|

Short: MPW, EWCZ, ULTA, ALGN, RBRK, PDCO, VRT, HST, ELF, CAR, ALAB, EYE Long: NEM, DGX, PM, ULS, PSA, CPT, AVB, IRT, T, VTR, AMH, TKO, TTD, ADBE, CLX |

This week we added Clorox (CLX) to the Long side and removed Xylem (XYL) and Rentokil (RTO) from the Long side and G-III Apparel Group (GIII) from the Short side. We added Shorts Avis Budget Group (CAR), Astera Labs (ALAB) and National Vision Holdings (EYE).

See below for updates on our 27 current high-conviction Long and Short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

NEM

Sector: Industrials

Sector Head: Jay Van Sciver

|

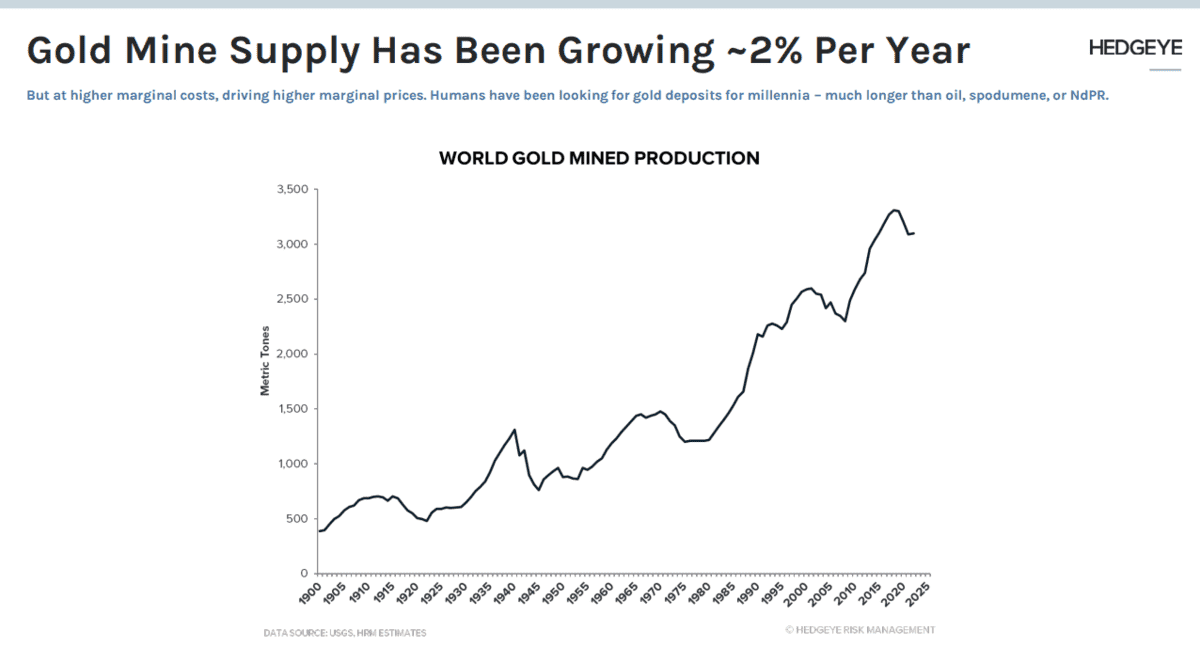

THESIS SUMMARY: Newmont has historically outperformed during Quad 4 macroeconomic conditions, characterized by decelerating growth and disinflationary pressures. Read full stock report, "Newmont Corporation (NEM): A Sure Way To Underperform Gold Long Term, But Short-Term Upside" |

WEEKEND UPDATE: Newmont Corporation (NEM) - The company recently announced plans to divest some of its non-core assets, including the Telfer gold mine and its 70% stake in the Havieron project in Australia. The deal with Greatland Gold is valued at up to $475 million and is expected to close in Q4 2024. This is part of Newmont's strategy to raise $2 billion by selling smaller mines, allowing the company to focus on its core assets and reduce debt while returning capital to shareholders.

