Darden Restaurants provided preliminary 1QFY12 EPS from continuing operations of $0.78 versus consensus of $0.87. The company also reported that 1QFY12 combined same-restaurant sales for Red Lobster, Olive Garden, and LongHorn Steakhouse are expected to increase 2.8%. This preannouncement is negative for the group but it is important to point out that some of the drivers are specific to Darden.

Preliminary 1Q U.S. same-restaurant sales results at Red Lobster, LongHorn Steakhouse and Olive Garden are 10.7%, 4.8%, and -2.9%, respectively. On a combined basis, the same-restaurant sales performance for 1Q was not terrible, but there are two important caveats to keep in mind. Olive Garden appears to have structural problems that will take some time to address and Red Lobster’s strong comp is impressive at first glance but comes almost entirely from promotion-driven traffic. An increase in price in August brought a steep decline in traffic.

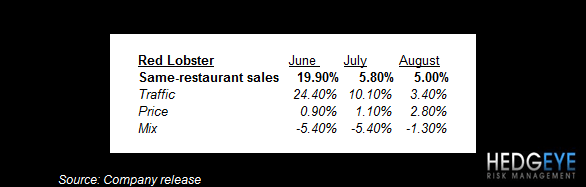

Red Lobster posted strong comp for the quarter but, with seafood inflation as high as it is, the question most investors will be posing is “are they making money?” The chart below shows the acceleration in two-year trends the preliminary 1QFY12 number implies and the table, below the chart, shows the monthly numbers for traffic, pricing, and menu-mix at Red Lobster.

Olive Garden is clearly suffering from structural problems and we believe that roughly half of the unit base needs to be remodeled. As discussed on the most recent earnings call, management plans to remodel 430 non-Tuscan Farmhouse restaurants in the Olive Garden system with completion by the end of fiscal 2014. On July 1st, management said that 60 restaurants had been remodeled for the purposes of a test and 75 are due to be remodeled this fiscal year. The schedule described by management would suggest that any issues being posed by restaurants in need of remodels are here to stay for some time!

LongHorn Steakhouse has been a strong concept for Darden over the past several quarters but this preliminary number suggests that the chain’s performance has come closer to the Street’s expectations. Same-restaurant sales were certainly strong, but a second consecutive decline – albeit marginal – in two-year average trends is not what investors were looking for. Intra-quarter, LongHorn comps slowed from 6.5% in June to 4.0% and 3.5% in July and August, respectively.

Darden has long been considered the safe haven of the casual dining space and this label has been earned by a competent management team that runs an impressive organization. Over the last few months, however, the difficult macro environment has been taking its toll on the casual dining industry. Gas prices, specifically called out by DRI CEO Clarence Otis this year, and – more recently – plummeting consumer confidence amid a confluence of headwinds have worried management and investors alike.

Today’s preannouncement of 1QFY11 EPS and same-restaurant sales will disappoint investors and likely cause many on the sell-side to realign their expectations with the change in tone from management.

Howard Penney

Managing Director

Rory Green

Analyst