Position in Europe: Short Italy (EWI)

Into the close of yesterday’s session Keith shorted Italy via the etf EWI in the Hedgeye Virtual Portfolio. Italy is a country we’ve come back to numerous times on the short side over the last eighteen months. This time around we got a bounce in the etf to opportunistically trade the security over the immediate term TRADE; however over the intermediate term TREND the country will be hostage to its bond auctions, ECB bond purchasing support, and political instability within the larger context of the country’s and Europe’s sovereign debt and bank contagion crisis.

The country’s outsized debt of 120% of GDP remains a persistent worry, yet pressing is that nearly one-third of its €226 Billion planned bond issuance for 2011 is outstanding. This compares to remaining bond issuance in Germany at 23%, France 17%, Belgium 4%, and Finland 4%, for example, according to Bloomberg.

With the Standard & Poor’s downgrading Italy’s credit rating one notch to A with a negative outlook on 9/19, S&P’s first downgrade of Italy since 2006, demand of Italian government paper, including the yield it will be priced at, will be increasingly dependent on buying from the ECB under its Securities Market Program [SMP] in the weeks ahead.

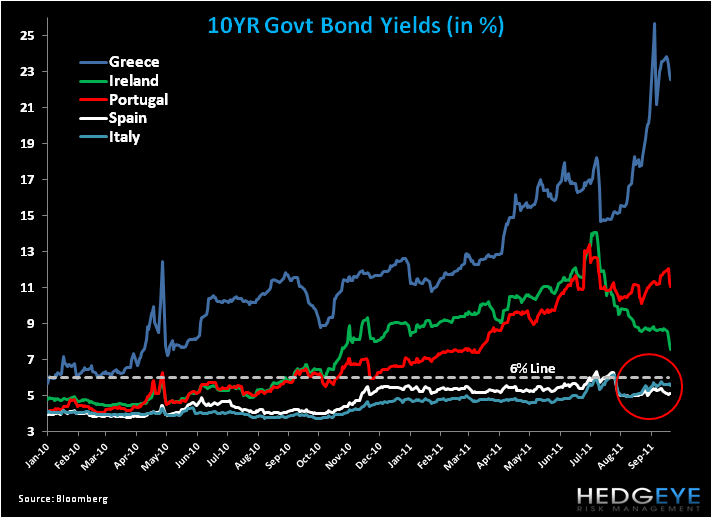

We’ve noted in previous work that the 6% yield on 10 year government bonds has been a historically significant level for the PIIGS, meaning that a violation of the line to the upside resulted in an expeditious upward run (see chart below). Italy, like Spain, has maintained a level below 6% since the ECB restarted the SMP on August 8th, and currently trades at 5.55%. Last week the SMP bought a total of €3.95 Billion of secondary bonds across the Eurozone (without stating which countries specifically), the smallest amount since the program’s restart that saw €22 Billion in purchases in the first week.

Investment and political risk remain hot topics in Italy. Investors are still questioning the extent to which Italy’s €54.5 Billion austerity package, which was heavily watered down when it was finally approved last month, will cut enough fat to move the dial on its debt and deficit figures. Much of this indecision is enhanced by the lack of credibility in leadership at the top. And if Berlusconi’s previous scandals weren’t enough to tarnish his reputation, allegedly he has a personal feud with his Economy Minister Guilio Tremonti, perhaps the one man that the market is turning to for a credible answer to the country’s fiscal state.

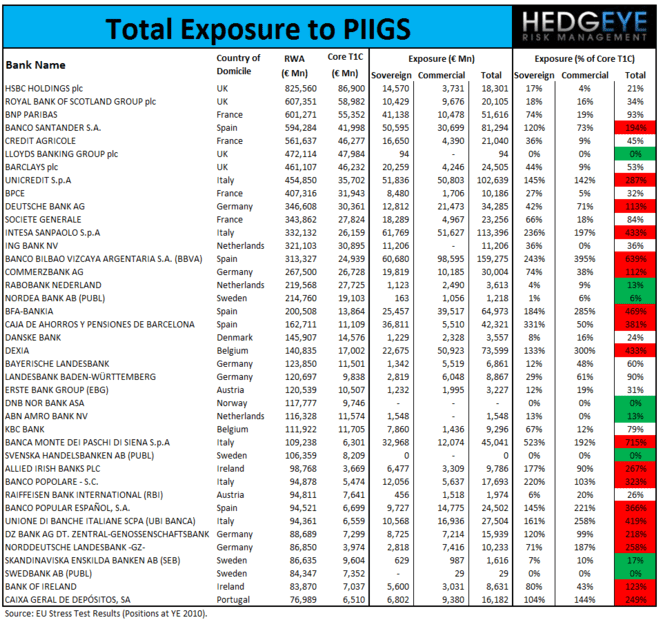

With the help of our financials team we’ve been able to quantify the exposures of European banks to the PIIGS. As the chart below demonstrates, 4 of the 5 listed Italian banks have over 300% of their Core Tier 1 Capital in PIIGS sovereign debt or commercial loans, with the remaining bank at 287%! While this data is stale, as of the 2010 Stress Test results, it nevertheless paints an ugly picture.

Italy extended its short-selling ban on Wednesday until November 11th. The Italian etf EWI is composed of 28.4% Financials, followed by 28.0% Energy, and 21.0% Utilities.

Italy FTSE MIB is down -27% quarter-to-date and over the same period 5YR Italian CDS has risen 300bps to 477bps. As the chart below shows, we don’t see downside support until 12,800, or roughly -13.5% from here.

Matthew Hedrick

Senior Analyst