Positions in Europe: Short EUR-USD (FXE)

The Eurocrats will be kicking the can further down the road... Based on comments from this weekend’s EU Summit, the tea leaves suggest this Wednesday’s second Summit meeting will underwhelm market expectations. The read-through from this weekend is that the ECB remains firm in not playing ball—that is taking on balance sheet risk to support (leverage) the EFSF; banks are responsible for recapitalizing themselves; and no guidance on the haircuts (exact percentage) banks should take on Greek holdings.

In order, this portends:

On the ECB: So long as the ECB is not going to directly support bolstering the EFSF, we don’t see any hope of expanding the facility in short order. The most recent example is the grave effort it took (months) for member states to ratify the July 21st EFSF, which didn’t even boost the current size of the facility.

The ECB continues its sovereign bond purchasing program [SMP], buying €4.49B in the week ended October 21st (vs €2.24B Oct. 14) of program’s total €169.5B, however with 10YR yields on Italian bonds trading right at the 6%, we’re not optimistic that this program can contain Italy’s sovereign risk (more below).

On Bank Recaps: In typical Eurocrat form, comments suggest banks will be responsible for recapitalizing themselves. No measures were offered in the very likely case that not all banks can accomplish this (risk management?). If the market is going to feel comfortable with this “plan”, there will need to be firm mandates on the size, scope, and timing of these recapitalization, as well as secondary plans should the banks not be able to accomplish the recap themselves. What are the nationalization strategies? How will the EFSF contribute to support banks when such measures have never been clearly outline, and more importantly, the facility is undercapitalized to support banks and sovereigns across the region? The web of cross-country exposures and derivative impact makes answering these questions all the more difficult.

On Greek Haircuts: Sarkozy said that “on the question of Greece, things are moving along. We’re not there yet”. There’s still no specific guidance on the haircut international lenders should assume, at 21% (as proposal 3 months ago) or closer to the 50-60% range supported by the German camp.

Remember, any haircut on Greek debt will be a technical default, so Eurocrats will continue to tip-toe around the subject/define it in all terms other than what it is, as to shield issues around the constitutionality of a default within the Eurozone, as there’s no specific language that provides guidance for debt default/”forgiveness” in any of the major treaties.

----

Given the above we expect to be underwhelmed by Wednesday’s meeting to produce any form of a “Bazooka” to cure Europe’s entire sovereign and banking ills. For more see our note on 10/20 titled “Italy’s 10YR at 6.02% Ahead of EU Summit”. We’re short the EUR-USD (FXE) in the Hedgeye Virtual Portfolio for this very reason.

Risk Metrics

As is typical for Mondays, below are our risk metrics across the sovereigns and banks. You’ll note that yields and CDS spreads on the sovereigns are continue to trend up and to the right, with critical focus now on Italy and Spain’s 10YR bond yield, the former which rose to 6.02% last Thursday. As a reminder, we flag the 6% level on 10YR government bonds as a historically significant level. When Greece, Portugal and Ireland broke through this level, yields shot up expediently and the individual countries required a bailout in short order. And this time around there’s no facility large enough to bailout Italy, which is sitting on €1.9Trillion of debt, or a Spain, or a large nation requiring assistance to prop up its banking sector.

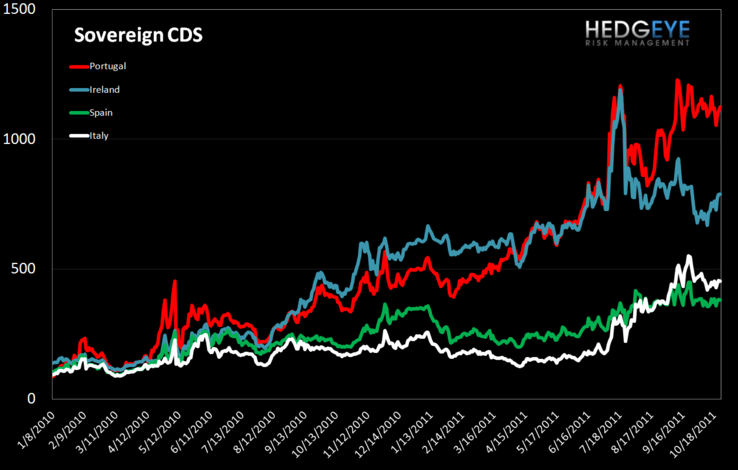

European Sovereign CDS – European sovereign swaps widened slightly last week. Only German and American spreads tightened. American spreads tightened by 12%. French swaps widened 6.4% to 192 from 180.

European Financials CDS Monitor – Bank swaps were mixed in Europe last week, with swaps tightened for 21 of the 40 reference entities. Greek banks were the worst performers, as Alpha Bank A.E. and EFG Eurobank Ergasias S.A widened 30% and 15.2% respectively. German banks also saw deteriorations, with swaps widening an average of 7.5% WoW.

Matthew Hedrick

Senior Analyst