THE HEDGEYE BREAKFAST MONITOR

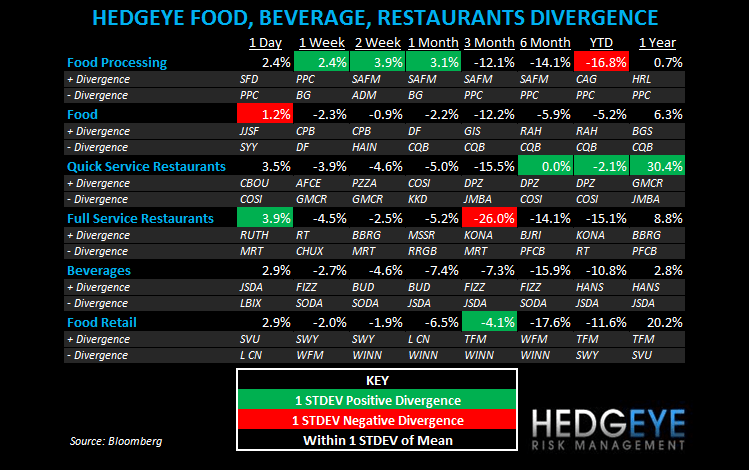

SUBSECTOR PERFORMANCE

On yesterday’s short-covering opportunity, which yesterday’s Early Look had predicted, casual dining outperformed peer subsectors. Food processors saw more muted gains on the day but continue to trade well as grain costs slide.

QUICK SERVICE

YUM reported earnings yesterday after the close. EPS beat expectations by a penny, coming in at $0.83. The stock is trading down premarket due to concerns about the quality of the beat (tax rate) and China margin pressure. China comps accelerated to +19%, confirming our confidence in YUM's China business following a recent trip to the country. Management is hosting the earnings call this morning.

MCD Japan SSS gained 4.8% in September. This is the first time in three months that the monthly comp number has been positive. The company attributed the gain to a change in lifestyle patterns after the lifting of the government-mandated electricity saving request on September 9th.

Howard Penney

Managing Director

Rory Green

Analyst