DGX

Sector: Health Care

Sector Head: Tom Tobin

WEEKEND UPDATE: Quest Diagnostics (DGX) – The company announced a strategic collaboration with Sentara Health Plans on September 18, 2024. This multi-year agreement will make Quest the exclusive independent lab provider for Sentara Health Plan members in Virginia and Florida, starting January 2025. The collaboration will expand Quest's service network in these regions and help reduce healthcare costs by redirecting lab services to Quest.

PM

Sector: Consumer Staples

Sector Head: Daniel Biolsi

|

THESIS SUMMARY: Philip Morris International embodies a transformative investment opportunity within the tobacco industry. Its strategic pivot towards smoke-free products, combined with a compelling financial profile and growth prospects shows potential in the stock price. Read full stock report, "Philip Morris International (PM): Smoking the Competition in Alternative Nicotine" |

WEEKEND UPDATE: Philip Morris International (PM) - This week, Biolsi wrote an Early Look on PM and its transition into smokeless nicotine. CLICK HERE to view the article.

ULS

Sector: Industrials

Sector Head: Jay Van Sciver

WEEKEND UPDATE: UL Solutions (ULS) - The company announced the pricing of a public offering of 20,000,000 shares of Class A common stock at $49.00 per share, consisting entirely of secondary shares sold by UL Standards & Engagement. The underwriters, led by Goldman Sachs & Co. LLC and J.P. Morgan, have a 30-day option to purchase up to an additional 3,000,000 shares from the selling stockholder. UL Solutions will not receive any proceeds from the sale. The offering, expected to close on September 9, 2024, is subject to customary closing conditions. Copies of the prospectus can be obtained from the lead underwriters.

The company continues to strengthen its position as a global leader in applied safety science, offering a wide range of services including regulatory compliance, sustainability, and risk management solutions. Stay long.

PSA

Sector: Real Estate Investment Trusts (REITs)

Sector Head: Rob Simone

|

THESIS SUMMARY: PSA maintains by far the most conservatively levered balance sheet, proving it with the greatest ability among storage REITS to supplement internal “same store” growth with accretive “external” growth via acquisitions and developments. Read full PSA Stock Report, "Public Storage (PSA): Safest In Self-Storage" |

WEEKEND UPDATE: Public Storage (PSA) - The company recently hit a new 52-week high, trading at $361.64 on September 16, 2024, following an analyst upgrade from Evercore ISI, which raised the stock's price target from $334 to $343. This follows a strong performance in recent months, with the company benefiting from its solid position as a leader in the self-storage industry.

In its latest earnings report (July 30, 2024), Public Storage reported earnings of $2.66 per share, missing the consensus estimate of $4.20. However, the company remains financially robust with a return on equity of 36.55% and a net margin of 44.88%. Public Storage also continues to offer a substantial dividend, with shareholders set to receive $3.00 per share on September 30, 2024, yielding around 3.31% annually.

CPT

Sector: Real Estate Investment Trusts (REITs)

Sector Head: Rob Simone

|

THESIS SUMMARY: This company's strong market position, operational efficiency, strategic development projects, and financial performance position it for significant growth over the next 6 months to 3 years. Read full stock report, "Camden Property Trust (CPT): High-Growth Market Operator" |

WEEKEND UPDATE: Camden Property Trust (CPT) - The company recently hit a new 52-week high, reaching $127.38 on September 19, 2024. This marks a strong performance driven by several positive analyst ratings. On the financial side, Camden Property Trust reported revenue of $387.15 million in its most recent earnings release, slightly exceeding analyst expectations. However, the company missed earnings per share (EPS) estimates, reporting $0.40 per share, compared to the expected $1.67. Camden also declared a quarterly dividend of $1.03 per share, which will be paid on October 17, 2024, yielding around 3.25% annually

AVB

Sector: Real Estate Investment Trusts (REITs)

Sector Head: Rob Simone

|

THESIS SUMMARY: Read full stock report, "AvalonBay Communities (AVB): A Core Long" |

WEEKEND UPDATE: AvalonBay Communities (AVB) - The stock recently hit a 52-week high of $236.26 recently, driven by strong demand in the real estate market. The company reported mixed results for Q2 2024, with earnings per share (EPS) of $1.78, missing analyst expectations of $2.71. However, revenue came in at $726.04 million, surpassing estimates. AvalonBay continues to develop its portfolio, with 299 apartment communities and 18 more under development, focusing on major metropolitan markets across the U.S. AvalonBay also recently announced a public offering of 3.2 million shares of common stock, which is expected to close soon, and provided an update on its third-quarter 2024 operating performance

