TODAY’S S&P 500 SET-UP - September 13, 2011

As we look at today’s set up for the S&P 500, the range is 33 points or -1.83% downside to 1141 and 1.01% upside to 1174.

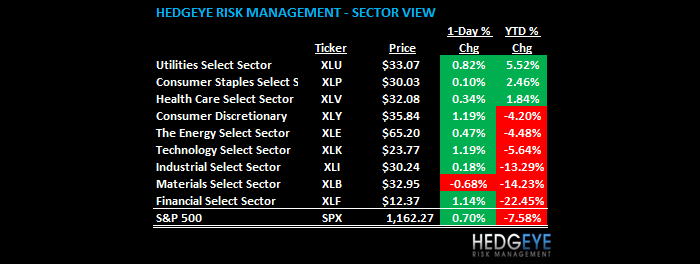

SECTOR AND GLOBAL PERFORMANCE

On our intermediate-term TREND duration, 8 of 9 Sectors remain broken/bearish. TREND trumps TRADE. The only sector of 9 that’s bullish TRADE and TREND = Utilities (XLU). We’re long Utilities and Healthcare (XLV) which is 1 of 3 Sectors that is bullish on our immediate-term TRADE duration (Consumer Staples, XLP, is the 3rd).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -219 (+1907)

- VOLUME: NYSE 1087.88 (-10.98%)

- VIX: 38.52 +12.14% YTD PERFORMANCE: +117.01%

- SPX PUT/CALL RATIO: 2.20 from 1.80 +22.48%

CREDIT/ECONOMIC MARKET LOOK:

FIXED INCOME: 10yr UST yields held the 1.86% support line yesterday; bouncing big this morning

- TED SPREAD: 33.78

- 3-MONTH T-BILL YIELD: 0.01%

- 10-Year: 1.94 from 1.93

- YIELD CURVE: 1.73 from 1.76

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30 a.m.: NFIB Aug. small business optimism

- 8:30 a.m.: Aug. import price index, est. M/m (-0.8%), prior (0.3%)

- 10 a.m.: IBD/TIPP Sept. economic optimism, est. 38.0, prior 35.8

- 11:30 a.m.: U.S. to sell $27b 4-week bills

- 1 p.m.: U.S. to sell $13b 30-year bonds reopening

- 2 p.m.: Aug. budget statement, est. (-$132.0b)

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- World oil demand forecast cut by IEA on concerns about health of global economy

- Merkel rejects Greek default, defends euro-area integrity

- President Obama gives jobs speech in Columbus, Ohio, 2:15 p.m.

COMMODITY/GROWTH EXPECTATION

OIL – alongside Copper and 10yr UST yields arresting their declines this morning, WTIC oil holding an important TRADE line of support ($86.03) is an important growth stabilizer in Global Macro this morning. This tells me we aren’t going to the dark ages of depression, yet. Global Macro remains as interconnected across asset classes as ever

MOST POPULAR COMMODITY HEADLINES FROM BLOOMBERG:

- Thailand May Cede No. 1 Rice Ranking to Raise Rural Incomes

- Gold May Fall a Third Day on Sales to Cover Losses in Equities

- Oil Gains a Second Day on Signs U.S. Crude Stockpiles May Drop

- Australia Seen Shipping Record Wheat Cargoes on Bumper Harvest

- China Builds Lead in Afghan Commodities, Adds Oil to Copper

- Steel Dynamics Cuts Forecast as Flat-Rolled Margins Get Squeezed

- Copper Climbs First Day in Three on Easing European Debt Concern

- Corn Falls as U.S. Cuts Demand Outlook, Crop Conditions Improve

- Wheat to Stay Near Parity With Corn as Soy Climbs, Goldman Says

- Oil Trades Near Four-Day Low as IEA Reduces Demand Estimates

CURRENCIES

EUROPEAN MARKETS

- GERMANY – with the DAX having moved into full crash/capitulation mode in the last 3 days of trading, it shouldn’t surprise anyone to see German stocks move 2% in 20 minutes to go green on the day. With political career risk dominating the craws of every Eurocrat, expect plenty more rumors than the “China buys Italy” thing we saw yesterday. Most of the rumors are lies, but deal with them.

ASIAN MARKETS

- ASIA: mixed on light volume as volatility in Asian Equities is calming (bullish); Australia/Japan/Malaysia = up; China/Thai/Singapore down

MIDDLE EAST

Howard Penney

Managing Director