THE HEDGEYE BREAKFAST MENU

Notable MACRO data points, news items, and price action pertaining to the restaurant space.

MACRO NOTES

As I posted yesterday for the MACRO team my thesis on the consumer is consistent with a fundamentally-weak economy: no job growth, declining real income, Bernanke-inspired price volatility, declining stock prices, falling house prices, sticky gasoline prices, and zero confidence.

Overall, the MACRO data out yesterday on consumer trends is consistent with the factors listed above. Yet, there are silver linings! Well, maybe…

Yesterday, the high frequency – ICSC chain store sales index – confirms the decelerating thesis, as the index fell 0.2% last week. This is consistent with the painfully slow downward trend (the index is now down 6 of the last 8 weeks.) On a year-over-year basis, growth dipped to 2.7%, the slowest pace in three weeks, though consistent with the trends of 1H11. Is there a silver lining here?

Also bouncing along the bottom is the Richmond Fed survey, which contracted for the third consecutive month in September. The pace of decline moderated from August, as the composite index rose 4 points to -6. Looking at the details, new and unfilled orders remained on downward trends but employment growth accelerated and input cost pressures eased. The increase in employment month-over-month is the first silver lining in the overall sluggish environment

Lastly, after plunging 14 points in August, the Conference Board Confidence Index was virtually unchanged in September (rising only 0.2). Last month saw a slight 0.7-point upward revision to the August print. The improvement was led by better employment expectations, which is the second silver lining.

If the economy were to accelerate confidence should recover, but given the excessive debt burden domestically and in Europe, it’s unlikely that growth is going to accelerate. Our 3Q GDP estimate is 1.1 to 1.4% year-over-year; the risk to the downside is that the low confidence results stay on a continued downward trajectory in sales trends, and causes further economic weakness.

The third silver lining is not one from today’s data, but one that economists often cite as a reason to buy equities here: that corporate America is flush with cash. That cash waiting in the wings coupled with pent-up demand could lead to a quick improvement in the jobs picture and an acceleration of growth.

Hope springs eternal, but is not an investment process!

SUB-SECTOR PERFORMANCE

Deflating the Inflation - is great for the Food Processing sector and not so good for food retail.

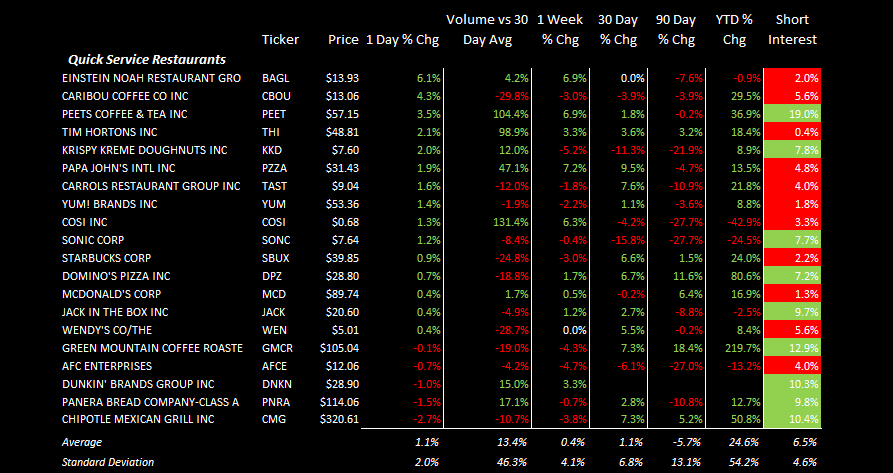

QUICK SERVICE

PNRA & DNKN were notable decliners on positive volume studies

Domino’s Pizza downgraded to hold from buy at Peel Hunt

Domino's Pizza UL & IRL interim management statement: says on track and confident that it'll finish the year in line with market expectations - For 2Q11 - SSS up +3.9%(605 stores) vs year-ago +9.9% (553 stores); UK only SSS+ 4.1% vs year-ago +11.5%; Republic of Ireland SSS in Euros fell (4.4%) vs year-ago (0.5%); E-commerce accounted for 46.6% of UK delivered sales vs year-ago 39.7% and Total online sales up +36.4% to £45.0M vs year-ago £33.0M

CMG initiated outperform with $400 target - Wedbush

PNRA initiated neutral with $116 target - Wedbush

COSI holder Blum Growth Fund calls for new board of directors and has also offered to serve as Chairman and CEO for a salary of $1 for the first year. Also, stated that would be attempting to influence the future of the company through changes to the board and management.

SONC - initiated equal-weight at Stephens

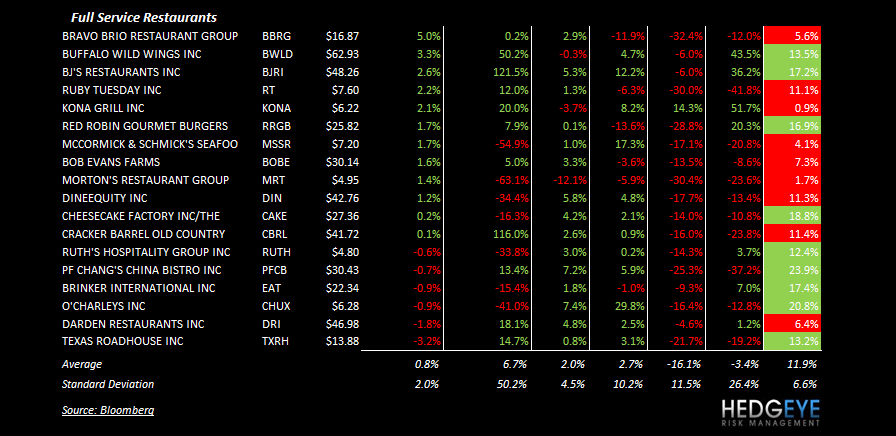

FULL SERVICE

BWLD - had a strong day yesterday on positive studies - initiated outperform with $82 target - Wedbush

BJRI had a strong day yesterday on positive studies - initiated neutral with $45 target - Wedbush

DRI & TXRH were notable decliners on positive volume studies. TXRH remains a favorite on the short side.

Howard Penney

Managing Director