IRT

Sector: Real Estate Investment Trusts (REITs)

Sector Head: Rob Simone

|

THESIS SUMMARY: IRT’s focus on value-add renovations, disciplined capital allocation, and presence in high-growth markets underpin its performance and growth prospects. Read full stock report, "Independence Realty Trust (IRT): Best Capital Allocator" |

WEEKEND UPDATE: Independence Realty Trust (IRT) - The multifamily apartment REIT, has been making notable strides recently. On September 19, 2024, the stock reached a new 52-week high, trading at $21.20. Analysts have been optimistic about its performance, with price targets ranging from $20 to $22, and several analysts issuing "buy" ratings. The company also recently declared a quarterly dividend of $0.16 per share, to be paid on October 18, 2024. This continues IRT's consistent dividend policy, yielding about 3.03% annually.

T

Sector: Communications

Sector Head: Andrew Freedman

|

THESIS SUMMARY: New dynamics around Fixed Wireless, Fiber Optic Internet, and the end of the Affordable Connectivity Program have caused concerns for traditional cable companies, but AT&T’s consistent results and diverse range of products positions them well to capitalize on emerging trends. The TAIL duration (3 years or less) outlook looks strong. Read full stock report, "AT&T (T): Telecom Giant" |

WEEKEND UPDATE: AT&T (T) - AT&T recently provided an update at the Goldman Sachs Communacopia + Technology Conference. CEO John Stankey highlighted the company's continued progress in expanding its 5G and fiber networks, with fiber penetration rates exceeding expectations. AT&T remains on track to meet its 2024 financial guidance and expects capital investments in the $21-22 billion range. The company is also focused on cost savings, targeting over $2 billion in run-rate reductions by mid-2026.

VTR

Sector: Real Estate Investment Trusts (REITs)

Sector Head: Rob Simone

|

THESIS SUMMARY: Ventas, Inc. stands out in the REIT sector, driven by its strategic focus on senior housing, favorable Return on Capital (RoC) profile, and effective capital deployment. Read full stock report, "Ventas Inc. (VTR): Earnings Growth 'Flywheel'" |

WEEKEND UPDATE: Ventas Inc. (VTR) - The company recently declared a quarterly dividend of $0.45 per share, payable on October 17, 2024. The company has experienced strong stock performance, with shares rising by 26% over the past three months, and its stock trading close to its 52-week high at around $64. Ventas continues to focus on its senior housing and healthcare properties. Stay long VTR.

AMH

Sector: Real Estate Investment Trusts (REITs)

Sector Head: Rob Simone

WEEKEND UPDATE: American Homes 4 Rent (AMH) - The company has seen recent positive performance, with its stock trading close to its 52-week high of $41.41. Currently, the stock is priced around $39.49, with a market cap of $14.53 billion. Over the past three months, the stock has gained approximately 10.63%, reflecting strong demand for single-family rental properties amid favorable market conditions. In its latest earnings report for Q2 2024, AMH posted revenues of $423.5 million, a 7.1% increase year-over-year. However, earnings per share (EPS) came in at $0.25, missing analyst expectations of $0.43. Despite the earnings miss, the company's net margin stood at a healthy 21.83%, and it continues to show robust profitability metrics.

TKO

Sector: Communications

Sector Head: Andrew Freedman

|

THESIS SUMMARY: TKO is well-positioned for long-term growth through its dominant brands in UFC and WWE, bolstered by strategic deals and strong margins, but faces risks from competition, regulatory challenges, and potential streaming disruptions. Read full stock report, "TKO Group Holdings (TKO): Fighting for the Sports Entertainment Belt" |

WEEKEND UPDATE: TKO Holdings (TKO) - UFC 306 at the Sphere in Las Vegas set a new record for the mixed-martial-arts organization, generating $22 million in ticket sales and breaking the previous record of $17.7 million from UFC 205 in 2016. The event, part of Riyadh Season Noche UFC, also set new records for merchandise sales and for the largest single-day gate at the Sphere, which is owned by Sphere Entertainment Co. CEO James Dolan. This marked the first live sporting event at the $2.3 billion venue, leveraging its 160,000-square-foot interior screen for a groundbreaking fan experience.

