“Discovery consists in seeing what everyone else has seen and thinking what no one else has thought.”

- Albert Szent-Gyorgyi, Hungarian Physiologist, Nobel Prize Winner

There are tipping points in time when suspicions become reality, hunches become facts, and theories become laws. The umbrella, having being raised sufficiently, clicks. Greek mathematician, physicist, and astronomer Archimedes was once asked, according to the Roman writer Vitruvius, to determine whether or not a crown made for King Hiero II was made entirely from gold or whether silver, or another cheaper alloy, had been furtively mixed in.

An important caveat; the crown was not to be damaged in the process. Soon thereafter, upon observing the rising water level in the baths as people entered the water, Archimedes realized a method by which he could measure the volume of the crown, or any irregular shape. Knowing the volume and weight of the crown, he could easily determine the density and thereby verify the soundness of the ornament.

Archimedes ran through the streets shouting “Eureka!”, or so the story goes. These “Eureka” moments happen to all of us and are generally preceded by a period of reflection, or obliviousness, which makes the discovery all the more jarring.

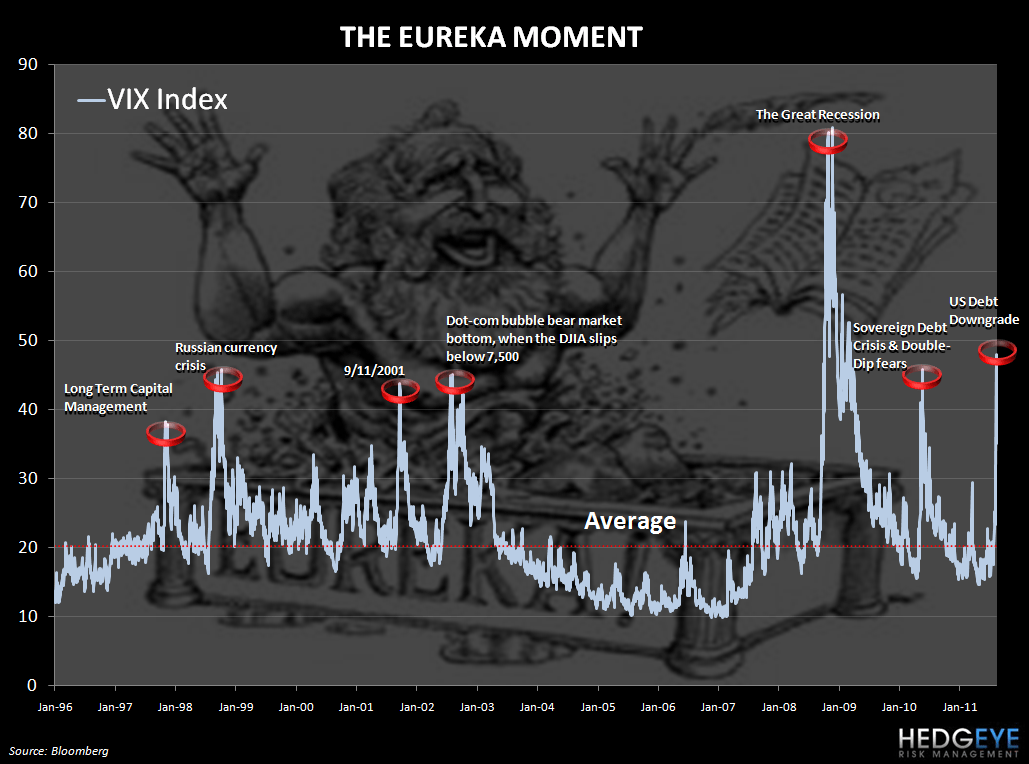

The stock market has certainly been jarred by the recent events in global macro. Of course, some investors were ahead of the game. George Soros had moved heavily to cash, for instance. For the overall market, simply looking at a chart of the S&P 500 shows quite clearly that a sudden realization came upon investors that stocks were greatly overvalued. For a proxy of the stress/fear levels on Wall Street upon this Eureka moment, and others in the past, simply take a glance at the chart at the bottom of this note.

It has long been Hedgeye’s contention, and Keith’s task on a daily basis, to highlight that big government intervention shortens economic cycles and amplifies market volatility. Uncertainty dissuades investors from allocating capital and governments tend to create uncertainty – in the long-run – via bailouts, short-selling bans, and the implementation of other interventionist policies. The volatility in the markets these past few days is testament to that fact.

To that end, today France, Italy, Spain and Belgium plan to enact bans on short selling or on short positions, which are only temporary and will do little to pacify the investment community or solve the structural problems that are impairing confidence. Josh Steiner weighed in this morning, writing a note to his clients titled, “BANNING SHORT SELLING HELPS FOR ABOUT 5 HOURS”. Steiner cites the short-lived bounce that occurred in US equity market, all of which was given back over the next seven trading days, when US authorities enacted a short selling ban in September of 2008.

