Q10. October 2011 is trending at roughly -3% versus a +0.8% comp in October 2010.

- Despite Pei Wei’s poor performance, management is opening 16-20 new Pei Wei restaurants in 2012. Year-to-date, there have been two Pei Wei’s opened and no more are projected for the remainder of the year in domestic markets. The company maintains that new stores are performing at-or-above system average revenue levels. Focusing on closing underperforming stores, or unilaterally rectifying any issues the concept is having, is likely a better use of time and cash than accelerating expansion. There is a pipeline that management is confident in but growing the store base is not a strategy that we believe will address the obvious issues being felt in many markets. In responding to a question on closing underperforming stores, management didn’t seem to be thinking along those lines at all.

- SG&A was $13 million versus $23 million last year. $8 million of the decline was due to lower share based compensation and lower incentive comp at all concepts and the Home Office.

- Inflation in 2012 is expected to be level, or even higher than, what the company has been experiencing during the second half of 2011.

- No doubt inspired by the success of EAT in driving the lunch day part, the Bistro will roll out a new lunch menu to an entire market. Pending the success of this test, a system-wide rollout of the initiative will proceed in 1Q12.

- Sell-side sentiment has gotten more bearish of late but there is precedent for a continuation of this trade. See chart below.

Howard Penney

Managing Director

Rory Green

Analyst