As we like to say at Hedgeye, markets don’t lie; politicians do.

Having said that, the quantitative set up for the Hedgeye sector models have all nine sectors bullish from an immediate-term TRADE perspective. Yesterday, Healthcare (XLV) joined four other sectors in the Bullish TRADE and TREND camp.

Keith’s models favor Utilities (+10.8% YTD), Consumer Discretionary (+6.7% YTD) and Healthcare (+6.7% YTD) on the long side. Market prices are saying that the consumer looks good, but the macro data continues to look challenged. As prolonged as the jobless malaise has been for consumers, it could be getting worse.

As a word of caution, consumers have not stopped spending and many well-positioned companies continue to post strong results. However, the anemic job and income growth, stock market volatility, falling house prices, elevated gasoline prices, and soft consumer confidence are all reasons for concern.

RETAIL SALES TRENDS - Today, after four weeks of little change, the ICSC chain store index surprised by posting a sizable decline and came despite seasonably cool weather, which should have supported sales trends. The 0.8% decline brought year-over-year growth to 2.4%, its lowest reading since mid-June. The ICSC noted weak customer traffic at all types of retailers during the week. Year-over-year growth softened as well, although it will take more than one soft week to suggest a change in behavior. Trend spending growth is nearly 3%, where it has been much of the year, with the exception of a dip in June and a jump in July.

HOUSING – The Hedgeye Financials team published a note today titled, “Case-Shiller Better, But Not Good Enough”. The Case-Shiller Home Price Index posted a -3.8% decline y/y in August versus -4.2% y/y in July on a non-seasonally-adjusted basis. This sequential improvement wasn't enough to live up to expectations, which were looking for a -3.5% y/y decline. Drilling down to the city level, 17 of the 20 cities showed improvement on a year-over-year basis between July and August. Atlanta, Las Vegas, and Miami were the exceptions. The Financials team likes ITB as a good short it is the US Home Construction ETF. It is similar to XHB but has a larger exposure to the builders themselves as opposed to home goods retailers and other non-builder components.

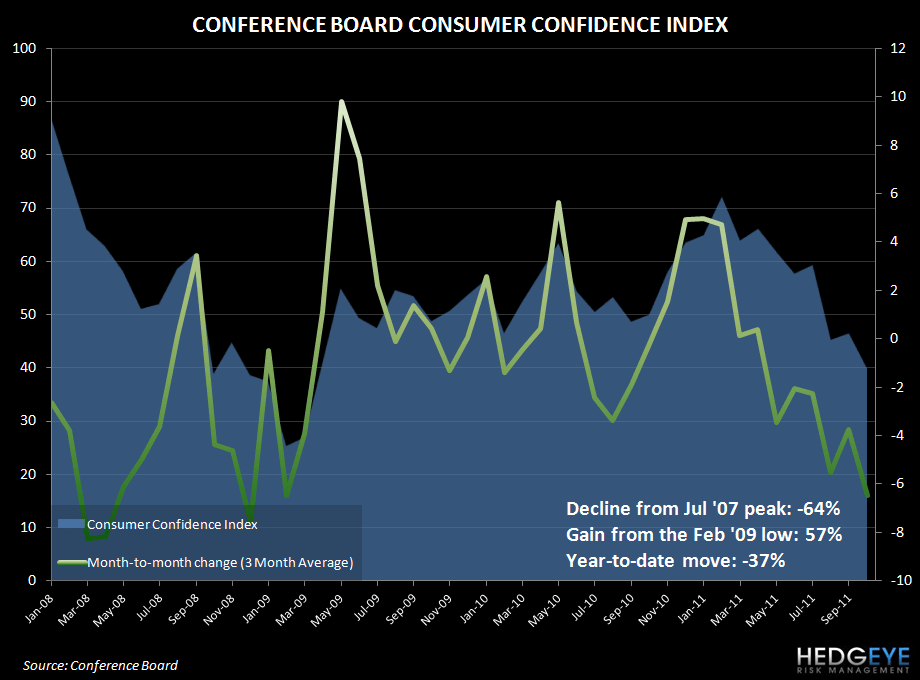

CONFIDENCE – This morning’s print was a bomb, clearly. The Conference Board’s Consumer Confidence Index decreased to 39.8 from a revised 46.4 reading in September. Tellingly, this month’s reading was less than the most pessimistic forecast in the Bloomberg survey. The expectations component fell to 48.7 from 55.1 (previously 54). The present situation component fell to 26.3 from 33.3 (previously 32.5).

RICHMOND FED - The composite index was unchanged from September at -6. Details of the survey said that the employment declined for the first time since September 2010, as the index plummeted 14 points to -7 - the lowest level since November 2009.

The market seems hyper-focused on the European debacle and, by comparison, the issues in the United States may seem less threatening. The macro trends are not encouraging and earnings season, which is far from over of course, has been less than reassuring with results from 3M this morning not corroborating with the view many are holding that fears of sluggish economic growth are overblown. The company said on its earnings call this morning that it expects sales trends in 4Q to be flat versus 3Q.

Howard Penney

Managing Director