Positions in Europe: Short EUR-USD (FXE); Short UK (EWU)

European capital markets whipped around last week alongside a decision late Thursday by France, Italy, Spain, and Belgium to ban short selling of bank and insurance stocks as the Swiss National Bank announced it would intervene to weaken the CHF. We continue to believe that Europe’s sovereign debt contagion has a long term TAIL and the uncertainty on the European community’s go-forward program (more below under “Calendar Catalysts”) should support marked downside in the periphery and a drag on the core over the immediate and intermediate terms. For now, investors hope Sarkozy and Merkel can cure ills over tea tomorrow – we’ll take the other side.

Short Selling Ban

To put the short selling ban in context, our Financials Sector head Josh Steiner wrote a note on Friday titled “Banning Short Selling Helps for about 5 Hours” in which he cites the short-lived bounce that US Financials (XLF) received on 9/18/08 on the SEC ban on short selling US financial stocks.

He notes specifically that “the US ban triggered a trough to peak move of 32% that lasted essentially 5 trading hours, all of which was given back over the next seven trading days. For reference, post the short-squeeze highs of $24.50 in the XLF on 9/18/08, the XLF proceeded to lose 76% of its value to its intraday low of $5.88 on March 6, 2009, roughly six months later.”

We use the US Financials short selling ban as a reference point for European bank stocks, especially for the banks of the PIIGS, France, and Germany, that saw heavy selling leading into last week’s short selling ban. To say the least, we don’t see any near term selloff as a clear buying opportunity.

Calendar Catalyst

There are a few calendar catalysts over the near to intermediate term, and the problem remains the political uncertainty on a road map to shore up sovereign debt contagion, especially as the spotlight moves to Italy and Spain. Here’s what’s ahead of us:

- Merkel and Sarkozy meet tomorrow (8/16) in Paris

- European banks, through VOLUNTARILY Private Sector Involvement (PSI), are scheduled to reduce Greece’s debt through exchanging existing bonds for new bonds with lower interest rates and longer maturities in late AUG/early SEPT

- The terms, but not size, of the EFSF will be voted on in mid to late September by EU member states

We continue to warn that we’re likely to see indecision across countries on if not the terms, but eventually the size, of the EFSF, which we see far undercapitalized to handle any bailout needs of Italy or Spain. Remember, the EFSF must be ratified by ALL EU countries, which cannot happen until parliament returns from summer recess. There are no rumors that tomorrow’s meeting between Merkel and Sarkozy will bring any clear decision, besides further stamping out the possibility of issuing a Eurobond (note: different from EFSF bonds), that the Germans are squarely against.

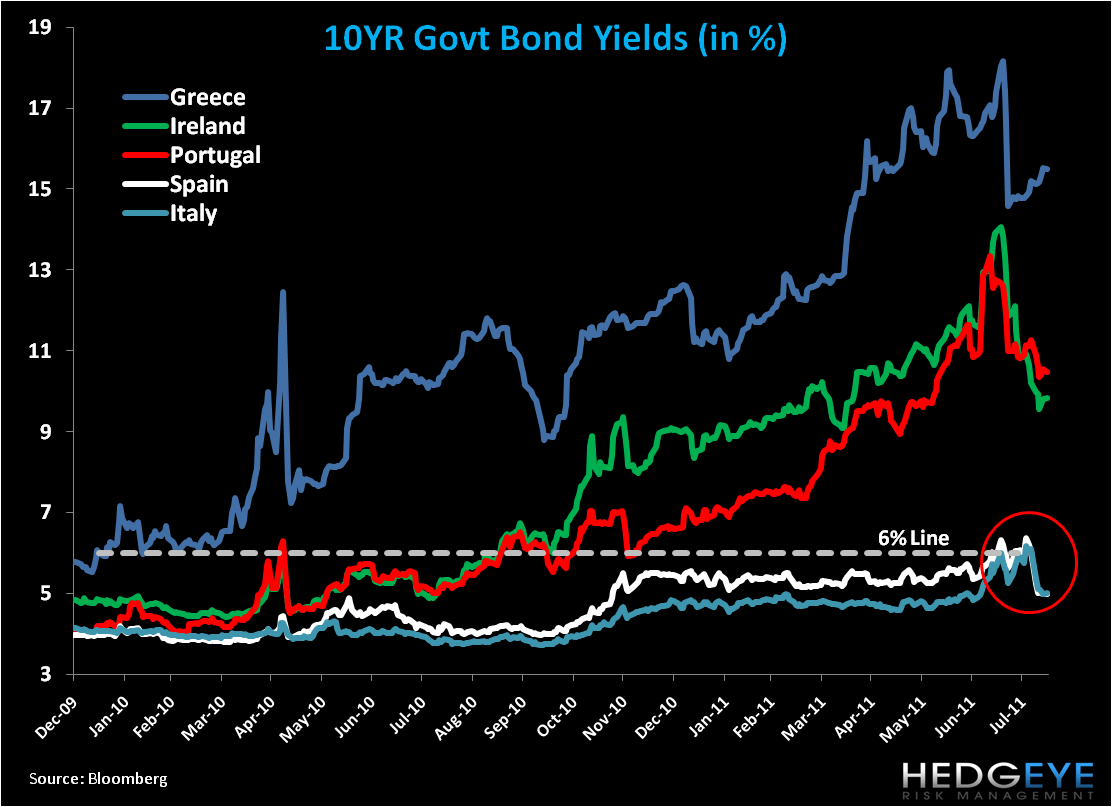

We think the ECB’s decision to re-engage the SMP bond purchasing program on 8/8 is a response to the lack of resolve on the terms and size of the EFSF, including its ability as a facility to shore up sovereign debt fears. To this end, we learned today that the ECB bought a monster €22 Billion in sovereign bonds last week! While sovereign bond yields have come in over the last week, importantly down to around 5% for Italy and Spain, there was no indication that this recent respite will hold. [Note: even in the days following the second bailout of Greece on 7/21 yields remained elevated (see chart below)].

European Financials CDS Monitor

Bank swaps in Europe were mostly wider last week. 34 of the 38 swaps were wider and 4 tighter. With the banks of no country immune to the move last week, the critical call-outs are the banks in Belgium, Germany, Greece, Italy, Portugal and Spain.

We remain short the UK due to the country's sticky stagflation and short the EUR-USD. Our trading range is $1.42 to $1.44, with the intermediate term TREND line at $1.43.

Matthew Hedrick

Senior Analyst