As steep as the roller coaster in US equities has been (down ~13% over 14 days of trading), the government’s revisions of 1Q11 GDP has also been violent enough to cause whiplash; over thirty-five days, GDP for the first quarter was revised down 81%!

Many investors today seem to be seeking a parallel to previous periods of market volatility. Is this 1987 again or 2008 again? But how is it different? One similarity between today and 2008 is that a major banking system is hanging by a thread. Slowly, it is becoming evident that platitudes and assurances from Trichet and other banking officials in Europe are losing traction with global investors as the extent of the Old World’s problems become more apparent.

One difference is that Europe is a far less united entity than the USA. That’s not bluster, that’s a fact. As mentioned in previous Early Look editions, conflict – not unity – has been a defining characteristic of the continent. If the similarities between 2011 and 2008 are bad, the differences are almost worse!

Over the last three weeks the VIX is up 44.1%, 26.7% and 36.3% (through Thursday), respectfully. As in 2008, the XLF has led the way in this downturn. Brian Moynihan, CEO of Bank of America, is doing his best impression of Dick Fuld circa 2008, stating – in that wooden way that only corporate CEO’s can pull off – that “everything is fine”.

Mr. Moynihan has assured interviewers that CDS spreads will go back down and instructed listeners of the company’s conference call to “trust” the management team. The stock price has long been underperforming the market and the bank’s 5-year CDS spreads are currently 317 bps wide. That’s 42% higher than the 2008 peak of 226 bps on 9/18/08 and 20% below the 3/30/09 peak of 402 bps. These metrics are certainly not echoing Mr. Moynihan’s sentiments. As Main Street America sees it, CEO’s and politicians are part of a separate group which they do not understand, do not trust, yet the actions undertaken by that group greatly influences the fortunes of the rest of the country.

Hedgeye’s Healthcare guru and general thought leader, Tom Tobin, wrote this week in his team’s morning “Healthcaster” note, “We made the point on the Debt Ceiling compromise that we would look back fondly on a process that has been roundly criticized and routinely blamed for recent stock volatility.” Tom’s macro view has been on point lately and, rather than buying into the trap of seeing the passing of the debt ceiling resolution as cathartic, Tom was cognizant of the repercussions of the lack of transparency in CBO and ratings agency processes and heightening public emotions. Observing this play out, Tom wrote, is “like watching two blind umpires argue a blown call.”

Perhaps most disturbing is that “to construct its forecasts, the CBO reviews major econometric models and information from “commercial forecasting services” and also consults with and relies on the advice of its expert panel of economic advisers”, including academics and Goldman Sachs.

That’s right; the CBO bases its forecasts on the advice of Academia and Wall Street! You couldn’t make this stuff up if you tried. The logic is enough to make your head spin.

The CBO uses street forecasts to peg their GDP forecasts which lead debt and deficit projections. The Street uses federal spending to calculate its GDP forecasts. Congress cutting spending leads to falling GDP, which leads to the Street cutting forecasts, which increases debt and deficit forecasts and increases the pressure to cut spending. In the middle of this whirlwind is the consumer, who bears the brunt of the spending cuts and lack of jobs. Ultimately, the consumer is the linchpin holding the economy together. 70% of US GDP is consumption. The very nature of the negative feedback loop I describe above is impairing a massive portion of our nation’s GDP from growing.

If you believe that our current political process is “broken”, as I do, the next step in the debt ceiling debate will be no better than a made-for-TV reality show starring partisan politicians sitting on “The Super Committee” putting together back-door deals (based on flawed data) that will take us further down a path of financial morass.

In the short run, we may get a reprieve from some of the Washington madness as Congress is on vacation for the balance of the month and the Obama family is going on vacation from the 18-28th. The markets, like time, wait for nobody. Not even the President. Given the interconnected nature of global markets, with Europe facing a 2008 style financial meltdown - who is watching the store?

Again, some of the differences between 2008 and today seem worse than the similarities: joblessness is higher, more people are reliant on food stamps for sustenance, and the financial crisis threatening to wreak havoc on our economy is not here in the USA and therefore less within our government’s control. The similarities, given that we are comparing the present situation to 2008, are inherently negative. Gas prices are elevated, the VIX is spiking, stocks have fallen off a cliff, and consumer confidence is depressed.

Collective Eureka moments dictate the larger trends in the market and Hedgeye has done a better-than-bad job of being ahead of the moves we have seen since our firm’s inception. In 2008, we moved to cash (as high as 96%); in March and early April of 2009, we made some strong calls to buy US equities (buying SBUX in April). Both of the market moves that ensued were long, pronounced, and driven not by any change in what market participants were seeing, but rather a change in how they were perceiving those factors and what they were thinking.

We have observed a sea-change in how investors are thinking about this market, politics, the role of government, and earnings expectations in the past couple of weeks. The Eureka moment is here. Big government has brought around another crisis faster than almost anyone could have thought possible.

How time flies.

Function in disaster; finish in style,

Howard Penney