TTD

Sector: Communications

Sector Head: Andrew Freedman

|

THESIS SUMMARY: The Trade Desk shows upside over a TAIL (3 years or less) duration, driven by its strategic initiatives in retail media along with its strong market position. Read full stock report, "The Trade Desk (TTD): Benefiting from Network Effect Expansion" |

WEEKEND UPDATE: The Trade Desk (TTD) - The company reported a strong Q2 2024, surpassing analyst expectations with revenue of $584.5 million and earnings per share (EPS) of $0.39. Growth was driven by expanding digital advertising, particularly in connected TV (CTV), which now accounts for nearly half of the company’s revenue. The Trade Desk continues to strengthen its market position with new partnerships and the adoption of Unified ID 2.0 (UID2) to enhance ad targeting and privacy. Recent integrations with Roku and Pandora showcase its growing presence in digital advertising. The CEO also clarified that while the company is developing its own streaming TV operating system, it is not directly competing with Roku or Amazon

ADBE

Sector: Software

Sector Heads: Andrew Freedman, Felix Wang

|

THESIS SUMMARY: Adobe remains the undisputed leader in the creative software market. We are confident AI will not be a headwind for Adobe. Read full stock report, "Adobe Inc. (ADBE): Undisputed Creative Leader" |

WEEKEND UPDATE: Adobe (ADBE) - In Q3 2024 the company reported record revenue of $5.41 billion, exceeding analyst expectations. Its earnings per share (EPS) came in at $4.65, beating forecasts of $4.53. This strong performance was driven by continued growth in its digital media business and innovation across its product suite. Adobe's stock has experienced some volatility. After reaching a recent high of $527.48, the stock has fluctuated, reflecting market concerns over its guidance for the remainder of the fiscal year, which fell short of expectations. The stock is currently trading 17.5% below its 52-week high. We believe they will meet our Q4 expectations on digital media, which are above Street estimates. Stay long.

CLX

Sector: Consumer Staples

Sector Head: Daniel Biolsi

|

THESIS SUMMARY: Clorox represents a compelling investment opportunity for those looking to capitalize on the company's strong market position, brand strength, and favorable market trends. Read full stock report, "Clorox (CLX): Post-Pandemic Hangover Is Cured" |

WEEKEND UPDATE: Clorox (CLX) - Clorox’s last earnings report was well above consensus, driven by margin performance. Investors were looking for visibility in Clorox’s margins, and they got it. The company faces difficult base effects in FQ4, but the margin upside potential can be reinvested to drive growth. Quad 4 and Clorox’s style factors are in alignment with our outlook for the company’s sales and margins.

MPW

Sector: Real Estate Investment Trusts (REITs)

Sector Head: Rob Simone

|

THESIS SUMMARY: The company is not a traditional triple-net REIT, rather an investor in hospital systems ("WholeCos" using the company's own words). In the process MPW removes the arbitrage from a traditional PorpCo-OpCo arbitrage. These investments are structured as loans + equity investments to the operator tenants, which are in many cases distressed and owe significant rent payments back to MPW as landlord. The arrangement is circular and depends on MPW's ability to raise attractively-priced external capital. The equity is very possibly completely worthless, as we think the assets are worth no more than ~$6.5 billion (updated) to true "arm's length" third-party buyers vs. pro forma net debt of ~$10.5 billion at share. Read full stock report, "Medical Properties Trust (MPW): A Dumpster Fire Burning on Fumes" |

WEEKEND UPDATE: Medical Properties Trust (MPW) - Following a Senate HELP committee hearing recently, concerns over Medical Properties Trust (MPW) were highlighted, particularly regarding its dealings with Steward Health. Key issues include admissions that MPW’s leases were “above market” and “unaffordable,” with capital investments not used for hospital improvements but instead to sustain recorded “rent” payments. MPW's recent "global settlement" suggests no cash flow for 18 months, and it appears aimed at avoiding real estate impairments and litigation. MPW faces significant impairments, potential funding gaps, and questions about liquidity, with its business model criticized for unsustainable practices and misaligned incentives focused on non-cash metrics. The company’s strategy risks repeating past mistakes by lending to undercapitalized operators to artificially maintain rent and earnings figures, pushing it into deeper financial instability.

