This note was originally published at 8am on September 02, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Old age is a shipwreck.”

-Charles de Gaulle

In life, there are certain inevitabilities, with aging at the top of the list. No amount of money, fame, or religion prevents the reality that we will all grow old, at least physically, one day. While in his quote above de Gaulle could easily have been talking about the fiscal discipline of Greece, he was, in fact, appropriately describing the reality of our bodies naturally aging and eventually deteriorating.

Now that I’ve started your morning off on a completely somber note, I’ll offer another reality, which is that aging and longevity research suggests that all of our life spans will be extended versus prior generations. Not only that, we will age more gracefully and comfortably as well. In her new book, “100+ : How The Coming Age of Longevity Will Change Everything, From Careers And Relationships To Family and Faith”, Sonia Arrison, a fellow Canadian and senior researcher at the Pacific Research Institute, provides an insightful overview of the technology of longevity.

In fact, as Arrison notes, human life has generally been extending since human life began. During the Cro-Magnon era, humans could have expected to live just long enough to graduate from high school, or to the ripe old age of eighteen. By the time of the European Renaissance life expectancy had almost doubled to thirty. By 1850, just as the U.S. population hit 23.1 million, the average age reached forty-three. Today, with the acceleration of medical breakthroughs, the average person in the Western world can expect to celebrate his, or her, eightieth birthday. In the future, according to Arrison:

“The first person to live to 150 years has probably already been born.”

The pursuit of longevity has been ongoing since the beginning of recorded history. One of the first contemplations of death actually occurs in Genesis, the first book of the bible. After willfully disobeying God by eating the forbidden from the Tree of Knowledge of good and evil, Adam and Eve were kicked out of the Garden of Eden, a place of immortality, into the real world where they faced sickness, death, and the threat of crazy New York taxi cab drivers.

I don’t need to restate the entire history of human aging to assure you that it is a topic that has been and likely always will be front and center for mankind. As a result, a vibrant growth industry has risen around areas of extending lives and more gracefully aging. In her book, Arrison discuss some of the key areas of development and investment, which we’ve borrowed and outlined in the table below:

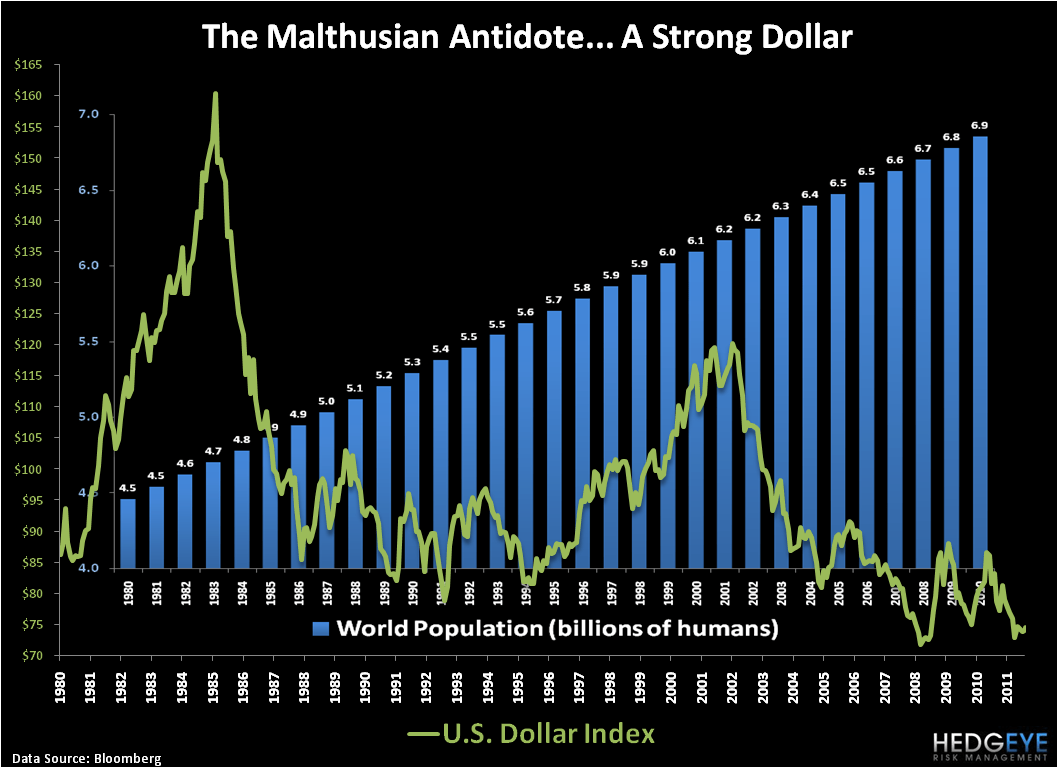

The key question that arises of any discussion of the extension of human life is whether the earth has the physical resources to support a growing population. Obviously, an important question given that human population has grown from 900 million in 1800 to just under 7 billion people today. The most famous critic of the earth’s ability to sustain population growth is Thomas Malthus, who in 1798 wrote in his “Essay on the Principle of Population”:

“Population, when unchecked, goes on doubling itself every 25 years, or increases in a geometrical ratio.”

Interestingly, Malthus’ thesis ended up being spot on for the growth of the earth’s population. Where Malthus ultimately failed was in his belief that subsistence could only grow arithmetically, which, according to his theories, would create a major issue in the future as there wouldn’t be enough resources to support the population.

Long term commodities bulls are obviously major advocates of Malthusian theories, as they describe a natural tightening of supply and demand for food, energy, and building materials. Ultimately this supply and demand will lead, according to commodity bulls, to long term favorable real price performance for commodities and impending disaster for those humans who can’t afford the accelerating price of commodities.

This is an interesting theory, but it hasn’t really played out in practice. The most prominent modern advocate of Malthusian theories is Stanford professor Paul Ehrlich, author of “The Population Bomb”. In the 1970s, he predicted that the world would run out of food (it didn’t) and in 1980 bet Julian Simon that over the next ten years, five specific metals would increase in price. So, what was the outcome? As Arrrison writes:

“During the decade from 1980 to 1990, world population grew more than 800 million – a huge increase that, according to Ehrlich, should have spelled disaster . . . Without fail, every single metal decreased in price, and Ehrlich was forced to admit defeat.”

The moral of the story is that even as the population has grown geometrically, humans have continued to innovate, live longer and healthier, and decreased their dependence on finite resources. (Incidentally, as shown in the Chart of the Day, the decade from 1980 to 1990 was also a period in which the U.S. dollar was flat (albeit with huge strengthening in between), versus trending down thereafter, which likely served to keep commodity inflation in check.)

So, as you head into the long weekend contemplating your longevity, I’ll offer a few tips. To start with, there does appear to be some credence to the health benefits of red wine, especially for those who are a little overweight, but the single and simplest tip to living a long and healthy life . . . . caloric restriction. Not sexy, but eating less works.

Enjoy the long weekend with your friends and families.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research