Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.

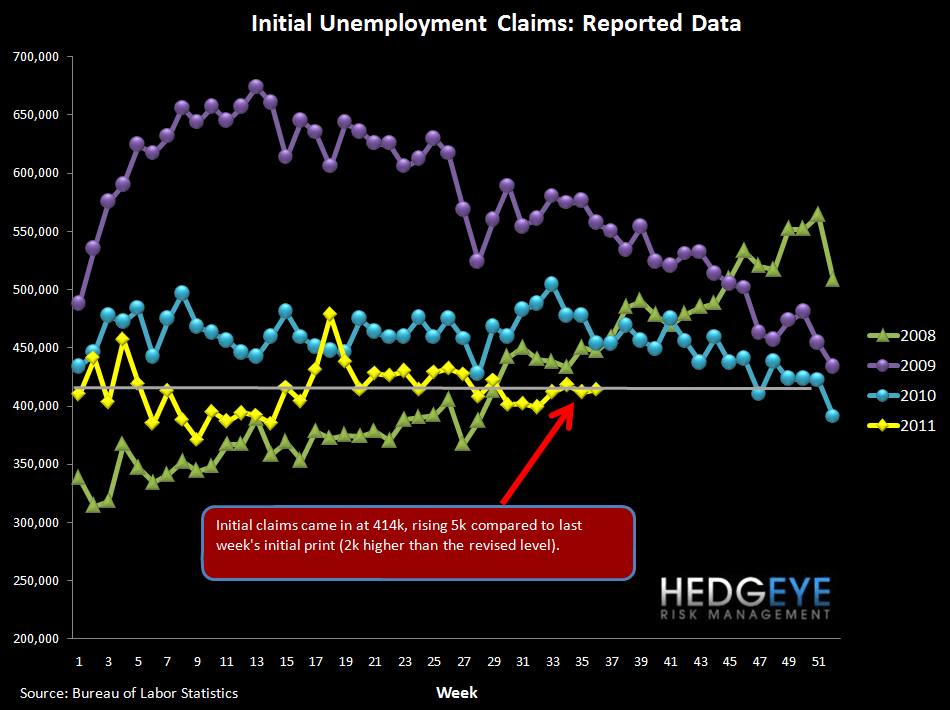

Initial Claims Rise 5k

Initial jobless claims rose 5k to 414k last week (+2k after the revision to last week's data). With this week's data point, there is now a clear upward trend in place in rolling claims. The Labor Department noted that there was little effect on claims from the hurricane. However, because of the Labor Day holiday, data from several states including California was estimated rather than actual. This means that revisions next week are likely to be larger than normal, although the revision could go either direction.

10-year Declines Put Enormous Pressure on Margins

We presented our Black Book yesterday that analyzes the impact of the current rate environment on NIM. To summarize, the impact is profound, wiping out substantial swaths of interest income at all the moneycenter banks. (Contact us if you haven't seen this presentation.) This week's price action in the 10-yr remained negative for the banks.

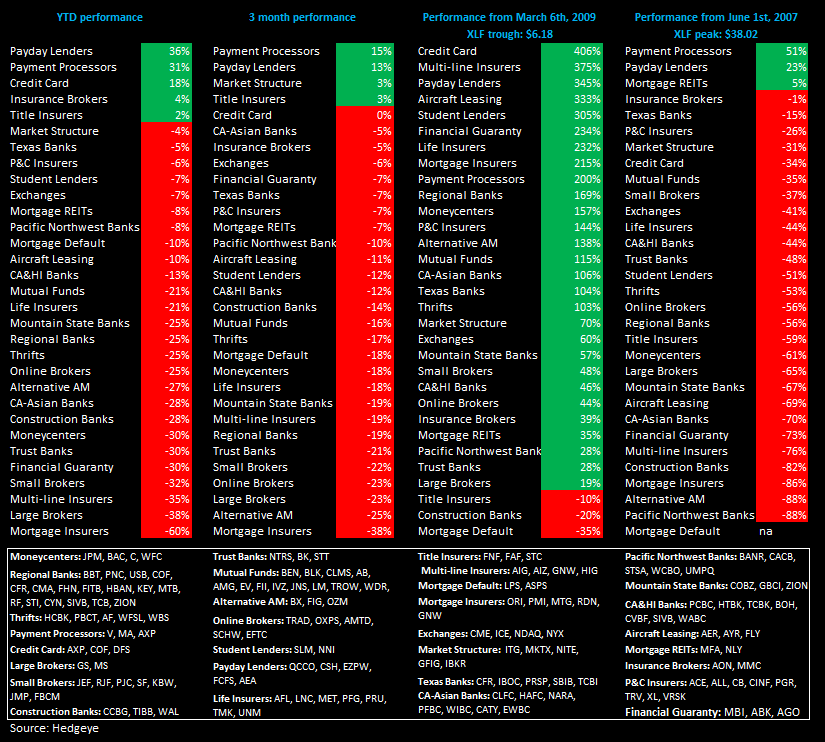

Subsector Performance Chart

The chart below shows the performance of financial stocks by subsector.

Joshua Steiner, CFA

Allison Kaptur

Having trouble viewing the charts in this email? Please click the link below to view in your browser.