EWCZ

Sector: Retail

Sector Head: Brian McGough

|

THESIS SUMMARY: We are Short European Wax Center (EWCZ) due to future negative comparable store sales (comps), an uncertain pricing strategy, high franchise costs, and an increasingly leveraged financial structure. Read full stock report, "European Wax Center (EWCZ): A Profitable Opportunity From a "Failed IPO." |

WEEKEND UPDATE: European Wax Center (EWCZ) - The company announced this week that it has taken various actions to focus on driving growth and profitability. It has partnered with Dolabra Digital, a data-driven strategy leader, to help with guest engagement and acquisition and retention in order to drive growth and efficency. Its realigning it’s Commercial and Field Operations teams, and it’s pausing its laser hair removal pilot outside of New York for the meantime. In the update the company reaffirmed the guidance given in August. While these are all great steps and goals, we think the company is still going to face demand pressure over the upcoming few quarters while it sorts its issues out, and in that meantime the stock is likely to trade lower toward its lows of sub-$5.

ULTA

Sector: Retail

Sector Head: Brian McGough

|

THESIS SUMMARY: Ulta Beauty is facing a multifaceted challenge as it contends with shifting consumer preferences, increased competition from Kohl’s Sephora, and potential market saturation. Read full stock report, "Ulta Beauty (ULTA): Headwinds and Slowing Trends" |

WEEKEND UPDATE: Ulta Beauty (ULTA) - Trends aren’t looking great for Ulta as the credit card data is steadily negative for the quarter. Last Q we saw negative comps for the first time in nearly 10 years, and the company tempered guidnace for the back half of the year. Even with the tempered guidance, the trends look incrementally bearish. This company is likely to put up negative comps in the upcoming quarters as the demand in beauty slows and the consumer continues to be under pressure. With revenues rolling, we think expectations here are likely to come down and this stock should trade down to around $300.

ALGN

Sector: Health Care

Sector Head: Tom Tobin

|

THESIS SUMMARY: Align Technology faces a challenging outlook heading into the second half of 2024. The combination of macroeconomic headwinds, high out-of-pocket expenses, rising financing costs, and competitive pressures creates a bearish scenario for the stock. Read full stock report, "Align Technology (ALGN): Macro and Market Headwinds" |

WEEKEND UPDATE: Align Technology (ALGN) - The company has faced significant challenges recently, with its stock down 6.32% in September and trading 25% below its 52-week high. Despite beating earnings expectations in Q2 2024 with EPS of $2.41, the company is struggling to maintain momentum. Year-over-year revenue growth was a modest 2.6%, signaling slowing demand in key market. Some analyst downgrades are reflecting concerns over the company’s high valuation—its price-to-earnings (P/E) ratio is currently 42.34, which may be hard to justify given the limited growth. Additionally, Align's reliance on discretionary dental care products like Invisalign could face headwinds as economic uncertainties and inflation impact consumer spending. Stay Short this name.

RBRK

Sector: Software

Sector Heads: Andrew Freedman, Felix Wang

|

THESIS SUMMARY: Rubrik faces growing challenges as competition intensifies, particularly with the Cohesity-Veritas alliance backed by Big Tech and NVDA, which threatens Rubrik's market share in key areas like cyber resilience. Read full stock report, "Rubrik (RBRK): The Best Times are Behind" |

WEEKEND UPDATE: Rubrik Inc. (RBRK) - The company has been facing significant challenges recently, with its stock performance showing considerable volatility. The stock is down 21% from its 52-week high, trading at around $31.54. Over the past month, it has experienced a sharp decline, falling 12% in just 30 trading days. This volatility is compounded by a weak financial position, with Rubrik’s operating margin at -142% and a profit margin at -149%, indicating that the company is struggling to convert sales into profitability. Stay Short RBRK.

PDCO

Sector: Health Care

Sector Head: Tom Tobin

WEEKEND UPDATE: Patterson Companies (PDCO) - The company is facing some notable headwinds. Recently, the company’s stock has seen a steady decline, dropping over 13% in the past three months and trading 36% below its 52-week high. In its latest earnings report for Q1 FY2025, the company missed expectations, reporting earnings per share (EPS) of $0.24, falling short of the consensus estimate of $0.32. Revenue also declined by 2.3% compared to the same period last year, indicating a weakening performance. Despite its current market capitalization of $1.92 billion, Patterson’s profitability metrics, including a slim profit margin of 2.58%, suggest operational challenges. Moreover, the stock’s poor performance relative to its moving averages signals potential bearish sentiment, with the stock now trading well below its 20-, 50-, and 200-day averages.

