TODAY’S S&P 500 SET-UP - August 3, 2011

This morning the USD breaking out above its intermediate-term TREND line; the most important global macro factor affecting everything that ticks right now. As we look at today’s set up for the S&P 500, the range is 61 points or -1.61% downside to 1240 and 3.23% upside to 1301.

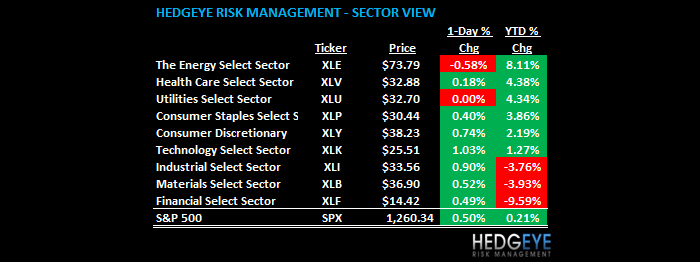

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +445 (+2195)

- VOLUME: NYSE 1352.06 (+7.98%)

- VIX: 23.28 -5.69% YTD PERFORMANCE: +31.72%

- SPX PUT/CALL RATIO: 1.52 from 2.10 (-27.82%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 25.81

- 3-MONTH T-BILL YIELD: 0.02% -0.04%

- 10-Year: 2.64 from 2.66

- YIELD CURVE: 2.31 from 2.33

MACRO DATA POINTS:

- 8:30 a.m.: Jobless Claims, est. 405k, prior 398k

- 8:30 a.m.: Bloomberg Consumer Comfort, est. (-47.5), prior (-46.8)

- 10 a.m.: Freddie Mac weekly mortgage data

- 10:30 a.m.: EIA natural gas

- 11:30 a.m.: U.S. to sell $20b 10-day cash-mgmt bills

WHAT TO WATCH:

- Japan sold yen to intervene in currency markets, acting unilaterally, Finance Minister Noda said

- Health Management Associates disclosed late yesterday had received subpoenas from Dept. of Health and Human Services: WSJ

- European Commission must decide by today whether to open in- depth investigation of ramifications from Deutsche Boerse’s buyout of NYSE Euronext

- Kraft Foods announces intent to create two independent publicly traded companies

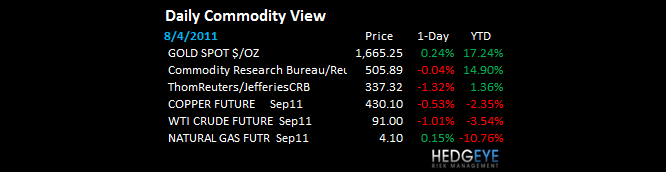

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Rio Tinto First-Half Profit Trails Estimates as Costs Increase

- Shipping Stuck in Recession on Expanding Glut: Chart of the Day

- Macarthur Lures Bidders as Peabody Rouses China: Real M&A

- Commodities to Rally, Buy Gold, JPMorgan Tells Investors

- Natural Gas Spread at 11-Year Low on Record Heat: Energy Markets

- Cargill Turkey Salmonella Link Spurs Second-Biggest U.S. Recall

- Newcrest Says 10 Die in Helicopter Crash in Indonesia

- Oil Trades Near 5-Week Low as Economy Concern Counters Stimulus

- Gold Near Record as Declining Currencies Increase Haven Demand

- Copper Premiums in China Drop to Four-Month Low on Demand

- Malaysia Export Growth Accelerates as Commodities Shipments Gain

- Coleman’s Merchant Commodity Fund Said to Decline 4.9% in July

- Copper Gains From Three-Week Low as BHP Strike Caps Second Wee

- Rogers May Boost Agriculture Investment on Food Shortages

- Rio warns on commodities outlook

- Escondida Workers to Weigh Offer at Strike-Hit Chilean Mine

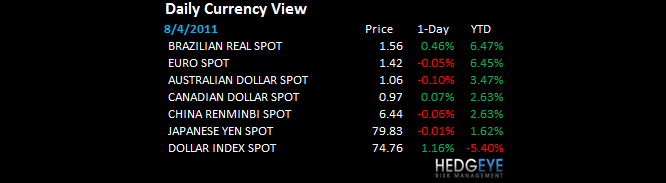

CURRENCIES

EUROPEAN MARKETS

- EUROPE: Italy is crashing, FYI (down -28% since FEB) and Russia (the only tape that was not broken) finally breaks Hedgeye TREND line support

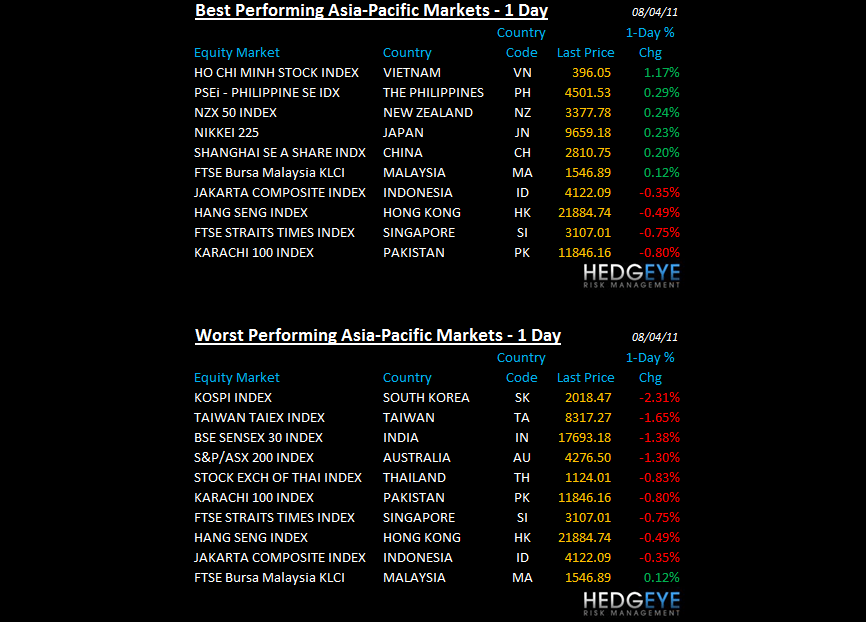

ASIAN MARKETS

- ASIA: ex-China (up +23bps overnight), Asian equity markets flashing negative divergences vs yesterdays hopeful US equity close; KOSPI breaks hard

MIDDLE EAST

Howard Penney

Managing Director