VRT

Sector: Global Tech

Sector Head: Felix Wang

WEEKEND UPDATE: Vertiv Holdings (VTR) - We remain bearish on Tech and VRT in Quad 4. We believe the name is over owned, the Bulls are trapped, and Felix Wang is the only legit bear on the name. The company's recent earnings didn't impress on the growth side. Demand expectations disappointed big time. Q2 revenues was only in-line with estimates; Q3 guidance (midpoint OF $1.96bn) below Bloomberg and buyside expectations but in-line with our estimate ($1.958bn). The bulls will point to Q2 order growth of 57% (HE: 30%) but it's less clear of a metric than revenues. However, Q3 orders growth guidance was only 10%-15%; we were modeling 15% for Q3. With harder comps on the way, order growth will continue to decelerate in a big way in 2H 2024.

HST

Sector: Gaming, Lodging, and Leisure

Sector Head: Sean Jenkins

WEEKEND UPDATE: Host Hotels & Resorts (HST) - Hotel REITs like Host Hotels & Resorts (HST) are facing significant challenges, with demand slowing across both leisure and non-leisure segments. Despite attempts by the sell-side to call a bottom, we don’t see one yet. The outlook into Q4 and Q1 2025 remains unfavorable, as comps are tougher than expected, and any near-term relief is likely temporary. Leisure travel isn’t offering a meaningful catalyst, and the ongoing shift toward alternative accommodations continues to pressure RevPAR growth. The bull case relies on a sharp reversal of these headwinds, which seems unlikely. We remain underweight and short on HST as further RevPAR deceleration appears likely.

ELF

Sector: Retail

Sector Head: Brian McGough

WEEKEND UPDATE: elf Beauty (ELF) - After a multiple week drop post-earnings print, ELF has more recently remained steady in the mid-$110s. The company is slowing from +70% growth to high-teens organic growth, coupled with margin risk. As revenues slow and margins weaker at a rate faster than the Street is expecting on this expensive stock, there is big valuation risk given its ~20x EBITDA multiple. We still see downside from here to sub-$100 and wouldn’t be long this until its closer to $75.

CAR

Sector: Industrials

Sector Head: Jay Van Sciver

WEEKEND UPDATE: Avis Budget Group (CAR) - The company has faced some significant challenges recently, signaling a bearish outlook. Despite reporting over $3 billion in revenue for Q2 2024, the company missed earnings expectations by a wide margin, posting earnings per share (EPS) of $0.41, far below the consensus estimate of $2.60. This marked a 2.4% decline in revenue compared to the same period last year. The stock has also struggled, plummeting nearly 25% over the last three months and trading 61% below its 52-week high. Go Short CAR.

ALAB

Sector: Global Tech

Sector Head: Felix Wang

WEEKEND UPDATE: Astera Labs (ALAB) - Astera Labs remains a compelling short opportunity, with the stock already down 40% since our initial call. Despite management’s optimistic narrative, the company faces several headwinds, including limited retimer demand in future Nvidia products, increasing competition from PCIe 6 and Gen6 retimers, and declining AI-related stock valuations. ALAB’s inflated valuation, deteriorating financial performance, and lack of significant profitability improvements further support the bearish outlook.

EYE

Sector: Health Care

Sector Head: Tom Tobin

WEEKEND UPDATE: National Vision Holdings (EYE) - has seen its stock drop to a 12-month low of $9.68 as of late September 2024, plummeting by over 58% in the past six months and 33% in the last three months, with the stock significantly underperforming its 200-day moving average. Despite beating EPS expectations in Q2 2024, the company missed revenue targets by 1.7%, signaling declining sales growth. Additionally, National Vision lowered its 2024 revenue guidance to $1.8 billion, below analysts' forecasts of $1.9 billion, with slim operating margins and a negative profit margin of -4%, pointing to deeper financial inefficiencies. Stay Short EYE.